OZ Minerals Limited

.png)

OZL Details

First concentrate will be delivered in the second half of 2019:OZ Minerals Limited (ASX: OZL) is into mining of copper, gold and silver, carrying out exploration activities and development of mining projects. The group reported revenue of $398 million in the first half 2016 while underlying NPAT reached $55 million. In the H1 2016, OZL produced copper of 58,368 tonnes and gold of 57,662 ounces at the all-in sustaining cost of US 120c/lb. The underground ore production has increased by 18 percent (to 1Mt) driven by better operating performance. Meanwhile, the Carrapateena project progress is on track to deliver first concentrate in the second half of 2019.

.png)

Financial Performance for 1H 2016 (Source: Company Reports)

Additionally, OZL’s strategy to partner with junior exploration companies has led in the search for copper, lead/zinc and nickel being broadened from SA to extend to WA and QLD. OZL has signed the deal with Mithril Resources targeting the Coompana block in the far west of SA, leveraging newly released exploration data under the South Australian PACE program. OZL has signed the deal with Cassini Resources to focus on their Nebo-Babel resource estimate of 203.1Mt (95.5Mt indicated resources and 107.5Mt inferred resources) and the wider highly prospective West Musgrave Province.

OZL is paying interim dividend amount of 6 cents per share totaling $18.1 million on September 23, 2016 and is trading ex-dividend on September 08, 2016. The stock has risen 32.95% in the last six months (as of August 18, 2016). We give a “Hold” recommendation on the stock at the current price of $6.96

OZL Daily Chart (Source: Thomson Reuters)

REA Group Ltd

.png)

REA Details

Impact from weaker listings: REA Group Ltd (ASX: REA) reported its FY16 numbers with revenues up 20% year on year (yoy) to $630m and EBITDA up 22% yoy to $347m. REA’s NPAT was $215m with 16% growth. The company’s cost growth has moved up to 34% yoy in 4Q16 against the 22% yoy revenue growth. REA’s listing volumes also got an impact from the recent election outcome with a 11% fall yoy. Australia witnessed a revenue growth falling from 22.4% in 1H16 to 12.5% in 2H16 owing to the weaker listings.

.png)

Revenue, EBITDA and margin trend (Source: Company Reports)

REA is still well positioned for continued growth from price rises across core depth products and even iProperty is seen to boost growth in long term. The company is trading ex-dividend on August 23, 2016 and will pay final dividend on September 15, 2016. We put a “Hold” recommendation on the stock at the current price of $60.58

REA Daily Chart (Source: Thomson Reuters)

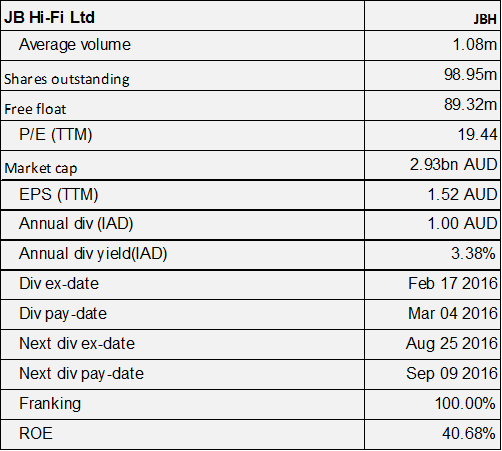

JB Hi-Fi Ltd

JBH Details

Strong FY16 results:JB Hi-Fi Ltd (ASX: JBH) has reported a very strong FY16 result driven by robust sales and gross margin underpinned by sales of $3,954m witnessing a growth of 8.3%, EBITDA of $262.1m up 9.2% and NPAT of $152.2m up 11.5%. The company has indicated for a good start to FY17 with 9.5% Like for like sales growth. JBH also took the advantage of a buoyant consumer environment with market share gains post Dick Smith’s demise. The company reported for 97% cash conversion.

The management has guided to FY17 sales of $4.25bn. The company is trading ex-dividend on August 25, 2016 and will pay final dividend (37 cents) on September 09, 2016. We give a “Hold” recommendation on the stock at the current price of $28.95

JBH Daily Chart (Source: Thomson Reuters)

