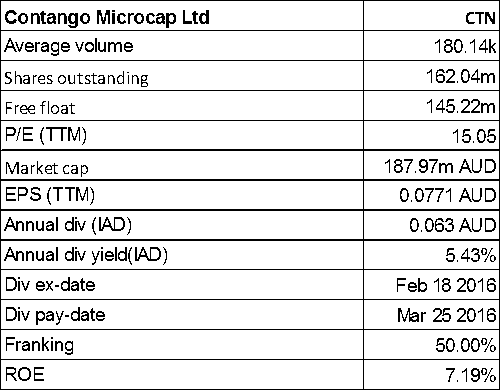

Contango Microcap Ltd

CTN Details

Improving performance: Contango Microcap Ltd (ASX: CTN) stock surged over 23% (as on August 26, 2016) in the last three months driven by the group’s improving assets performance. Net Assets after Tax rose to $190.13m as of July 31

st, 2016 as compared to $179.84m in June 2016. CTN has also realised the equity holding in its subsidiary Contango Asset Management Limited (CAML) sold effective June 30, 2016. The purchase price for CAML has been $13m and this represents profits of $2m to CTN. CAML delivered 15.7% rate of return over last 12 years since beginning. In the above regard, Tyrian diagnostics has signed an implementation agreement to support the management buyout of Contango Asset Management.

Net Tangible Assets, Asset Composition & Investment Portfolio of CTN (Source: Company Reports)

On the other side, the company has strong future position as CTN had earlier mentioned that it has sufficient reserves of $13.9m for the dividends of next two years. Despite the recent stock rally, the group is trading at a reasonable P/E. We give a “Hold” on this dividend yield stock at the current price of $1.16

CTN Daily Chart (Source: Thomson Reuters)

WAM Capital Limited

.png)

WAM Details

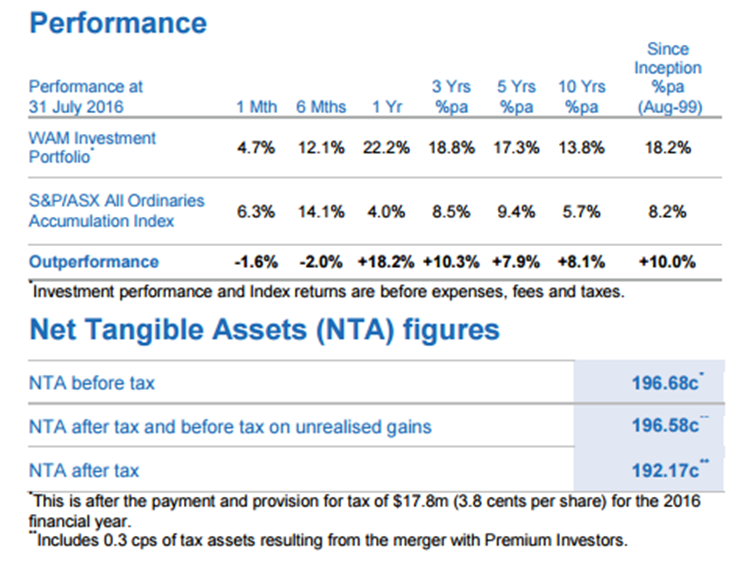

Boosting capital position: WAM Capital Limited (ASX: WAM) recently raised a capital of $247.2m through SPP and the placement was considerably oversubscribed (as on August 22, 2016). WAM raised more than $128.1m through SSP at the fixed price of $2.14 per share and also raised $119.1m through placement with the same terms as SPP. The group also reported a fully franked final dividend of 7.25 cents per share which will be paid in October, 2016.

Investment Update & Net Tangible assets of WAM (Source: Company Reports)

The group’s NTA also increased from July’s number with the pretax NTA rising by $20.0 million or 3.41 cents per share from 196.68 cents per share to a theoretical pre-tax NTA of 200.09 cents per share.

