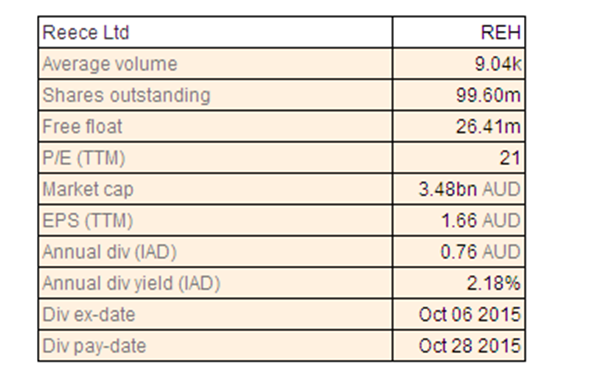

Reece Ltd

REH Dividend Details

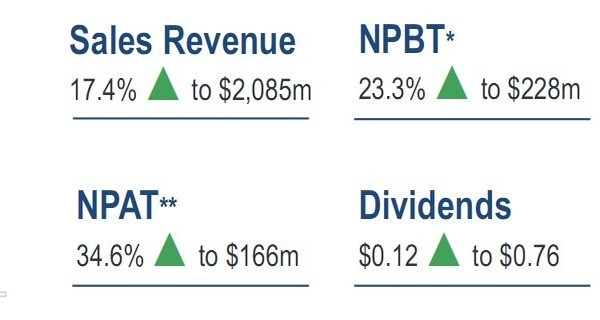

Record result and integration update: Reece Ltd (ASX: REH) has announced that sales for the first quarter of FY2016 were up 9% at $ 571 million and as a result, net profit after tax at 31 December 2015 is expected to be more than 15% above the previous year. Sales in FY 2015 was in excess of $ 2 billion for the first time in the history of the company growing by 17.4% to $ 2.08 billion. Net profit after tax grew by 34% to $ 165.6 million and both results are records for the company.

Performance (Source: Company Reports)

Dividends declared by the company for FY 2015 grew 12 cents per share to 76 cents per share and a final dividend of 52 cents per share fully franked was declared. EBIT was up 25.4% to $ 237 million because of the increase in margins by 73 basis points to 11.4%. Net assets were up 12% to $ 926 million. The branch network stood at 571 outlets with the opening of 14 new outlets in FY 2015. The supply chain was strengthened with the new Melbourne Distribution Centre and the new Perth Distribution Centre in development. Functions and roles were also realigned in order to obtain better alignment. In addition to the record results, the integration of Actrol and Metaflex was completed and the company continues to invest heavily in its core business to maintain its competitive advantage.

We acknowledge that the company is doing well and will continue to do so but regard the stock as overvalued while trading at a high PE ratio, and do not recommend a buy at the moment.

REH Daily Chart (Source: Thomson Reuters)

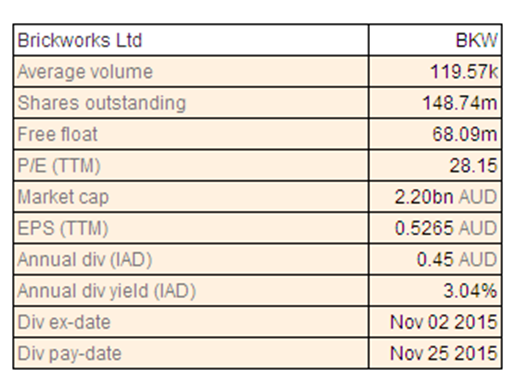

Brickworks Ltd

BKW Dividend Details

Stability in revenue stream but softness in statutory profit after tax: The corporate structure of Brickworks Ltd (ASX: BKW) provides diversification and stable earnings over the long term and there are three main components of the structure. There is the Building Products Group, Land and Development and Investments. The Building Products Group consists of Austral Bricks, Austral Masonry, Bristile Roofing, Austral Precast and Auswest Timbers. The Land and Development business has the job of maximising the value of surplus land created by the Building Products division. The 42.72% stake in Washington H Pattinson provide a stable revenue stream as well as superior returns. For the financial year ending 31 July 2015, the underlying net profit after tax grew by 18.5% to $ 120.3 million and underlying EPS grew by the same percentage to 81.1 cents per share.

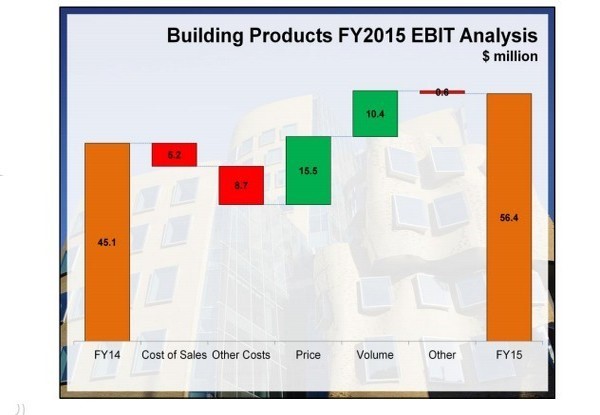

Building Products FY15 EBIT (Source: Company Reports)

Statutory net profit after tax of $ 78.1 million was down by 24% and statutory EPS was down by 24.2% to 52.6 cents per share. The company reported earnings contribution from all three businesses which delivered earnings growth compared to the previous year. Statutory profit after tax was impacted by the significant items relating to non-cash impairments in Austral Precast and Auswest Timbers and in Washington H Soul Pattinson subsidiary companies. The board of directors has increased the final dividend by 2 cents per share to 30 cents per share fully franked taking the full-year dividend to 45 cents per share fully franked.