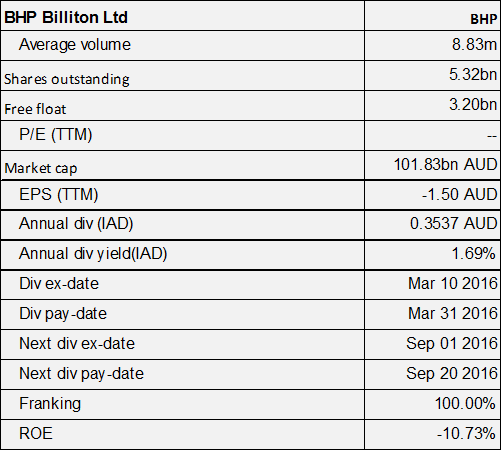

BHP Billiton Ltd

BHP Details

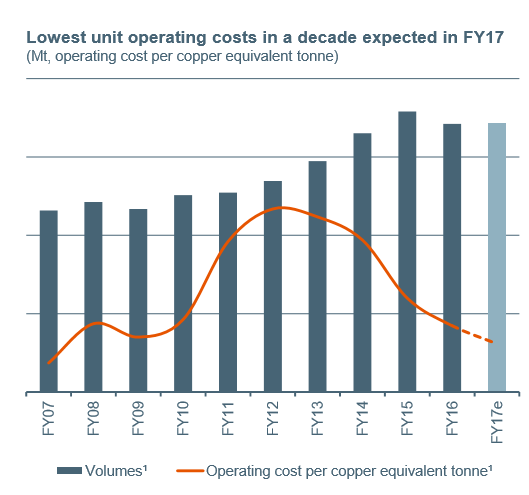

FY17 Production Guidance largely unchanged: BHP Billiton Ltd (ASX: BHP) reported better than expected FY16 underlying NPAT of US$1.2b and underlying EBITDA of US$12.3b at the back of lower costs. Unit cash costs across the Group down 16% from FY15. BHP also updated about impact from Samarco dam failure with direct costs incurred by BHP Billiton of US$70 million. On the other hand, BHP’s net debt rose slightly to US$26.1b owing to lower working capital release and negative revaluation of debt. The miner reported better than expected results for all divisions than expected with copper and coal doing well on lower costs. The company has reduced its capex guidance for FY17 from US$5.7b to US$5.4b.

Unit Operating Costs (Source: Company Reports)

FY17 Production guidance for petroleum (200-210 MMBoe), iron ore (265-275 mm tons, WAIO basis) and met coal (40 mm tons) were all unchanged. FY17 copper guidance was lowered to 1.66 mm tons from earlier 1.7 mm tons and thermal coal guidance was lowered to 30 mm tons versus previous guidance of 32 mm tons.

The company is trading ex-dividend on September 01, 2016 and will pay final dividend (18.18 cents) on September 20, 2016. We give a “Buy” recommendation on the stock at the current price of $21.29

.PNG)

BHP Daily Chart (Source: Thomson Reuters)

Villa World Ltd

.png)

VLW Details

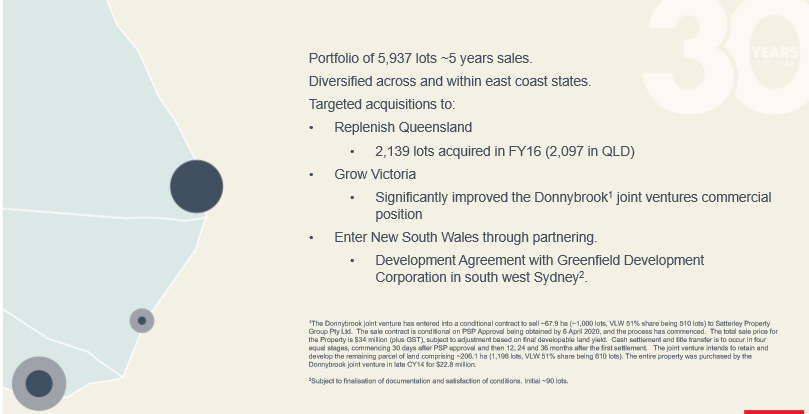

Robust sales result: Villa World Ltd (ASX: VLW) reported a strong FY16 result with statutory NPBT rising about 62% to $47.2m which is 1.3% ahead of guidance while NPAT rose 32% to $33.7m. The company has reported for revenue rise of 20% to $387m given continued sales momentum. VLW achieved a total of 1,185 sales during FY16 as compared to 843 in the prior corresponding period. Queensland was a big contributor to the results with 74% of sales and 83% of revenue given the number of projects. Underlying gross margins dipped by 50bps to 26.5%, and are expected to be between 24-26% in FY17. VLW provided FY17 NPAT guidance of at least $35.4m.

Strategic Portfolio (Source: Company Reports)

The company is trading ex-dividend on September 01, 2016 and will pay final dividend (10 cents) on September 30, 2016. The stock is up 13.5% in the last three months (as at August 18, 2016). We give a “Hold” recommendation on the stock at the current price of $2.49

VLW Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.