Medibank Private Ltd

.PNG)

MPL Details

Underperformance of the Medibank brand and a slowing market in FY16: Medibank Private Ltd (ASX: MPL) is set to hold its AGM in November 2016 and reported a 46.6% growth in the group NPAT to $417.6 million in FY 16 primarily due to the improved operating profit of the Health Insurance business. However, MPL in health insurance has paid $5.1 billion on behalf of the customers and some challenges remain with the value of offer to the customers.

.png)

FY 16 Financial Performance (Source: Company Reports)

The revenue growth has remained soft due to underperformance of the Medibank brand and a slowing market. Accordingly, MPL stock fell over 22.77% in the last six months (as of November 03, 2016) while we give an “Expensive” recommendation on this dividend yield stock at the current price of – $ 2.49

.png)

MPL Daily Chart (Source: Thomson Reuters)

AMP Ltd

.PNG)

AMP Details

Profit margins might fall: AMP Ltd (ASX: AMP) reported two significant actions in its cashflows and assets under management (AUM) for the third quarter to September 30, 2016. The first one is the implementation of a significant reinsurance arrangement with Munich Reinsurance Company of Australasia Limited (Munich Re). The second step is the strengthening of best estimate assumptions across both AMP Life and NMLA effective from December 31, 2016. The group’s insurance sector has been impacted and accordingly, AMP is trying to improve their earnings stability, free-up capital while focus on their growth potential. On the other hand, the group’s cash flows in the third quarter are subdued due to the ongoing uncertainty in superannuation legislation, which led to the lower consumer confidence in the system, advisers adjusting to the enhanced regulatory environment and investment market volatility. Additionally, FY 17 profit margins for the Australian wealth protection business are expected to be impacted by combination of strengthened assumptions ($65 million) and execution of the reinsurance agreement ($25 million). This would pressurize the group’s profit margins by about $90 million. The group has also announced the notice pursuant to Corporations Act Subsection 259C(2) exemption. AMP stock fell 15.6% in the last one month (as of November 03, 2016), and we give an “Expensive” recommendation on this dividend yield stock at the current price of – $ 4.53

.png)

AMP Daily Chart (Source: Thomson Reuters)

Henderson Group PLC

.PNG)

HGG Details

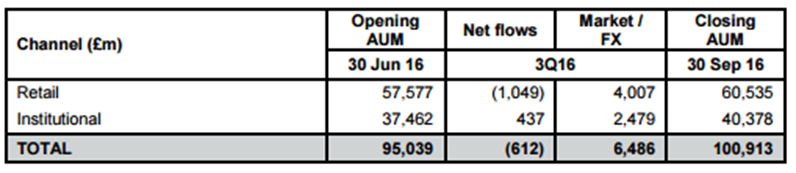

Dampening Retail client sentiment: Henderson Group PLC (ASX: HGG) posted a 6% growth in the Assets under management (AUM) to £100.9bn in the third quarter 2016 as compared to £95.0bn in June quarter. Positive markets and FX gains offset sterling weakness. However, the retail net outflows were £1.0 billion, as over 70% of the outflows occurred in July immediately after the UK Referendum. On the other hand, the institutional net flows were £0.4bn positive, which reflects the continued success in Henderson’s core UK business and an increasingly global client base in Continental Europe, the US and Australia. Long-term investment performance is said to be strong, while 77% of funds outperformed over three years.

AUM & Flows (Source: Company Reports)

HGG stock fell over 30.22% in the last six months (as of November 03, 2016), and still trading at a high P/E. The weak retail client sentiment could persist in the coming months. Accordingly, we give an “Expensive” recommendation on this dividend yield stock at the current price of – $ 3.55

HGG Daily Chart (Source: Thomson Reuters)

Cover-More Group Ltd

.PNG)

CVO Details

Raising funds for Travelex Insurance Services acquisition: Cover-More Group Ltd (ASX: CVO) has completed the retail component of A$73.3 million Entitlement offer. CVO also successfully finished the institutional non-renounceable entitlement offer and raised about $61.8 million to partially fund the acquisition of Travelex Insurance Services Inc. for US$105.0 million. The Retail Entitlement Offer closed on October 17, 2016, and raised over $11.5 million. The issue and allotment of 9.7 million shares under the Retail Entitlement offer has been completed. We give a “Buy” recommendation on the stock at the current price of – $ 1.43

.png)

CVO Daily Chart (Source: Thomson Reuters)

Bank of Queensland Limited

.PNG)

BOQ Details

BOQ’s niche businesses, including BOQ Specialist and BOQ Finance delivered strong results: Bank of Queensland Limited (ASX: BOQ) recently responded to the ASX query on Appendix 3Y (Change of Director’s Interest Notice). The group reported a 6% growth in the statutory profit after tax to $338 million for FY 16.

.png)

FY 16 Financial Performance (Source: Company Reports)

The cash earnings after tax increased to $360 million, which is due to a continuing focus on niche businesses including BOQ Specialist and BOQ Finance, coupled with a further improvement in the loan impairment expense and included the one-off $15 million investment to refine BOQ’s operating model. The group is holding its AGM on November 30, 2016. We give a “Buy” recommendation on the stock at the current price of – $ 10.02

.png)

BOQ Daily Chart (Source: Thomson Reuters)

Steadfast Group Ltd

.PNG)

SDF Details

Resilient business model for FY 17: Steadfast Group Ltd (ASX: SDF) reported a 45% growth in the underlying NPATA to $82.0 million in FY 16 and the underlying cash EPS grew 12% to 11.00 cps. The statutory NPATA grew 67% to $95.0 million while Gross Written Premium (GWP) grew 4.2% to $4.5 billion in FY 16 as compared to FY 15.

.PNG)

Underlying NPATA (Source: Company Reports)

SDF has the largest general insurance broker network in Australia and New Zealand with 27% market share in Australia. Additionally, for the FY 17 the underlying NPATA is expected to be in the range of $85 million -$90 million even when the major assumptions include the flat market conditions and no material acquisitions. We give a “Hold” recommendation on the stock at the current price of – $ 2.07

.png)

SDF Daily Chart (Source: Thomson Reuters)

Platinum Asset (Investment) Management Limited

.PNG)

PTM Details

Buy Back of shares: Platinum Asset Management Limited (ASX: PTM) will hold its AGM on November 17, 2016. PTM reported for Funds Under Management (FUM) of $ 23,404 million as at September 30, 2016 which is lower than $ 23,885 million as at August 31, 2016. The group also earlier announced for an on-market share buy-back for up to 10% of PTM’s issued share capital or about 58.7 million ordinary shares over in a year. This share buy-back indicated the confidence of the group over their potential performance. PTM stock fell 19.8% in the last six months (as of November 03, 2016), placing them at attractive valuations wherein the stock has a decent dividend yield and is trading at a reasonable P/E. Accordingly, we give a “Buy” recommendation on the stock at the current price of – $ 4.87

.png)

PTM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.