Hunter Hall International Ltd (ASX: HHL) improved its second half of fiscal 2015 year’s guidance, and forecasts a 30% increase in operating profit after tax , as compared to $1.63 million during first half of 2015. Meanwhile, for the total fiscal year of 2015, the operating profit is expected to be 5% better as compared to %3.65 million reported in the fiscal year of 2014. The group also announced an increase of 30% of final dividends for the fiscal year, as compared to 6.4 cents per share in last fiscal year, to be in line with the rise in operating profit after tax.

Hunter Hall first half of 2015 performance

-

Hunter Hall’s revenues from investment management fell 7.6% to $7.6 million during the first half of 2015, as compared to $8.23 million in 1H14. The group was able to maintain steady operating expenses of $5.24 million in the first half of 2015. However, the net profit after tax also reduced by 13.4% on a year over year basis to $1.7 million during the first half. Meanwhile, HHL’s funds under management improved by 5.5% to $1.01 billion as at December 31, 2014 from $960 million in June 30, 2014. The group’s funds under management slightly improved to $1,118.2 million as at June 30, 2015, as compared to $1,070.6 million in March 31, 2015. The fund flows have been improving partly due to falling Australian dollar prices.

-

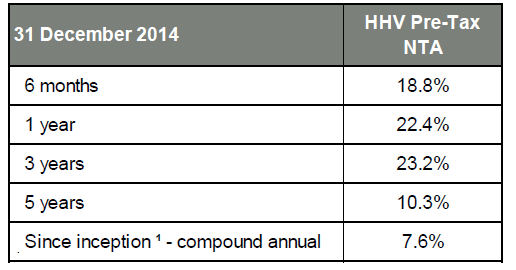

HHL reported a Pre-tax net tangible assets of 141.11 cents per share as at July 31, 2015, while Pre-tax net tangible assets excluding DTA stood at 139.71 cents per share. Meanwhile, the post-tax net tangible assets were 134.02 cents per share. As per the balance sheet highlights, HHL improved its net cash by $1.4 million to $19.3 million in 1H15, as compared to 2H14. HHL started a new fund named Hunter Hall High Conviction Equities Trust in December 2014, and expects it to deliver better returns amid volatility.

-

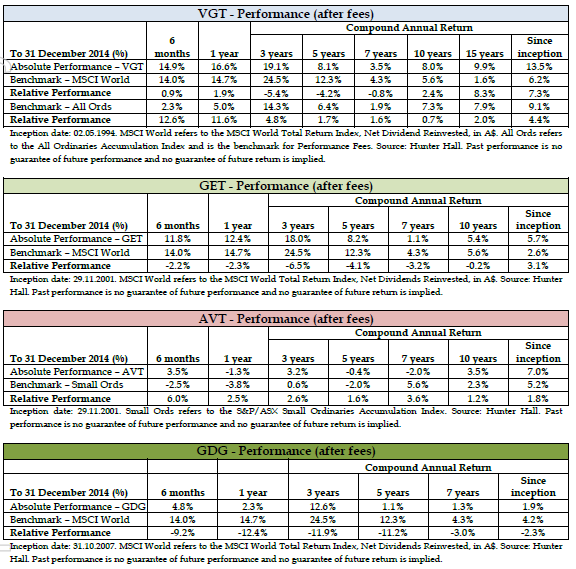

Hunter Hall funds’ performance during the period (Source: Company Reports)

-

Hunter Hall Global Value Limited (HHV) highlights

-

Hunter Hall Global Value Limited (HHV) is the listed fund of the group in ASX, and reported a decent first half of 2015, with the operating profit soaring by 24% to $41.3 million, as compared to the first half of 2014, while the net profit after tax reached $3.3 million during January 2015 month. HHV’s total shareholder returns for the first half of fiscal 2015 delivered 32.7%, against the total shareholder returns of 18.2% during the first half of fiscal 2014. NTA per share rose to $1.1745 at June 30, 2014 as compared to $1.3634 at December 31 2014. Accordingly, the NTA per share price discount has reduced to 4% at December 31 2014, from 14% at June 30 2014. HHV has been steadily improving its dividends since December 2012, and declared a part franked interim dividend of 4.0 cents per share, which would be paid on April 29, 2015.

Investment Performance (Source: Company Reports)

-

Hunter Hall Global finished 28.3 million fully paid ordinary shares placement to raise gross amount of $35.7 million at $1.26 per share. Hunter Hall Global Value also reported that it would be issuing a pro-rata non-renounceable rights issue of over 43.44 million of new fully paid ordinary shares to its shareholders at an issue price of $1.26 per share, on a 1-for-5 basis. HHV would be raising over $54.7 million through this offer.

-

Sirtex Medical, M2 telecommunications, JDS , Citigroup and Prada are the top five holdings of the fund, with net assets representing 14.9%, 4.8%, 4.1%, 3.9% and 3.6% respectively. Sirtex Medical, Take two interactive and Citigroup were the top performers in the month of July, gaining 1.5%, 08% and 0.5% respectively. However GI Dynamics, St Barbara and Seven West Media offset some of these gains by declining by 1.2%, 07% and 0.3% respectively.

Outlook

-

In July, Hunter Hall Global Value’s delivered an absolute returns of 27.2% over one year but the relative performance fell 5.7%. HHV delivered 8% absolute returns since inception while the relative performance was just 1%. Moreover, the outstanding returns ofSirtex Medical (which generated over 79.3% over the last fifty two weeks) has been partly driving the overall funds performance. On the other hand, we believe that the diversification of the overall fund is relaatively low, with major concentration on Australia, NZD and US markets (combined share of 60.2%). Moreover, if these top performers do not generate returns as expected, than the fund’s performance might be challenging going ahead.

HHL Daily Chart (Source - Thomson Reuters)

-

Hunter Hall International shares have been falling since 2008, and reduced 58.9% in last five years alone. However, the stock has been recovering this year, generating a year to date returns of over 20.5% driven by fund inflows, guidance upgrade and investment performance. On the other hand, we believe that this recovery is a short term trend and the group’s funds’ performance have relatively been inferior as compared to its competitors. Moreover, the stock is trading at expensive valuations with a higher P/E of 17.31x against its peers. Based on the foregoing, we give a “SELL” recommendation to the stock at the current price of $2.40.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.