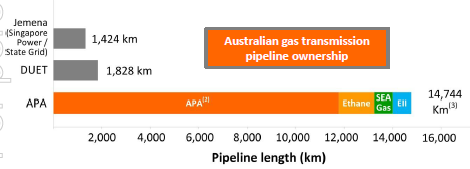

APA Group (ASX: APA) is a major gas pipeline owner by pipeline length, capacity and volume in Australia. The company has 14,744 km transmission gas pipelines for underground and LNG gas storage. The gas network pipelines are 14,744 km with 1.3 million gas consumers. APA has 585 megawatts power generation capacity, with 244 km HV electricity transmission. The group owns around 19 billion of assets. APA got a stable outlook rating from Moody’s and S&P who assigned Baa2 and BBB credit ratings respectively.

Australian gas transmission pipeline leader (Source: Company Reports)

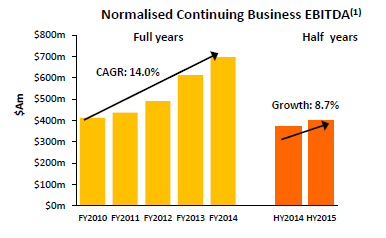

First half of 2015 highlights

APA revenues rose to $523 million for the first half of 2015, as compared to the $510 million in the first half of 2014. The group improved its EBITDA from continuing operations by 9% yoy to $401.3 million, against $369.2 million during the corresponding period of last year. The overall energy infrastructure contributed to the increase, which soared 15% yoy to $373.6 million during the period.

Solid Earnings performance history (Source: Company Reports)

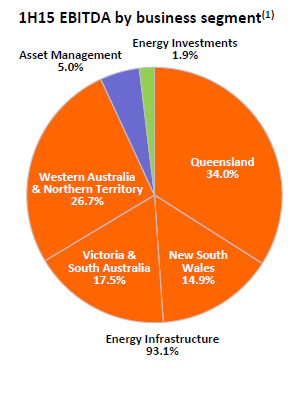

The energy infrastructure EBITDA was driven by its Queensland and Victoria & South Australia EBITDA which rose 25% yoy and 13% yoy respectively to $136.4 million and $108.8 million. However, New South wales EBITDA fell by 4% yoy to $59.6 million. The Moomba/Wallumbilla compressions were finished and the BWP bi-directional was installed as a part of the group’s initiatives to increase the East Coast grid capacity. The Victoria and NSW interconnect expansion activities are ongoing. Meanwhile, the GGP expansion project was also completed while the EGP construction is continuing. The group’s Asset management EBITDA and Energy investments also plunged by 42% and 12% on a year over year basis. The one time relocation charges of APA infrastructure and offloading the shares of Envestra contributed to the decline.

First half of 2015 EBITDA by Segment (Source: Company Reports)

Meanwhile, the group’s statutory EBITDA soared 113% yoy to $849.6 million, while the net profit after tax increased 287% yoy to $467.3 million, on the back of net pre-tax profit of $430 million coming from the sale of the group’s equity holding in AGN (earlier known as Envestra) as well as the one time performance fees of $ 17 million being refunded to APA. However, the normalized net profit after tax declined 8% yoy to $111.2 million, impacted by the omissions of the earnings and tax distributions from Envestra. But, the group has improved its operating cash flow by 22% to $263.2 million, from $216.6 million in the corresponding period of last year.

Growing business through Acquisitions

APA Group had recently entered into a new multi-service gas transportation agreement to boost its capacity at Victoria to New South Wales Interconnect. The gas sourced from Victoria to the gas market in eastern Australian will be supplied for seven years under the agreement. Accordingly, the group needs to develop looping on both the Moomba Sydney Pipeline and the Victorian Transmission System which is estimated cost over $85 million. This expansion would boost the daily capacity of the Victoria – New South Wales Interconnect by 30 TJ. The group expects to complete this expansion by mid of 2016.

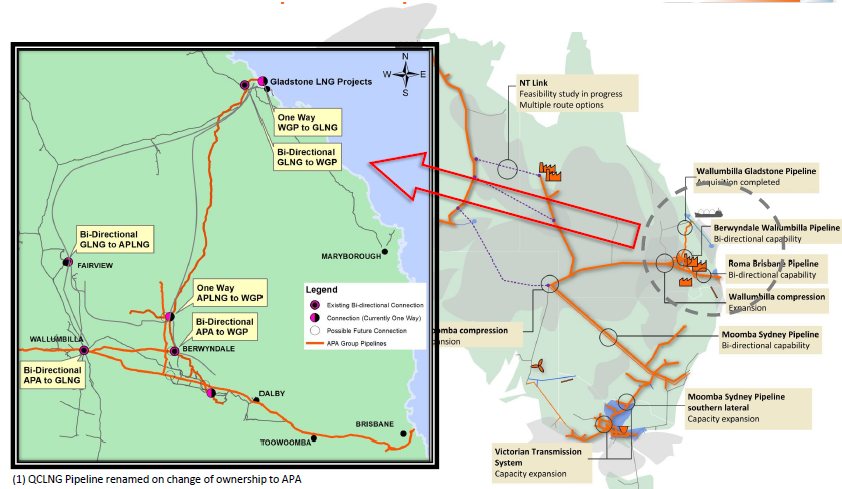

The company also completed its BG Group of the Queensland Curtis LNG (‘QCLNG’) Pipeline acquisition in June. APA acquired this for USD 4.6 billion and expects an EBITDA contribution of over USD355 million the first full year. The company retitled the QCLNG pipeline to the Wallumbilla Gladstone Pipeline (‘WGP’), which would add to its east coast gas grid with over 7,500 km across eastern Australia. The company got twenty year pay contracts from BG Group and China National Offshore Oil Corporation (‘CNOOC’), via this acquisition.

Wallumbilla Gladstone Pipeline (Source: Company Reports)

Outlook

The group issued a statutory EBITDA guidance in the range of $1,257 million to $1,272 million for the full year of 2015. The Normalized EBITDA is estimated to be in the range of $810 million to $825 million, and reflect contributions coming from the newly acquired WGP of over $35 million (at an assumed AUD/USD exchange rate of 0.77). APA also recently declared a final distribution of 20.5 cents per stapled security for the six months ended on 2015. This distribution, coupled with the interim distribution of 17.5 cents declared for March 2015 would generate a total distribution of 38.0 cents per security for the fiscal year of 2015.

Solid first quarter results, multiyear contract and acquisitions led the APA group shares higher, generating a year to date returns of 21.7%. The stock surged 9.3% in the last four weeks only driven by the news of its new multi-service gas transportation agreement and more than estimated distributions. However, we believe that investors have overbought the stock and need to be cautious ahead of its 2015 fiscal year results in August.

Based on the foregoing, we give an “Expensive” recommendation to APA group at the current levels of $9.05 , and review the stock later.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.