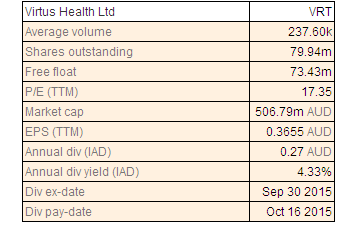

Virtus Health Ltd

VRT Dividend Details

Building business through acquisitions: Virtus Health Ltd (ASX: VRT) reported a revenue growth of 16.1% yoy to $233.7 million in FY15, against $201.2 million in prior corresponding period, boosted by the group’s domestic acquisitions and improved international operations performance. The group acquired Sydney based Independent Diagnostic Services, a general category pathology laboratory, to boost its specialist diagnostics capabilities and leverage IDS network of seven collection centers at southern suburbs of Sydney. The group has a dominant position with regards to ARS in Australia. VRT also reported that its fertility centers revenues improved more than estimated. It further maintained its leadership in Australia’s IVF services and improved its total IVF cycles to 17,064 in FY15 in comparison to 15,021 in the fiscal year of 2014, which includes contribution from TasIVF acquisition. There has been an increase of 6.6% in the fresh IVF cycle activity in Australia in the first three months of FY 2015/16. Apart from Australia and Greenfield developments, Virtus is also targeting United Kingdom and South East Asia to boost its international growth. VRT also has been able to expand UK footprint with the acquisition of Rotunda IVF in Ireland which is accretive to earnings per share.

.png)

Virtus ARS markets (Source: Company reports)

VRT stock corrected over 19.75% during this year to date impacted by the rising competition and tough market conditions. But, favorable demographic drivers in Australia coupled with improving demand across its international operations would steer growth in the near future. Potential can be seen in VRT given the increasing social trend towards later childbirth bodes in developed countries. Further, funding environment with regards to IVF supports the aforesaid trend. Given the bettering conditions, the stock recovered over 10.84% (as of Oct 28, 2015) in the last four weeks. Based on the above, we maintain our “BUY” recommendation on the stock at the current price of $6.22

Capitol Health Ltd

.png)

CAJ Dividend Details

Acquisitionsand

MRI Market shift to boost growth: Capitol Health Ltd (ASX: CAJ) is focusing on acquisitions and partnerships to generate growth in the long term. Accordingly, CAJ recently entered into an MOU with Enlitic to leverage Enlitic’s expertise and Artificial intelligence for delivering better patient outcomes. The group also finished its Southern radiology and Eastern Radiology acquisitions during April and July months, respectively. CAJ expanded its NSW radiology in Sydney through Liverpool diagnostics acquisition. The $7.2 million in annual revenues are expected to be generated based on the Liverpool’s acquisition which will be accretive to margins. Meanwhile, Capitol Health generated outstanding revenue increase by 23% yoy to $111.2 million for the FY15, partly driven by synergies from Sydney radiology, Imaging Olympic park acquisitions, and improving market penetration coupled with organic growth. CAJ’s underlying net profit before tax also climbed 59% yoy to $16.2 million, driven by the better operational efficiencies and enhanced business scalability. The Government’s favor towards MRI market players, rising ageing population, acquisition synergies and CAJ’s focus on sub specialty radiology seem to be the catalysts for growth.

.png)

Maintaining a solid growth track (Source: Company Reports)

However, we do note that the stock has crashed over 36% in last five days (as on 28 Oct, 2015) in view of the revenue guidance lowering for FY16. This comes at the back of Medicare Benefits Schedule (MBS) review which is said to impact the growth in FY16 owing to changes in referral patterns in some areas. The Company stated that the gross revenues are 4% to 6% below expectations with Victorian operations having more susceptibility to revenue weakness. More insights are to be provided during the AGM in November 2015. The company did not comment on the revenue trend for the rest of the financial year as of now. Nonetheless, we think that the company is driven by strong internal factors and may be able to deal well with the current changes. We maintain a “BUY” recommendation to the stock at the current price of $0.41

Greencross Limited

.png)

GXL Dividend Details

Expanding addressable market: Greencross Limited (ASX: GXL) business is performing well and was able to increase the size of its business from FY13 to FY15, driven by the Mammoth merger and City Farmers acquisition. The Company provided its trading update on 1Q16 stating total revenue growth of 19%. Further, group’s like-for-like (LFL) sales went up 6%. The 5% LFL result for the Australian retail operations was below expectations and 4.8% for Vet was noted. The network expansion has been significant in view of nine retail sites added (against the target of 20 for FY16), four vet practice acquisitions (for the target of $20 million of acquired vet revenue for FY16) and six co-located clinics (against the target of 12 for FY16). The co-location program is expected to enhance GXL’s exposure to the domestic veterinary services segment.

.png)

Greencross target pipeline (Source: Company Reports)

Another highlight has been the updated banking facilities that are expected to provide further debt capacity as per the agreed amendments with NAB and CBA. The amended existing debt facilities are expected to improve covenants. As noted earlier, Greencross customers spend 5x more at GXL stores which offers retail, vet and grooming services as compared to customers who shop only at its retail stores and 2x spend by customers who use only Greencross vet. Accordingly, the company is focusing on these three growth platforms, to achieve its target to boost the market share. Greencross improved its retail loyalty membership by 25% yoy to more than 2.9 million members while the Healthy Pets Plus membership surged by 43% yoy to >43,000 members during FY15. GXL shares corrected over 23.05% during this year to date (as of Oct 28, 2015) partly impacted by management changes and investor’s concerns over its organic growth. But, given the market opportunity to the group we maintain a “BUY” on GXL at the current price of $6.20

Mesoblast limited

Solid Clinical pipeline Programs: Mesoblast limited (ASX: MSB) recently reported that USPTO granted a very relevant patent disclosing MSB’s proprietary adult mesenchymal precursor cells for the use of forming and repairing the blood vessels in ischemic tissues. The group has >661 patents across 72 patent families, and the recent approval would further boost MSB’s IP in the US in cardiac and vascular diseases treatment. Moreover, MSB’s allogeneic mesenchymal stem cell-based regenerative medicine product JR-031, developed by the group’s Japanese partner JCR Pharmaceuticals, was suggested for approval. Mesoblast is also recruiting at North American sites for developing MPC-150-IM - Chronic Heart Failure, as it expects an early completion of the ongoing Phase 3 trial on the back of FDA’s acceptance of demonstration. The MPC-06-ID - Chronic Discogenic Low Back Pain (CDLBP) program is also recruiting across North American sites and MSB got positive feedback from discussions with the European Medicines Agency (to expand in European sites). Accelerated USA approval was also clarified through the FDA and an open-label of Phase 3 study of over 60 children is on.

.png)

Pipeline Programs (Source: Company Reports)

The recent update on MSB and Celgene extending their agreement and giving Celgene an extension of 6 months for the right of first refusal to license MSB’s products related to selected diseases (such as Graft versus Host Disease, inflammatory bowel diseases etc.) indicates continued interest from Celgene in MSB. Mesoblast shares delivered negative year to date performance of over 22.80% (as of Oct 28, 2015) and we view this as a bargain opportunity and accordingly give a “BUY” recommendation at the current stock price of $3.41

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.