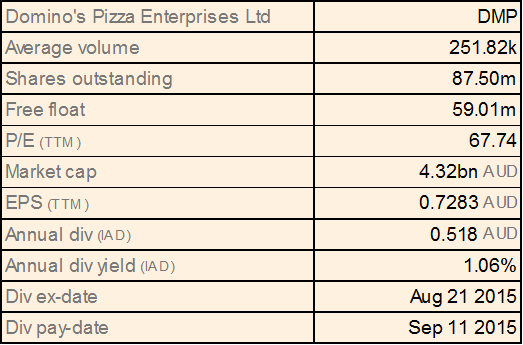

Domino’s Pizza Enterprises Ltd.

DMP Dividend Details

Profit Upgrade and new store openings: The financial highlights by Domino’s Pizza Enterprises Ltd (ASX: DMP) for FY 2015 include a growth of 40% in net profit after tax to $ 64 million, 19.3% growth in revenue to $ 702.4 million, underlying EBITDA growth of 34.4% to $ 127.8 million, strong earnings growth in Australia and New Zealand with double-digit same store growth, unprecedented growth in Europe with EBITDA growth of 92.3%, strong same store growth in both France and the Netherlands including the best first and second half achieved in the past three years and underlying EBITDA growth in Japan of 38%. Shareholders were paid a final dividend of 27.2 cents per share fully franked making a full year dividend of 51.8 cents per share, a growth of 41.1% over the previous year.

Performance (Source: Company Reports)

Clearly, it has been a successful year for the company and the brand is now positioned for more sustained growth. This was a record year for store growth in Australia and New Zealand with a focus on digital innovation and new product launches. Like-for-like sales growth in Australia and New Zealand was 11.3% largely because of Pizza Mogul and Value Range. Europe showed same store sales growth of 6.4% and the Pizza Chef platform was introduced in Europe, the Online Ordering System in Belgium and Quick Ordering in the Netherlands. One of the biggest drivers of same store growth achieved in this market was product innovation. In Japan, 64 new stores were added during the financial year and same store growth was 1.8% in line with management expectations. The new HTML 5 platform was launched. The group store focus saw 177 new stores being added to the group and other key milestones included the 1500

th store opening in just over six months from the 1400

th store opening. The first quarter same store results for the first 18 weeks of FY 2016 were 13.9% growth for Australia and New Zealand, 7.7% for Europe, 0.7% for Japan and 10.5% for the group.

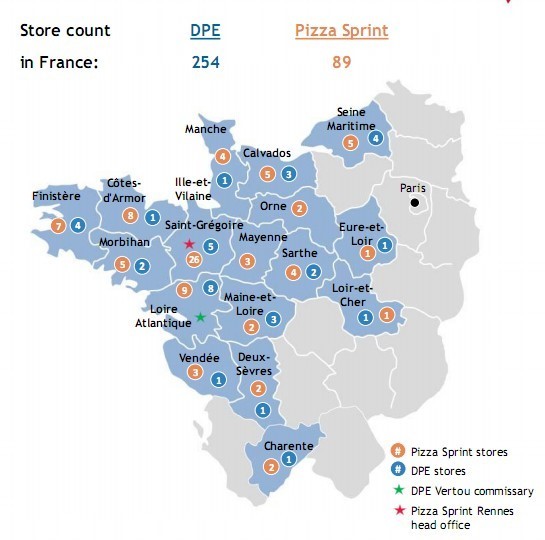

Locations (Source: Company Reports)

The company has provided an upgraded guidance for FY 2016 with EBITDA and Net Profit after Tax guidance to be up in the region of 25% on the underlying. ANZ same store sales guidance is upgraded to 9% to 11%, Europe same store sales guidance is upgraded to 6% to 8% and same store sales guidance in Japan remains unchanged. As of today, the company has 1544 stores and new store openings have been upgraded to the range of 260 stores to 280 stores (including Pizza Sprint stores) across the group. The long-term store count in Europe is being upgraded from 1350 to 1500. The FY 2016 outlook for ANZ includes 40 new digital projects to be delivered and investment in high-tech energy-efficient smart ovens. The outlook for Europe includes the rollout of the global online ordering platform in France and plans to launch SMS ordering. The outlook for Japan is the introduction of "Line" ordering and a rapid store growth plan.

