NVT shares have gone through a challenging twelve months with the stock price dropping more than 40% from its 52-week high. However, the company, which has its operations into education industry, and is set to benefit from the anticipated rise in demand for education especially from the Asian students. NVT is an Australian listed company offering a range of education services. The company has it business in four segments: university programs, School of Audio Engineering (SAE), Professional and English (PEP) and corporate.

However, a risk that looms over the company is that its competitors can always outgrow by offering and operating their own program. But such kind of threat cannot be seen in the near future, and income investors can expect the stock to grow in line with the company’s guidance and maintain dividend yield of 6.5% in the financial year 2016.

Education services businesses Academies Australasia Group Ltd (ASX: AKG) gave a disappointing full-year profit update, suggesting businesses like Navitas, who are dependent on the assistance of government, public sector or universities have risk of failing. However, NVT itself or any other report has not yet hinted any such issue. Therefore, valuing a strong company on the basis of hypothetical scenario would be too conservative.

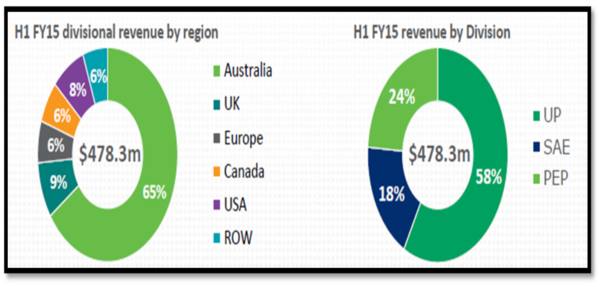

Divisional Revenue (Source - Company Reports)

Divisional Revenue (Source - Company Reports)

Revenue, EBITDA and NPAT has surged consequently over the past five years, which is a healthy sign for the company. The quality of the company can be judged from the fact that even though the bottom line has been uneven, its EBITDA has spiked over the past five years. Growth has been the outcome of healthy performance from its university programs, professional and English divisions. The company has to pull out from the Indian and Nepalese markets in the wake of non-genuine students, but it was well compensated by the US, Canada and Australian markets.

Revenue + Npat (Source - Company Reports)

Revenue + Npat (Source - Company Reports)

Net profit for the education group for the six months ending December 31 came in $31.3 million, a drop of 13.2% from $36.1 million posted in the first half of fiscal 2014. Further, there was goodwill impairment charge of $9 million regarding the contract with Macquarie University for the fall. For the half year, revenues of NVT spiked 13.9% compared to $480.5 million in the previous corresponding period. However, despite the drop the company maintained its 2015 financial year guidance of EBITDA between $162 million to $172 million.

There is no denial that Navitas is facing intense competition and tightening global economy, despite such headwinds, all three divisions of the company are expected to grow in fiscal 2015, With NVT determined to address education and training needs in the global knowledge economy, a reasonable growth can be expected even after 2015.

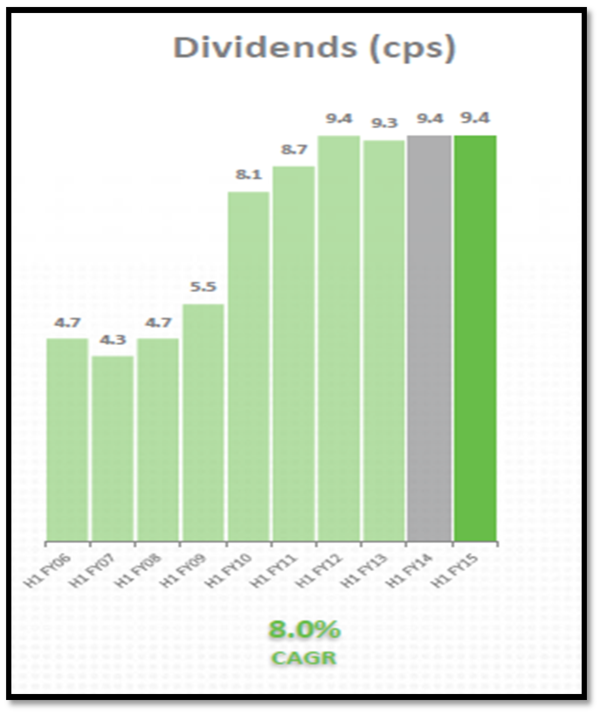

Dividends (Source - Company Reports)

Dividends (Source - Company Reports)

NVT is also looking to invest in growth opportunities and productivity improvements areas such as increasing its sales staff in source countries, US expansion of University Programs and SAE, improved staff capability and better systems and processes such as shared services. The company entered into partnership with Florida Atlantic University in Boca Raton, which marks its first substantial partnership in four years and sixth in the United States.

NVT’s Northern Hemisphere University program colleges including the UK, USA and Canada has seen an increase in the enrollments by 6%. More importantly, North America and Canada posted strong growth numbers with Canada growing by an impressive 16% and US operations posting a rise of 15% partly on the back of opening of Navitas’ sixth US College at Florida’s Atlantic University. UK results were a cause of concern with just 1% growth due to ongoing issues from the visa rules. The company does not expect the visa rules to be eased in near term. “UK government commentary since winning re-election in May does not indicate any immediate change to this policy and therefore we believe that enrollment growth in the UK will be challenging for some time,” Rod Jones, Group CEO of Navitas said last month. However, the company continues to offset weaker growth in the UK by strong growth in the US and Canada.

The Department of Education and Training has awarded NVT a role to deliver Industry Skills Fund Advisory Services. Under the program, NVT’s Professional and English Programs Division will get funding to help small, medium and large businesses to effectively utilize training optimize growth. Also, NVT has completed the acquisition of University of Canberra College Pty Limited. The acquisition will certainly help NVT to push its growth in fiscal 2015 and beyond.

NVT shares recorded an extraordinary share gain of 241% in the first six months of last year. At that time the shares were not trading at very high multiple. However, since July 2014 onwards, share of the education group tumbled performing below the S&P/ASX 200, and the underperformance continues till date. Further, NVT shares have corrected considerably over the past one month, and now are moving in positive direction, signaling excellent opportunity to rise higher from the current price point.

Thus, on the basis of above reasoning, we recommend NVT a

Buy at current price of $4.16.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.