Santos Ltd

.png)

STO Dividend Details

Strong LNG sales partly offsetting the revenue pressure: Santos Ltd (ASX: STO) fourth quarter of 2015 production slightly fell by 1% year on year (yoy) to 14.9 mmboe, and accordingly the fourth quarter sales revenue fell by 24% yoy on the back of ongoing pressure in average realized oil prices which declined by 33% yoy to US$44 per barrel. Recently, Standard and Poor’s ratings Services (S&P) also downgraded the group’s long-term senior unsecured credit rating to BBB- as compared to BBB ratings. On the other hand, Santos had heavily cut its capital expenditure to over $1.66 billion in FY15 which is a 54% decrease against prior corresponding period (pcp) in order to partly offset the top line pressure. The total year production costs per barrel also fell by 10% on a yoy basis.

.png)

Fourth quarter and full year of 2015 performance highlights (Source: Company Reports)

Moreover, in the fourth quarter of 2015 GLNG train 1 produced 544,000 tonnes of LNG and delivered daily LNG production rate of more than 10% which is well ahead of the nameplate capacity driven by a solid upstream deliverability as well as consistent plant performance. GLNG’s first cargo started delivery from October 2015 and overall 11 cargoes were shipped, wherein seven cargoes were delivered to Gladstone in 4Q15. Santos also built long term contract for GLNG delivery, which would start from March 2016. The group is also strengthening its capital position and raised over $3.5 billion of capital during November leading to a $4.8 billion of cash and committed undrawn debt facilities and has no major debt maturities till 2019 in order to withstand the falling oil prices pressure. The company’s

South Australian Gas development JV effort with Origin Energy and Beach Energy has indicated completion of a six-well infill development drilling campaign in the Moomba North Field. Moomba-207 and 208 wells intersected gas pay in line with pre-drill estimates and all the wells have now been cased and suspended for future production. In view of the above developments, we reiterate our “BUY” recommendation on the stock at the current price of $3.14

.PNG)

STO Daily Chart (Source: Thomson Reuters)

OZ Minerals Ltd

OZL Dividend Details

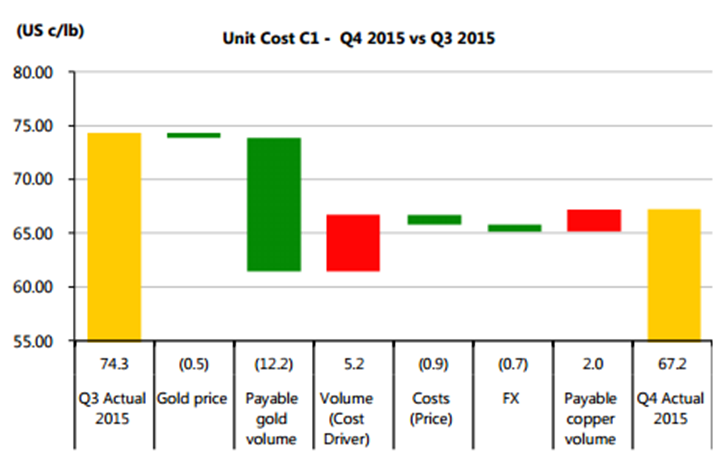

Strong capital position: OZ Minerals Ltd (ASX: OZL) reported an overall copper production of 130,305 tonnes in 2015, which is close to the upper side of the group’s issued guidance of 126,000 to 131,000 tonnes. Moreover, OZL achieved a C1 cost of USD 70.1 c/lb during 2015, while the fourth quarter of 2015 C1 cost further improved to USD 67 c/lb as compared to US 74 c/lb in the third quarter of 2015 as higher gold grades were milled. OZ Minerals remained debt free as of FY15 end and has a $553 million in cash. OZL also reported three major earn-in exploration deals located at SA, WA and QLD. The group recognized Carrapateena which has a high grade resource and the project is estimated to be announced next month. OZL is also focusing to control costs and delivered more than $5 million of annualised savings.

Unit Cost C1 factor analysis (Source: Company Reports)

OZL’s Prominent Hill concentrates Shipments reached 73,369 dry metric tonnes in the fourth quarter which comprise 29,870 ounces of gold, 223,822 ounces of silver and 37,091 tonnes of copper. The group’s focus on operational efficiency led to an open pit’s processing plant working improvement by 25% above its name plate capacity.

Meanwhile, OZL is also positioning itself for long term prospects and accordingly confirmed the ability of its Prominent Hill plant to efficiently process its stockpiles of gold ore, while the group intends its potential blend of ore to be fed into the plant after 2020. The company also updated that its Prominent Hill’s underground operation is being expanded to lift the peak capacity by 30% to 3.5 - 4.0 Mt per annum. Based on the above, we give a “BUY” recommendation on the stock at the current price of $4.11

.PNG)

OZL Daily Chart (Source: Thomson Reuters)

Woodside Petroleum Ltd

.png)