Stock Performance: We believe that the company has delivered solid financial results for FY 2015 and that the momentum is likely to carry through in FY 2016 and beyond.

However, the stock is trading at its 52-week high price and a P/E ratio of about 67x, and seems to be expensive at the current price.

DMP Daily Chart (Source: Thomson Reuters)

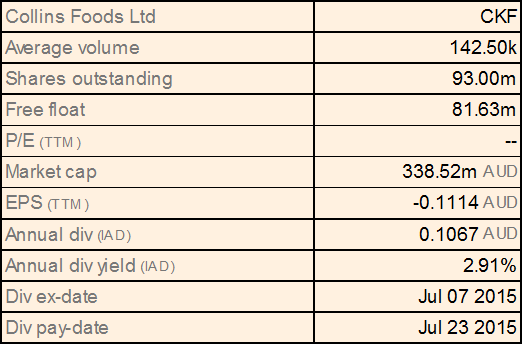

Collins Foods Ltd

CKF Dividend Details

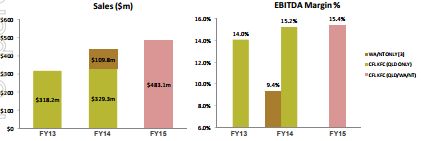

New stores, cash generation and positive FY15 result: Collins Foods Ltd.’s (ASX: CKF) financial results for FY 2015 shows growth of 34.4% in underlying revenues to $ 571.6 million, 37.4% in underlying Net Profit after Tax to $ 24.6 million and 37.5% in EBITDA to $ 67.4 million. ROCE was up by 2.5% to 12.9%, net debt was down to $ 122.8 million resulting in an improvement in net leverage ratio to 1.83, the underlying EPS was 26.4 cents per share and the net cash flow $ 4.9 million, the final dividend was 6.5 cents per share fully franked making a full year dividend of 11.5 cents per share an increase of 9.5% over the previous year. Pre-tax non-cash impairment charges were $ 38.3 million comprising of $ 37.5 million for Sizzler and $ 0.8 million for KFC. The underlying revenue was up 46.7% with same store sales up 4.8%. Six new restaurants were built with 16 others undergoing major remodels. A disciplined focus on cost control resulted in improvements in EBITDA margins which at 15.4% were up 20 basis points and EBIT margins at 11.8% were up 40 basis points. The KFC brand was supported by compelling core products as well as great brand building with a focus on customer experience to drive topline growth and investment in growth oriented assets.

Sales and EBITDA Margin % (Source: Company Reports)

The Sizzler Australia brand is now regarded as non-core to strategic growth and a limited number of restaurants will be closed in FY 2016 with an estimated impact on earnings of $ 0.9 million. No further growth capital will be invested and the remaining restaurants will be closely monitored with a view to taking appropriate action as and when necessary. Sizzler Australia is forecast to generate a positive EBITDA in FY 2016 and Sizzler Asia which is not included in the review will continue to operate as normal. Strong cash generation is supporting a strong balance sheet and cash flow was positive at $ 4.9 million. Net operating cash flows before interest and tax was up by $ 13.5 million due to the strong effect of EBITDA offset by a working capital increase. Tax payments increased by approximately $ 6.8 million and the instalment rate in FY 2014 was low because of the lack effect of IPO costs of approximately $ 2 million. Tax instalments which changed from monthly to quarterly resulting in a negative effect of roughly $ 2 million while the rest of the tax increase was because of improved financial performance and acquisition. Capital expenditure increased by $ 11.9 million over the previous year but was in line with budget.

Looking to the future, there will be a continued disciplined focus on the KFC business with eight new stores being built and major remodels on 18 more. There will also be a continued focus on margin improvements in WA/NT and continued refinement of the Snag Stand concept with further investment. Group capital investment will be in the region of $ 33 million and the dividend policy will be to payout 50% of Net Profit after Tax excluding KFC in WA/NT.

Stock Performance: The results were above our expectations and it is heartening to see that something concrete is being done about Sizzler which is a drain on the rest of the group.

However, the stock is trading close to its 52-week high price, and we believe that the stock is expensive at the current price levels and do not recommend an investment at the moment.

.png)

CKF Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.