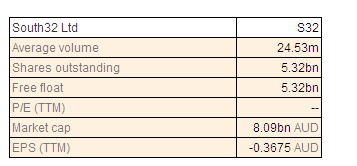

South32 Ltd.

Operating efficiency enhancement efforts to boost bottom line: South32 Ltd (ASX: S32) shares corrected over 26.73% since its listing till date, after touching all-time high of $2.45 in May. But, we believe that the recent sell was due to profit booking by investors in South32 Ltd, as each eligible BHP Billiton shareholder got a share in South32 during the demerger. Moreover, the group is focusing on controlling its costs by at least US$350 million per annum by the end of fiscal year of 2018 and intends to cut capital expenditure by 9% for the next fiscal year to US$650 million. South already achieved a pro forma productivity led cost efficiency of over US$282 million in the fiscal year of 2015 and with management focusing more on regional operations by decreasing layers of management, the group is expected to derive more benefits. S32 improved its pro forma underlying earnings by 41% to US$575 million during the period.

Operating efficiency enhancement efforts to boost bottom line: South32 Ltd (ASX: S32) shares corrected over 26.73% since its listing till date, after touching all-time high of $2.45 in May. But, we believe that the recent sell was due to profit booking by investors in South32 Ltd, as each eligible BHP Billiton shareholder got a share in South32 during the demerger. Moreover, the group is focusing on controlling its costs by at least US$350 million per annum by the end of fiscal year of 2018 and intends to cut capital expenditure by 9% for the next fiscal year to US$650 million. South already achieved a pro forma productivity led cost efficiency of over US$282 million in the fiscal year of 2015 and with management focusing more on regional operations by decreasing layers of management, the group is expected to derive more benefits. S32 improved its pro forma underlying earnings by 41% to US$575 million during the period.

Converting high value resources to reserves (Source: Company reports)

The group is maintaining a decent balance sheet, and got a credit quality rating of BBB+/Baa1 from Standards & Poor’s and Moody’s. South32 stock rallied over 4.5% in just last five days and we reiterate our “BUY” rating at the current price of $1.51.

.bmp)

S32 Daily Chart (Source: Thomson Reuters)

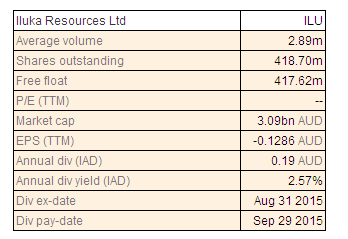

Iluka Resources

Improving production to offset commodity prices pressure: Iluka Resources Limited (ASX: ILU) stock fell over 11.95% (as of Oct 13, 2015) in the last six months due to China market slowdown and falling commodity prices. But ILU is improving Z/R/SR production in the coming periods to maintain its sales revenues growth. The company’s mineral sands revenue surged by 2% yoy to $349.6 million in the first half of 2015, driven by the better revenue per tonne given the falling Australian dollar. Unit cash costs excluding by-products plunged 14.3% yoy to $616/tonne, while unit cash costs including by-products fell 20.4% to $634/tonne during 1H15. ILU also has a solid resource potential and recent doray’s agreement indicates solid gold potential in the western gawler craton project area. ILU would continue its cost cutting efforts and intends to improve its unit cash costs further.

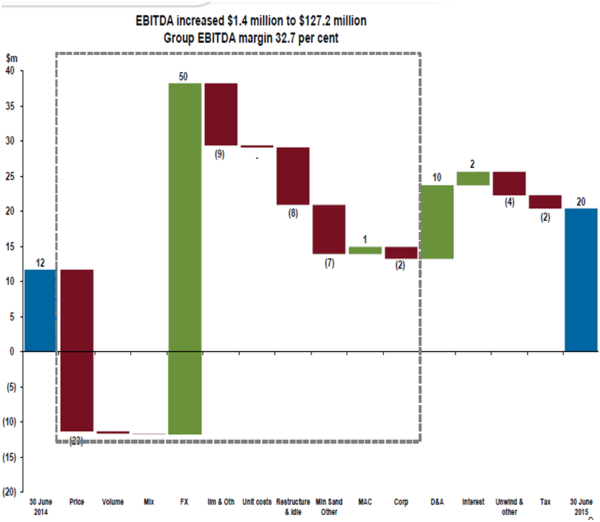

EBITDA improvement (Source: Company Reports)

Recent updates entail Horsham council evaluating an application from Iluka Resources to subdivide land at its Kanagulk mine. We remain bullish on the stock and reiterate our “BUY” recommendation at the current stock price of $7.22.