Accordingly, WAM stock rose over 4.2% (as on August 26, 2016) in last three months and still trading at a very cheap P/E. We maintain our “Hold” recommendation on this dividend yield stock at the current price of $2.24

WAM Daily Chart (Source: Thomson Reuters)

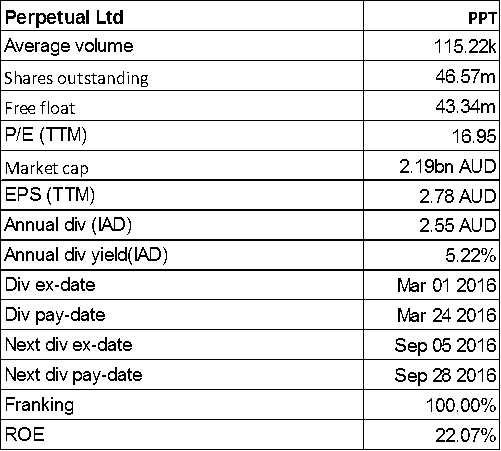

Perpetual Limited

PPT Details

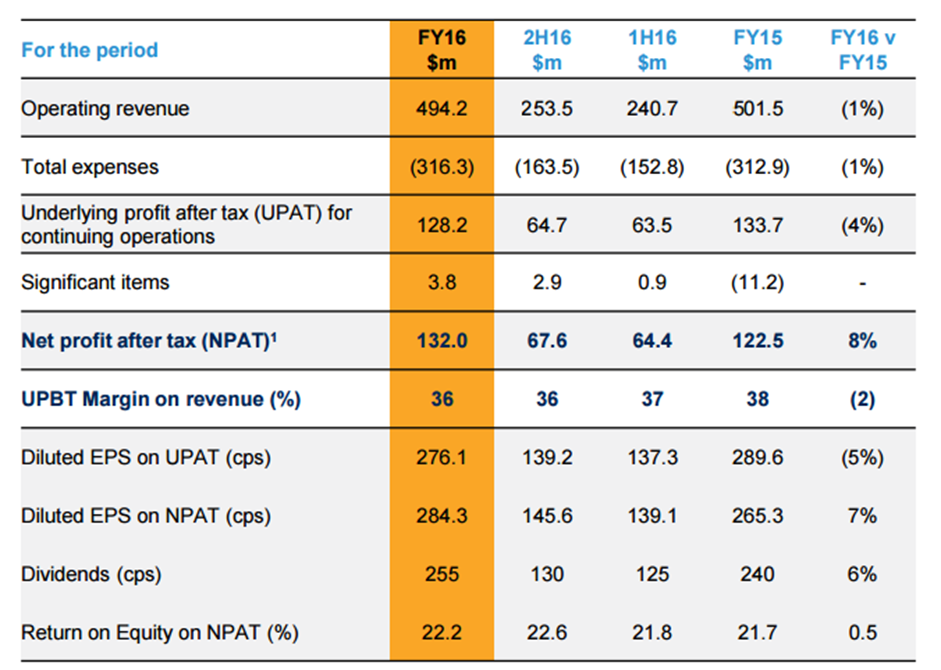

Mixed performance: Perpetual Limited (ASX: PPT) reported a decent FY16 NPAT growth of 8% year on year (yoy) to $132 million in FY16 as compared to the same period of last year while fully franked full year dividend reached 255 cents per share, which rose 6% against FY15. This is the sixth consecutive half wherein the group generated positive net flows driven by net new clients and decent investment performance. On the other hand, the group’s operating revenue fell 1% to $494.2 million in FY16 as compared to $501.5 million in FY15.

