HGG’s stock has seen a surge on the back of robust first half results and some optimism in the market with headwinds such as China and Greece factors settling down. Further, the stock is trading in vicinity of its 52-week high, making it a bit expensive to own at this time despite solid fundamentals. Year to date the stock is up over 46% while in the last twelve months the shares are up almost 32%.

HGG is a holding company of the UK investment management group Henderson Global Investors. HGG offers diversified investment advice on asset classes such as equities, fixed income, property and alternative investments.

HGG offers a good mix of both income and growth. The performance of the stock is closely tied to the performance of the broader index as investors invest more during the settled periods and when overall macro outlook is positive. With Greek debt crisis moving towards conclusion, Henderson is already guiding towards attractive growth for atleast a couple years. For instance, HGG is expected to improve its earnings by 6% in the current year and 16% in the next year. The expected numbers are impressive by any count, giving HGG a PEG number of 0.9, suggesting better capital gain going ahead.

(

Source: Company Report)

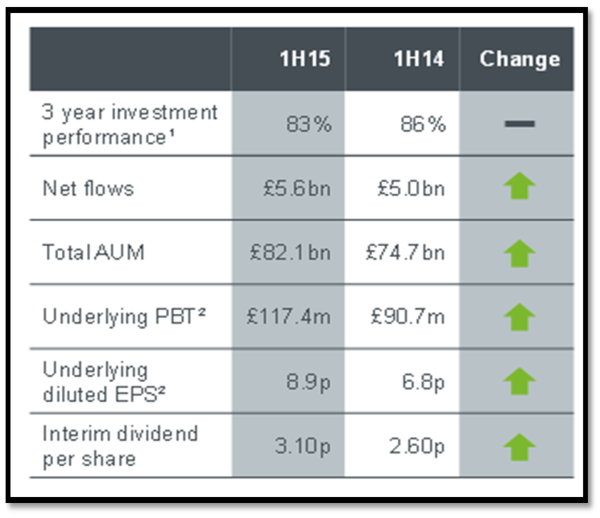

HGG posted stellar results for the six months ending June with an increase of 29% in pre-tax profit totaling to £117.4 million. The company also raised its Interim dividend by 19% to 3.1p. The result is even better after converting it to the Australian dollars as the currency is in down trend against the British currency. Cash levels for the company is strong than what the investors were expecting after the fund manager made several acquisitions including two Perennial funds and increasing stake from 41% to 100% in the 90 West Asset Management Pty Ltd. 90 West is an Australian-based resources fund manager, and its acquisition will help HGG to take benefit of the new business the firms have developed together in Australia and other regions.

(

Source: Company Report)

The acquisition of two Perennial funds will push HGG’s assets under management (AUM) in Pan-Asia to £9.6 billion ($19.2 billion) from £4.0 billion. The acquisition will give HGG a “recognized domestic investment management capabilities” and will push the company into “Top 30 of Australian asset managers,” said Andrew Formica, chief executive of Henderson. The Perennial deals are expected to be concluded by the fourth-quarter this year.

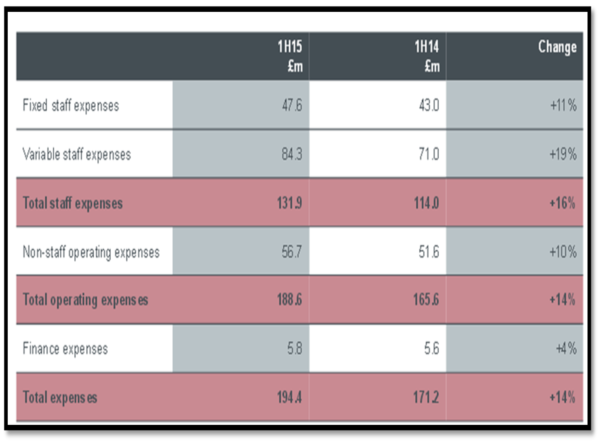

Asset under management (AUM) for the company increased by around 10% to £82.1 billion versus £74.7 billion as on 30 June 2014. Further, net flows for the period came in at £5.6 billion. The company announced underlying diluted EPS of 8.9p. Total expenses for HGG was up 14% to £194.4 million including the wage bill, which was up 11% to £47.6 million primarily due to the recent acquisitions. At the end of June, HGG posted a surplus capital of £113 million versus £44 million at the end of December last year. In addition, the net fee income was up £296.1 million for the first half.

Owing to its strong solid business performance and improved capital position, the Board also announced a share buyback program of £25.0 million, which will be implemented during the second half.

(

Source: Thomson Reuters)

HGG’s strong half yearly result has boosted investor’s confidence to accumulate the stock, and send share price higher. But it appears that all the current positive news and expectations of a robust growth has already been factored in the stock, hinting investors to be patient and wait for the stock to pull down. Though the stock is backed by strong fundamentals, but at present stock price HGG appears to be have a premium price tag.

On the basis of above factors, we recommend HGG as EXPENSIVE at current price of $5.87.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.