We note that at the current price, the stock remains expensive.

BKW Daily Chart (Source: Thomson Reuters)

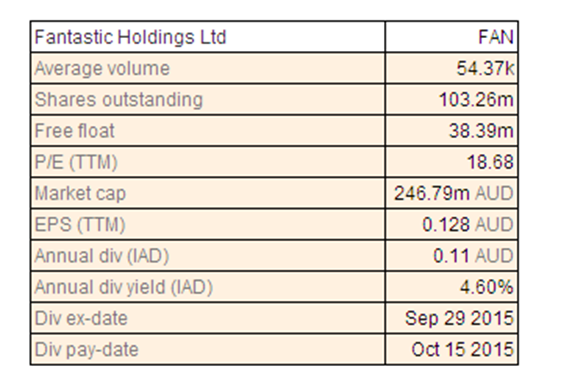

Fantastic Holdings Ltd

FAN Dividend Details

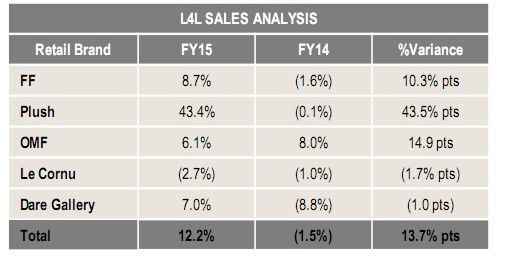

New stores and better product offerings: For the year FY 2015, Fantastic Holdings Ltd (ASX: FAN) reported record statutory sales of $ 496.9 million which is an increase of 11% over the previous year and group EBIT of $ 19 million representing an increase of 116.9%. Comparative store sales increase was 12.2% largely because of increases delivered by Fantastic Furniture and Plush which jointly account for around 85% of group sales. The strong second-half sales came mainly from Fantastic Furniture which reported an increase of 15.9% over the previous period and Plush which reported growth of 35%. The increase in sales was delivered by an enhanced product offering, improved advertising communication and customer service and a more engaged workforce. Dare Gallery was successfully divested during the year and the China-based manufacturing joint-venture came into production and started shipping. The Le Cornu business faced issues and lost market share from the growth of Fantastic Furniture and Plush as well as the opening of the new Ashley store. However, because of the history and the unique propositions offered, management is focused on restoring market share and improving business productivity. Undelivered customer orders as on 30 June 2015 was $ 34.3 million, which is an increase of 8.4% over the previous year. Operating cash flow for the year was $ 24.3 million and the group had a net cash position of $ 31.7 million after accounting for debt of $ 5 million.

LFL Sales (Source: Company Reports)

The momentum of FY 2015 has continued and group like for like sales growth for the first quarter of FY 2016 is 16.9%. The company has a good past performance and a growth platform for the future but we believe that the share is pricey at the current prevailing level given the high PE ratio and current price about the 52-week high.

FAN Daily Chart (Source: Thomson Reuters)

