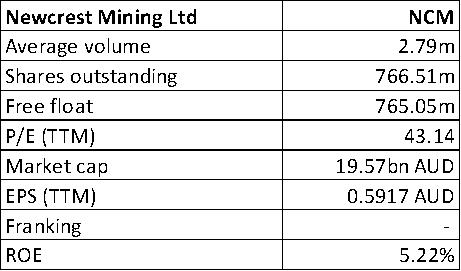

NCM Details

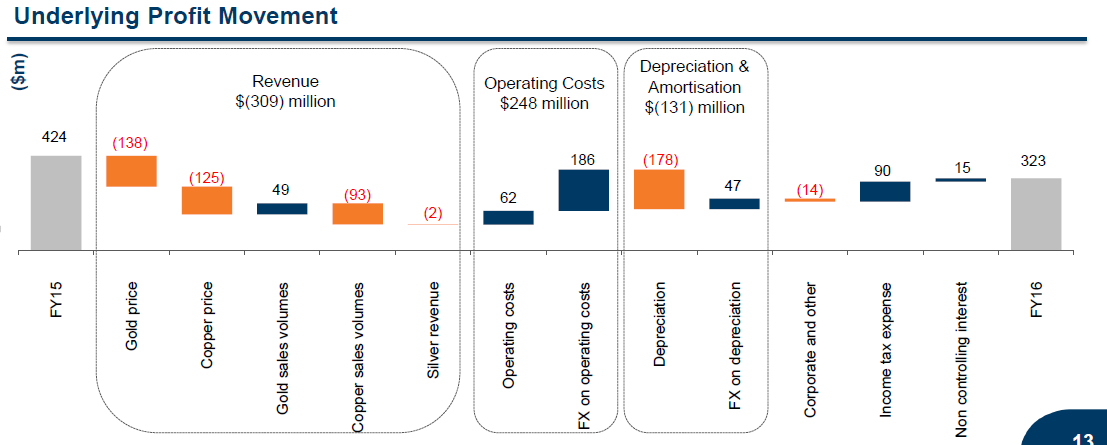

Disappointing Full year results: Newcrest Mining Limited (ASX: NCM) fell 3.9% on August 15, 2016 with the announcement of its full year results that revealed a 24% fall in underlying profit to US$323 million while statutory profit slipped by 12%. The production of 2.439 million ounces of gold has been reported. Gold revenue of $2,857 million was 3% below the prior period owing to a 5% reduction in the realised gold price. Similarly, copper revenue dropped 35% to $403 million against the prior period due to a 24% reduction in the average realised copper price and a 16% decrease in copper sales volumes as a result of lower copper production from Cadia and Telfer.

Underlying profit movement (Source: Company Reports)

Controlling costs and debt:

NCM stock otherwise delivered an outstanding performance this year, and generated over 95% returns (as of August 12, 2016) driven by the solid gold prices rally this year. Moreover, the group’s control over All-In Sustaining Cost margin and declining debt also pleased investors, further contributing to the stock performance. NCM’s net debt fell by 27% or $0.8 billion to $2.1bn as at 30 June 2016 while All-In Sustaining Cost margin fell by 8.4% to $404/oz for the fiscal year of 2016.

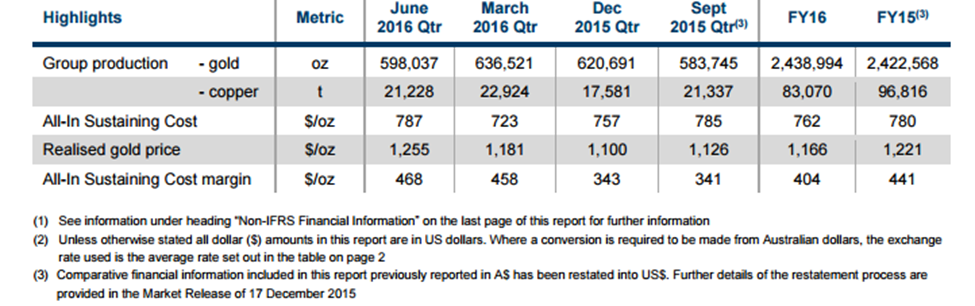

June quarter and fiscal year of 2016 performance (Source: Company Reports)

Softness in Outlook: The company commented that first quarter FY17 gold production is expected to be relatively lower than the implied average for FY17 guidance. AISC spend is expected to be maintained at around average rates.

Higher valuations: The major driver for the stock rally of NCM is gold prices rather than its production performance. During June quarter of 2016, the gold production fell by 6.0% to 598koz for the quarter while copper production fell by 7.4% to 21kt during the quarter. This lower gold production was reported on the back of extended suspension of Gosowong production after its earlier geotechnical event in February 2016 and lower grade ore processed at Cadia. Solid Lihir production and ramp up production of Cadia East also could not offset this pressure. Even the group’s All-In Sustaining Cost (AISC) per ounce for the June quarter increased by 8.9% to $787/oz due to $56 per ounce rise in sustaining capital expenditure. For FY16, the group managed to deliver only 0.7% rise in gold production to 2.4moz during the year. Copper production also fell by 14.2% to 83kt during the year.

NCM’s All-In Sustaining Cost margin fell by 8.4% to $404/oz for the year. Meanwhile, the huge rally in the stock placed NCM at unreasonable valuations, which is now trading at a higher P/E. Further, the economic headwinds relating to interest rates at a global level may impact the gold prices. We therefore recommend investors to take profits, and accordingly, give a “Sell” recommendation on the stock at the current price of $24.51

NCM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.