Hub24 Ltd

.png)

HUB Details

Solid Funds under Administration growth: Hub24 Ltd (ASX: HUB) reported an outstanding Funds under Administration (FUA) growth of more than 100% to $1.7 billion for FY15 driven by $20.23 million revenue contribution via Paragem acquisition. Accordingly, its revenues surged by 626% year on year (yoy) to $29.3 million in FY15 with its Platform segment revenue rising by 151% yoy during the period. As a result, the shares of HUB generated a strong returns during this year, and rallied over 295.76% in the last six months (as of January 05, 2016). The group’s FUA rose 92% during first quarter of 2016 to $1.98 billion while reached $2.23 billion (as of November 25, 2015). HUB’s addressable market, superannuation assets is estimated to double in the next ten years, wherein Wrap Platforms are forecasted as the major growing segments. Accordingly, the group’s management estimates to build $8 billion to $10 billion in FUA by the end of the decade. HUB24 has smaller than 1% market share in Wrap Platform, and intends to enhance its market share in this segment and leverage the growing opportunity.

.png)

Fiscal year of 2015 performance (Source: Company Reports)

Meanwhile, IOOF Holdings made an acquisition proposal of the entire stake of HUB for $2.75 per share price, boosting HUB stock further by 82.4% in the last three months. However, we believe that the recent strong rally placed HUB stock at expensive valuations. Moreover, IOOF Holdings withdrew their acquisition offer and did not negotiate the price beyond $2.75 per share price. We give an “Expensive” recommendation on the stock at the current price, and would review the stock at a later date.

HUB Daily Chart (Source: Thomson Reuters)

ALS Ltd

.png)

ALQ Dividend Details

Boosting Capital Position: ALS Ltd (ASX: ALQ) enhanced its capital position by finishing over $325 million fully underwritten, 5-for-21 pro rata entitlement offer of 96.96 million of new totally paid ordinary shares to eligible shareholders. On the other hand, ALS reported a weak first half of 2016 performance with underlying net profit after tax falling to $61.9 million as compared to $67 million in prior corresponding period. Revenues slightly increased by 0.25% yoy to $712.1 million during the period while oil and gas markets pricing pressure impacted profit margins.

.png)

ALS Life Sciences performance (Source: Company Reports)

Meanwhile, ALS Life Sciences surged 16% on a yoy basis, but the group’s other segments were impacted by tough market conditions. We believe the stock pressure would remain in the coming months given the ongoing tough market conditions. Based on the foregoing, we give an “Expensive” recommendation on this stock at the current price.

ALQ Daily Chart (Source: Thomson Reuters)

GUD Holdings Ltd

.png)

GUD Dividend Details

Subdued consumer sentiment coupled with falling Australian dollar to add pressure: GUD Holdings Ltd.’s (ASX: GUD) management reported that the ongoing falling Australian dollar would impact its margins, as the products need to be bought at decreased currency levels. Moreover, the ongoing subdued consumer sentiment was expected to impact Christmas trading season leading to a weak FY16 performance. GUD reported a revenues increase of 3% to $611.5 million in fiscal year of 2015, against $591.6 million in fiscal year of 2014 on the back of better performance across all of its segments (except Sunbeam). Second half performance was strong in FY15, as compared to the first half and the revenues rose by 7% as compared to prior corresponding period. The group reported a strong bottom line growth and enhanced its attributable profit by 88% yoy to $33.2 million, driven by its efficiency efforts. GUD finished the acquisition of Brown & Watson which would contribute to the group’s automotive aftermarket business.

.png)

GUD Holdings LtdFiscal Year of 2015 Performance (Source: Company Reports)

Based on the foregoing, we give an “Expensive” recommendation to the stock at the current price.

GUD Daily Chart (Source: Thomson Reuters)

Billabong International Ltd

.png)

BBG Details

Weak Outlook: Billabong International Ltd (ASX: BBG) stock plunged 2.16% in the last four weeks (as at January 05, 2016) on the back of a weak outlook by management for fiscal year of 2016. Management reported that the falling Australian dollar is leading to margin pressure for the group in the short term. Moreover, the group’s term debt is denominated in US dollars, and the rising US dollar led to an increase in principal and interest. Billabong International business in North America which includes department stores, big action sports chains, tourist retail and teen retail is also facing performance pressure in North America. The slowdown of the hardgoods market in skate during the initial months of fiscal year of 2016, is estimated to impact the sales of Sector 9 as well as Element skateboards. In addition, consumers are pursuing value shopping and constantly looking for deals, adding more pressure to the group to compromise on margins. Management stated about its EBITDA at $2.5 million during the first four months of FY16 impacted by tough market conditions in America and the mounting foreign exchange pressure on product costs. The company recently announced for the release of 357,143 shares from voluntary escrow arrangements on January 10, 2016.

.png)

Fiscal year of 2015 performance (Source: Company Reports)

Meanwhile, we believe BBG stock pressure would continue in the coming months given the ongoing impact of weak consumer sentiment and falling Australian dollar pressure on the group’s performance. Based on the foregoing, we give an “Expensive” recommendation on the stock.

BBG Daily Chart (Source: Thomson Reuters)

AP Eagers Ltd

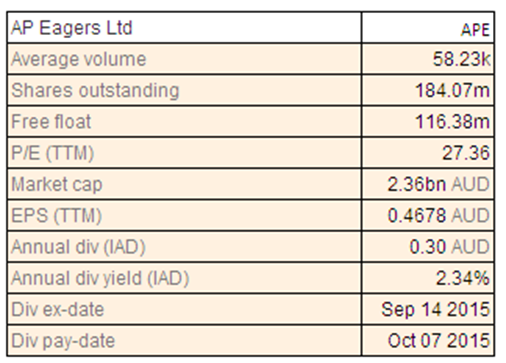

APE Dividend Details

Dependence on Acquisitions to expand business: AP Eagers Ltd (ASX: APE) is acquiring Motors Group Tasmania, Silver Star Motors (Mercedes-Benz) in Doncaster and Burwood, Victoria, coupled with Mercedes–Benz Ringwood dealership in Victoria, and Waverley Toyota in Glen Waverley, Victoria, to boost its car retailing business. The group is investing over $114 million for these acquisitions (inclusive of goodwill and estimated net assets) with the initial consideration to be funded via the issue of 2.2 million shares and the transaction is targeted to be finished by first quarter 2016 and contribute to the FY16 EPS. Meanwhile, APE had delivered strong FY15 performance with the EBITDA growing by 24% yoy to $77.5 million on the back of increase in its core car retailing segment. As a result, APE shares generated outstanding performance during 2015, rallying around 111.67% (as of December 31, 2015). On the other hand, the spurt in the stock has placed it at higher valuations.

.png)

Growth Timeline highlights (Source: Company Reports)

With the current challenging retail market conditions, investors are concerned over its ability to sustain its FY15 growth as well as the group’s reliance on acquisitions to expand business. APE is trading at a relatively higher P/E while has a modest dividend yield. Based on the foregoing, we give an “Expensive” recommendation on the stock at the current price, and would review the stock at a later date.

APE Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.