Overview of results of FY16 (Source: Company Reports)

The group’s overall expenses also fell, while the cost to income ratio rose to 64% in FY16 against 62% in FY15. The stock has risen over 14.9% in the last three months (as on August 26, 2016) and is trading close to the 52-week high price. We believe that the stock is “Expensive” at the current price of $48.96

PPT Daily Chart (Source: Thomson Reuters)

Magellan Financial Group Ltd

MFG Details

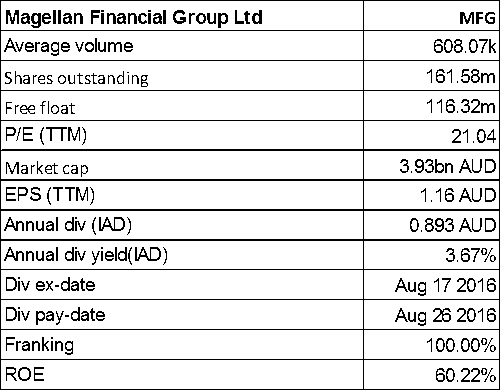

Solid Average Funds under Management performance: Magellan Financial Group Ltd.’s (ASX: MFG) average funds under management rose over 27% to $39.4 billion for fiscal year of 2016 while reported profit after tax was of the order of $198.4m with an increase of 14% on a yoy basis. Whereas, fully diluted EPS of the group was up by 13% to 115.5 cents per share (cps). MFG also declared fully franked (interim & final) dividend of 89.3 cps which grew by 19% on a yoy basis.

MFG Final Results (Source: Company Reports)

The group manages $12b on behalf of their retail investors in Australia & New Zealand and also attracted $2.3b of net inflows during FY16. MFG launched a Colonial First State in May 2016 which is replica version of their infrastructure strategy and helps to boost penetration in Infrastructure.

Magellan also has strong support for ASX quoted funds and replica funds on the AMP and BT/Westpac platforms. We put a “Hold” recommendation on the stock at the current price of $24.18

MFG Daily Chart (Source: Thomson Reuters)

Hunter Hall International Ltd

HHL Details

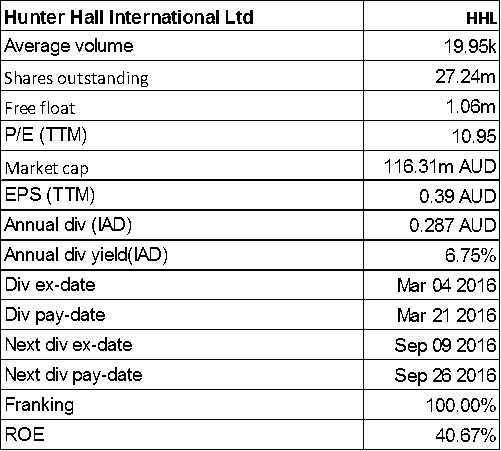

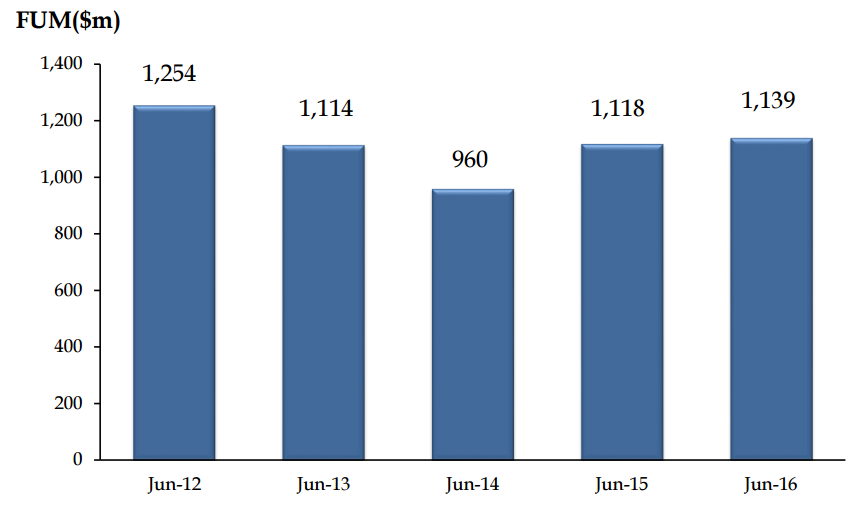

Meek growth for Funds under Management: Hunter Hall International Ltd (ASX: HHL) stated a PAT of $7.8m which is up by 86.8% on a yoy basis. The group got $1.782m in net performance fees from HCT & AVT. HHL also declared dividend of 28.7 cents per share for FY16.