ILU Daily Chart (Source: Thomson Reuters)

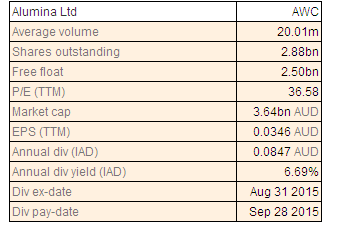

Alumina Limited

Improving performance despite pricing pressure: Alumina Limited (ASX: AWC) is improving its performance, witnessing a net profit after tax of US$122 million in the first half of fiscal 2015, against the net loss of US$47 million in the corresponding period of last year. Recently, Alcoa reported 11% dip in revenues to $5.6 billion during third quarter of 2015 owing to divestures, closures and market headwinds. Alcoa Management however commented that alumina segment maintained solid margins during the third quarter. The market is expected to view the Alumina division result as a positive. Meanwhile, Alumina mines are placed among the lowest cash cost of production in the world. Growing demand from Malaysia would offer some respite to the firm in the short term while the overall global demand is estimated to recover in the long term. Alumina has an attractive dividend yield of about 6.69%. We give a “BUY” recommendation on the stock at the current price of $1.23.

AWC Daily Chart (Source: Thomson Reuters)

Origin Energy

.png)

Strengthening capital reserves for better flexibility: Origin Energy Ltd (ASX: ORG) is focusing on boosting its capital and accordingly announced its capital raising initiatives of $4.7 billion during last month to strengthen financial flexibility. Therefore, ORG announced a $2.5 billion of fully underwritten pro rata entitlement offer. Explorations by Origin and its joint ventures have been showing positive performance, indicating the group’s solid portfolio of assets and its capabilities of potential production. The drilling at Yolla-5 and Yolla-6 production wells in the Bass Basin occurred and accordingly Origin started production. Australia Pacific LNG would start selling its first share of gas production from its ATP620/648 fields to QGC during fiscal year of 2016 further boosting its top line. The group expects its Energy Markets performance to be at par with its 2015 fiscal year, driven by rising natural gas sales to LNG projects. The recent China trade data has hit the stock price which has raised few concerns.

Origin’s exploration and production permits and data (Source: Company Reports)

However, considering that ORG has a solid dividend yield of 7.97% and is focusing on internal growth drivers, we maintain our positive stance on Origin and reiterate our “BUY” recommendation at the current price of $5.93.

.bmp)

ORG Daily Chart (Source: Thomson Reuters)

Santos

.png)

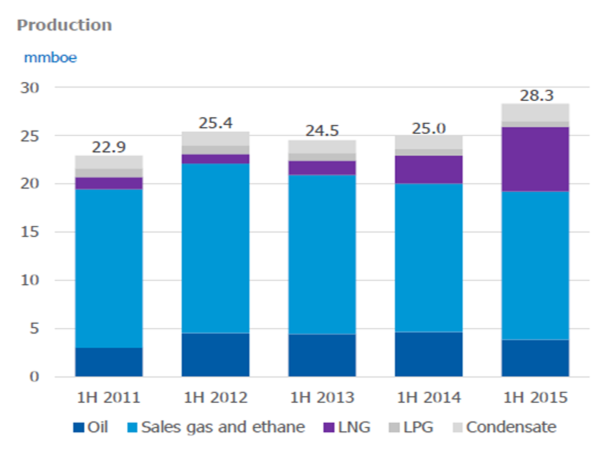

Positive Outlook: Santos Ltd (ASX: STO) stock plunged over 26.07% in the last three months impacted by falling oil prices and poor first half of 2015 financial year. The group’s revenues plunged over 15% yoy to $1.6 billion in the first half of 2015 financial year while EBIT plunged 36% yoy to $226 million impacted by 90% yoy increase in exploration expenses. On the other hand, the group’s Asia Pacific EBITDAX witnessed a major increase due to PNG LNG half-year of production. STO also boosted its overall production by 13% yoy to 28.3 mmboe driven by more than expected production from PNG LNG and Darwin LNG as well as Cooper gas. LNG production soared 131% on a year over year basis in the first half of 2015, while the GLNG first LNG is estimated to be delivered by the third quarter of the fiscal year. STO shares rose over 23.99% in the last four weeks (as of Oct 13, 2015) alone partly driven by positive exploration results. The group’s JV with drillsearch for Washington -1 well at PEL 570 confirmed gas shows across Toolachee, Epsilon and Patchawarra formations and the well is cased and suspended for future. Maroochydore-1 exploration well at ATP 924 on Inland cook oil fairway in Southwest Queensland is underway. As per south Australian oil project highlights, five well program (joint venture, Beach and Origin) in greater limestone creek area had two appraisal wells and one near field exploration well. The fourth well in south Australian gas- Tirrawarra-86 is cased and suspended post the intersection of oil and gas play in target zones on track with estimates. With regards to the Queensland gas project highlights (joint venture, Beach and Origin), Whanto south west-1 well is on track with pre drill estimates and the well is cased and suspended. Santos has a solid dividend yield of 5.5% and is focusing on improving production and operational efficiencies. The company is also focusing on cost reduction strategy that is speculated to partly entail cutting of about 200 jobs from eastern Australian business.

Rising Production (Source: Company Reports)

Any possible recovery of oil prices or Australian dollar would add support to the stock in the coming months. Based on the foregoing, we give a “BUY” recommendation to the stock at the current price of $5.56.

.bmp)

STO Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2015 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.