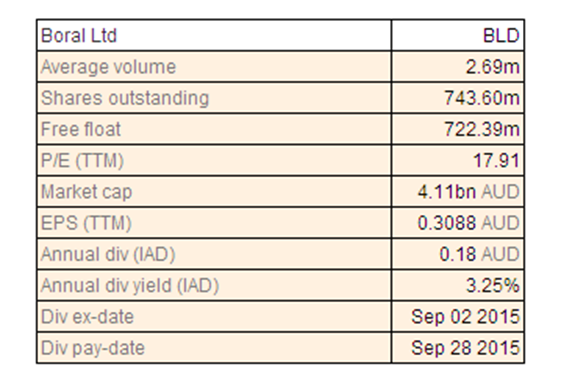

Boral Ltd

BLD Dividend Details

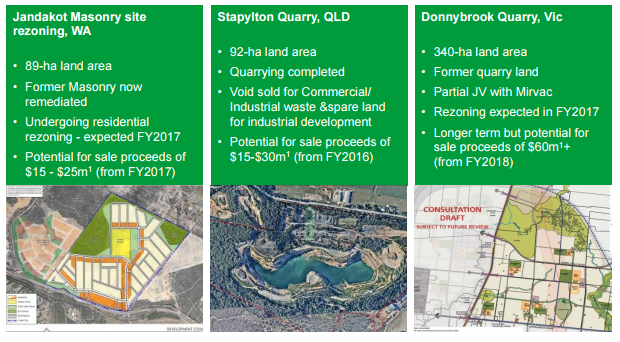

Steady Outlook and US market conditions to improve: Boral Ltd (ASX: BLD) is an international building products and construction materials company with operations in Australasia, the USA and Asia. It operates across 13 countries and employs more than 12,000 people. The four operating divisions all of which have defined strategic priorities are Construction Materials and Cement, Building Products, Boral Gypsum and Boral USA. The company’s Penrith Lake Development Site has been estimated to have 5,000 residential lots with potential earnings from FY17. Results for FY 2050 highlights are reported with revenue of $ 4.4 billion, profit after tax of $ 249 million up 45%, EBIT of $ 357 million up 21% and gearing of 19%.

Property Pipeline (Source: Company Reports)

Construction Materials and Cement is expected excluding property to maintain the same high levels of EBIT in FY 2016 as the achievement in FY 2015. A multi-year recovery in infrastructure spearheaded by major roads projects is expected to benefit by late FY 2016 continuing into FY 2017. Building Products is expected to improve underlying earnings growth despite the soft forecast for housing activity. Reported EBIT in FY 2016 is expected to be similar to FY 2015 because of the impact of the Bricks East earnings moving to 40% post-tax equity accounted earnings. Further, underlying business improvements can be expected from Boral Gypsum and Sheetrock volumes should grow and synergies strengthen in FY 2016. Finally, Boral USA is expected to increase EBIT in line with the expected 1.2 million housing that starts in FY 2016. The market is understandably encouraged by the gradual improvement in performance of the company but we believe that the current stock price represents an unrealistic premium on the true value of the company. We find the stock to be expensive at the current price level.

BLD Daily Chart (Source: Thomson Reuters)

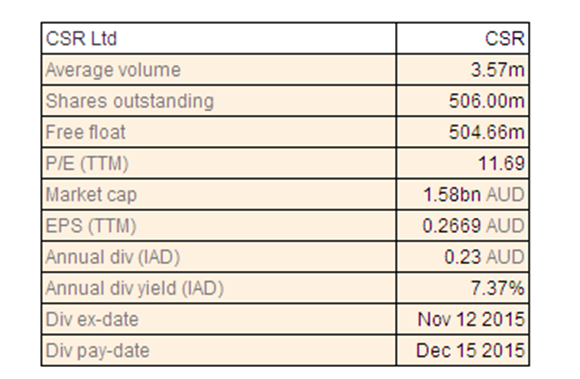

CSR Ltd

CSR Dividend Details

Improvement in all businesses and pipeline of work in residential construction markets: CSR Ltd (ASX: CSR) has reported an impressive performance for the half-year to 30 September 2015. Revenue was up 14% to $ 1.1 billion, EBIT up by 31% to $ 149.3 million, net profit after tax up by 32 % to $ 92.4 million, statutory net profit up by 13% to $ 77.6 million, EPS up by 32% to 18.3 cents per share and unfranked half-year dividend up 35% to 11.5 cents per share. The growth in trading revenue was because of a 12 % increase in residential market activity and the strong performance from recent transactions. The significant items of $ 24.3 million before tax includes transaction and integration costs to complete the Bricks JV. The EBIT reflects strong performance in all businesses. Building Products reported a 42% increase to $ 89.9 million and growth was 30% if the minority portion of PGH Bricks is excluded. There were market share gains in AFS and Hebel as well as margin improvements in all businesses. Viridian reported a higher EBIT of $ 2.3 million as a result of pricing initiatives and improved product mix.

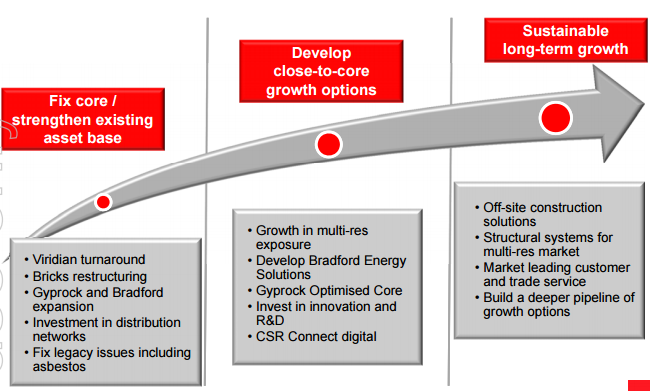

Phases of CSR’s approach (Source: Company Reports)

There was an investment of approximately $ 3 million in product development and business improvement. Aluminium reported an increase of 32% to $ 54.7 million because of a 5% increase in realised prices despite a decline of 2% in volume because of shipment timing and the benefit of $11 million because of “pot linings” and RET reduction. Property reported a decline to $ 16.2 million because of the settlement of the second tranche of the New Lynn Auckland site.

We believe that despite the aforesaid performance, the stock looks expensive.

CSR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.