WPL Dividend Details

Updates on exploration activities and asset improvement: Woodside Petroleum Ltd (ASX: WPL) reported a 6.4% year on year (yoy) increase of production to 24.9 MMboe in the fourth quarter of 2015. On the other hand, WPL’s sales revenue fell by 37.3% yoy to $1,105 million during the quarter on the back of ongoing oil prices pressure. The group is incurring impairment charges in the range of $1,000 million to $1,200 million in pre-tax of 2015 fiscal year. Woodside Petroleum production also fell by 3% in 2015 fiscal year to 92.2 MMboe against the 95.1 MMboe in 2014 fiscal year affected by the decreased volumes in Balnaves oil asset on the back of natural reservoir decrease, but the impact was partly offset by better LNG and condensate volumes from the North West Shelf (NWS) Project. The group delivered annualized loaded LNG production rate equal to 4.9 mtpa at Pluto LNG (100% project), which is better than the average estimated annual production capacity of 4.3 mtpa forecasted by WPL during FID in 2007. Woodside Petroleum also started production from the Greater Western Flank Phase 1 Project and got approval worth of US$2.0 billion for Greater Western Flank Phase 2 Project off the north-west coast of Australia. WPL even found gas in its Myanmar’s Shwe Yee Htun-1 exploration well at Block A-6 in the Rakhine Basin and finished the excess of 6,800 square kilometers of 3D seismic. Woodside Petroleum is also raising funds by making bilateral debt agreements worth of US$350 million. WPL also confirmed that first LNG from its Wheatstone Project would be by middle of 2017 and Julimar Project would supply gas to the onshore plant.

.png)

Production and sales performance (Source: Company Reports)

The shares of WPL plunged over 27.23% in the last six months (as of February 03, 2016) like its peers given the ongoing oil prices pressure. The fall in the stock price has placed WPL at attractive valuation, which is trading at a cheaper P/E. Woodside Petroleum also has an outstanding dividend yield. Given the latest developments and trading scenario, we give a “BUY” recommendation on the stock at the current price of $27.14

WPL Daily Chart (Source: Thomson Reuters)

Syrah Resources Ltd

.png)

SYR Details

Receiving strong response for Balama Project: Syrah Resources Ltd (ASX: SYR) stock surged 21.8% (as of February 03, 2016) in the last three months as the group’s strong marketing efforts for its Balama Project have been paying off. The company has been making long term agreements for its Balama project, indicating the project’s strong demand and bright prospects. The group made a ten year Statement of Sales Intent (SSI) for up to 15,000 tonnes per annum (tpa) with a major refractory producer as well as entered into a three year Product Sales Agreement with Morgan Hairong to provide 2,000 tpa of uncoated spherical graphite. SYR even made a three year marketing Agreement with Morgan Hairong to supply 5,000 tpa of uncoated spherical graphite and 2,000 tpa of coated spherical graphite. Recently, Syrah made an SSI with Hiller Carbon for purchasing and reselling 25,000 tpa to 35,000 tpa of Balama recarburiser in the United States, Canada and Mexico regions. The group is leveraging Morgan Hairong proprietary spherical graphite coating technology by making a twenty year Technology Licensing Agreement. Meanwhile, SYR reiterated that its Balama Project development is on track with estimated beginning of the processing plant by this year end and the production ramp up is projected by the first quarter of 2017.

.png)

Syrah Resources licenses as of December 31, 2015 (Source: Company Reports)

The company is working on various development activities for the Balama Project and has commenced pre-stripping of the Balama West orebody with bulk earth works completed at the plant site. Overall, the project remains on budget and schedule. SYR reported to have AUD 191.59 million cash at the end of the December 2015 quarter. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $3.83

SYR Daily Chart (Source: Thomson Reuters)

Xero Ltd

.png)

XRO Details

Currency pressure impacted cash flows: Xero Ltd (ASX: XRO) recently reported that its December quarter of 2015 cash and short term deposit balances reached NZ$202.7 million. The group’s Cash flow from operating and investing activities fell to $(20.1) million during the quarter on the back of ongoing fall of New Zealand dollar. As a result, the group reported an impact of $1.8 million of operating and investing cash flows against the third quarter of fiscal year of 2015 and a decrease of $4.6 million (without foreign exchange impact) as compared to the corresponding period of last year.

.png)

Cash flow from operating and investing activities (Source: Company Reports)

The company reported an average revenue per user (ARPU) rise in 1H16 results driven by improvement in the UK and exchange rate movements. However, subscriber growth in the US was slightly below expectations. However, we still believe that XRO has the potential given attributes such as the improving cloud accounting market position in Australia and New Zealand with 425,000 subscribers, 65% growth in annualised committed monthly revenue over pcp and continuous expansion of solutions ecosystem. Based on the above, we give a “BUY” recommendation for the stock at the current price of $15.10

.PNG)

XRO Daily Chart (Source: Thomson Reuters)

Freelancer Ltd

.png)

FLN Details

Outstanding cash receipts growth: Freelancer Ltd (ASX: FLN) generated a 62% yoy rise of cash receipts to $11.9 million during the fourth quarter of 2015, driven by Escrow.com acquisition contribution since November 2015. FLN reported cash and equivalents of $32.2 million as of December 2015 against $42.6 million in the previous quarter as the group paid US$7.5 million for Escrow.com acquisition.

Meanwhile, Escrow.com gross payment volume improved to US$430 million in FY15, an increase of 34% as compared to US$320 million in FY14, indicating strong growth prospects from the business. Along with strong balance sheet, the company has positive operating cashflow of $0.36 million in Q4 2015 and $1.43 million for FY15. The company has also announced about NASA and FLN’s partnership in 2016 for designing an arm for a robotic astronaut on the International Space Station. Given the growth prospects, we give a “BUY” recommendation on the stock at the current price of $1.73

FLN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.