FUM chart (Source: Company Reports)

Operating profit from investment management enhanced 10% on a yoy basis. On the other hand, the company’s funds under management rose only 1.9% to $1.139b from $1.118b in FY15. We believe that stock is “Expensive” at the current stock price of $4.23

HHL Daily Chart (Source: Thomson Reuters)

Henderson Group PLC

.png)

HGG Details

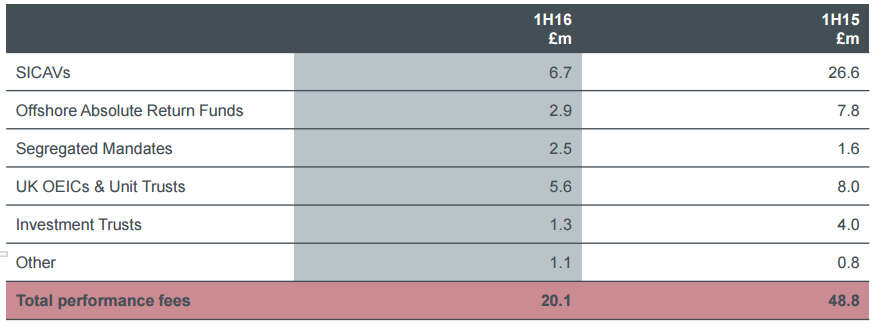

Market uncertainty impacted the performance: Henderson Group PLC (ASX: HGG) asset under management rose just 3% to £95 from £92 in FY15 while the underlying profit before tax fell to £100.5 million as of June 2016 as compared to £117.4 million as of June 2015, as Brexit uncertainty and outcome had impacted the performance.

Performance Fees (Source: Company Reports)

We believe the pressure on the stock would continue in the coming months given the economic conditions at the macro level. Considering all factors, we recommend “Expensive” at the current stock price of $4.20

HGG Daily Chart (Source: Thomson Reuters)

BT Investment Management Ltd

.png)

BTT Details

Expanding geographic diversity: BT Investment Management Ltd (ASX: BTT) reported an NPAT growth of 26% to $78.3m in first half of FY16. The group managed to increase the Funds under management of BTT to $79.7b as of June 30, 2016 as compared to $77.2 billion as of March 2016, which is $2.5 billion rise in FUM. Meanwhile,

BTT is growing their products including Absolute return, and diversified income and demographic changes motivating rising demand of Income products. BTT also declared interim dividend of 18 cents per share in FY16 up by 6%. On the other hand, we believe that the company would continue to face performance pressure in the coming months given the ongoing currency fluctuations coupled with other market challenges. We give an “Expensive” recommendation on the stock at the price of $9.07

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

BTT Daily Chart (Source: Thomson Reuters)

Platinum Asset (Investment) Management Limited

PTM Details

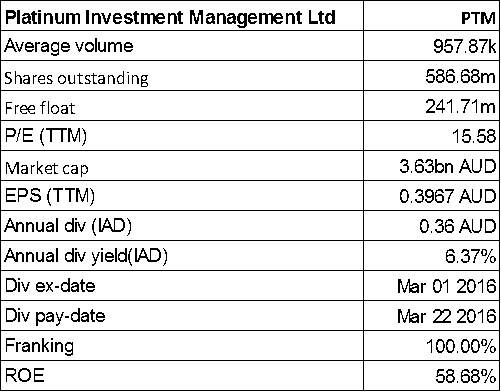

Softness in Performance: Platinum Asset Management Limited (ASX: PTM) reported a weak performance with the fee revenue falling 0.9% to $337.9 million (2015: $340.9 million) on account of average Funds Under Management declining by 1.2% to $25.8 billion (2015: $26.1 billion). As a result, the stock fell over 4.11% in the last five days (as on August 26, 2016). We believe that the group has the ability to recover in the coming months given the expertise of the management. We maintain our “Hold” recommendation on the stock at the current price of –

PTM Daily Chart (Source: Thomson Reuters)

DisclaimerThe advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.