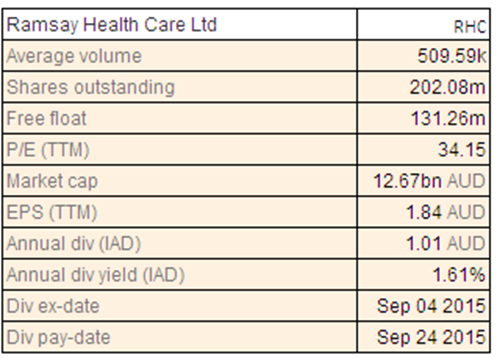

Ramsay Health Care Ltd

RHC Dividend Details

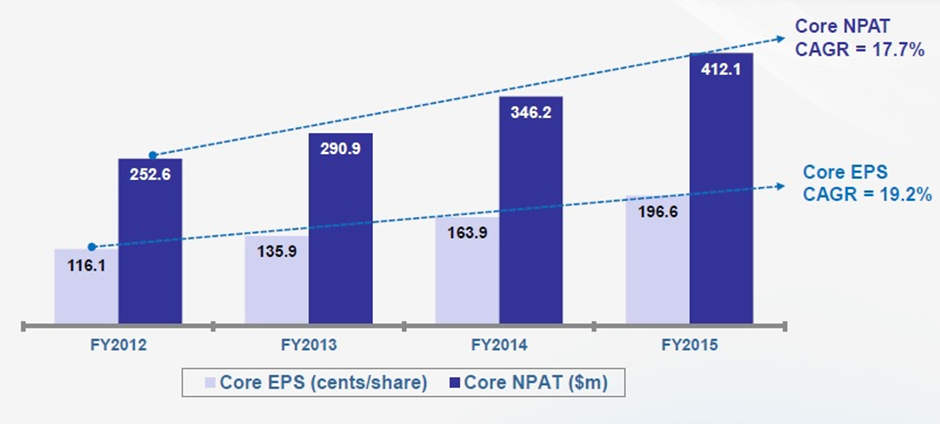

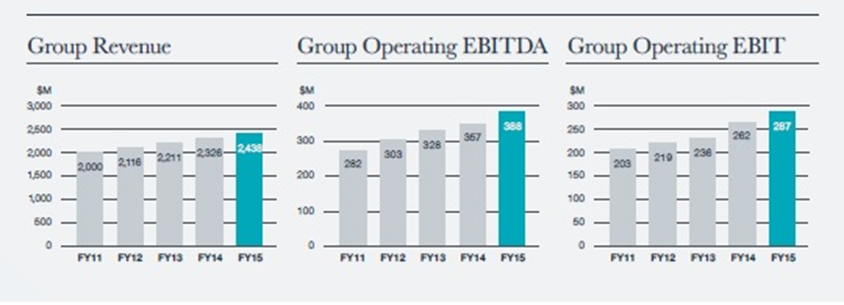

Acquisition growth:For the financial year 2015, Ramsay Health Care Ltd (ASX: RHC) recorded a growth of 19% to $412.1 million in its net profit after tax while earnings per share rose 20% to 196.6 cents. The group's revenue increased 49.8% to $7.4 billion while EBIT rose 37.4% to $803.9 million. RHC declared final dividend of 60.5 cents fully franked, up 18.6% from previous year. Meanwhile, Ramsay is expanding its business and completed $190m worth of expansions at existing facilities during FY15. The group also approved a further $197 million in redevelopments across the group. Recently, Ramsay Générale de Santé announced that following regulatory approval for the acquisition of the HPM Group, consisting of 9 hospitals in Lille France, completion of the acquisition has now occurred. With this acquisition, Ramsay Générale de Santé’s expanded presence in the greater Lille area which will now comprise 11 facilities with 2,180 employees, 700 doctors and is expected to treat approximately 160,00 patients per annum. The purchase price was an enterprise value of €169.5 million, the consideration being a combination of Ramsay Generale de Santé’s cash on hand, draw-down of its debt facilities and the assumption of HPM Group’s external debt. The HPM Group will be fully integrated into the Ramsay Générale de Santé Group.

Growing NPAT (Source: Company reports)

Besides, Ramsay's Malaysian affiliate Ramsay Sime Darby Health Care (RSD) has entered into a Framework Agreement to establish a joint venture with Jinan University No.1 Affiliated Hospital. Given strong industry fundamentals, continuing implementation of its successful growth strategy and barring unforeseen circumstances, Ramsay is targeting core NPAT and core EPS growth of 12% to 14% for FY 2016. The stock has risen 5.96% in the last one year (as at January 18, 2016). We rate this stock a BUY rating at the current share price of $61.12

RHC Daily Chart (Source: Thomson Reuters)

Japara Healthcare Ltd

.png)

JHC Dividend Details

Booming aged care demand drove the group’s performance:Japara Healthcare Ltd (ASX: JHC) delivered a better than estimated EBITDA guidance (of $50.3 million) at $50.6 million, an increase of 26.5% during full year 2015 financial results against previous year. Revenue rose 14.8% to $281.3 million with occupancy at 94.6% compared to 93.9% in previous year. Net profit after tax stood at $28.8 million. Refundable Accommodation Deposit (RAD) inflows increased significantly to $77.3 million compared to only $24.3 million in 2014 led by aged care reforms which enabled the company to charge RADs on a higher number of places. The company's Whelan Care acquisition contributed strongly in financial year 2015, while in financial year 2016 contribution is foreseen to be higher than $5 million. Meanwhile, Profke, another acquisition, is expected to contribute operating EBITDA between $3.5 and $4.0 million in FY16. The Profke acquisition was recently completed for $79.5 million which comprises of four aged care facilities and 587 beds in Queensland and New South Wales. The acquisition provides Japara Healthcare with a strategic presence in the Queensland market and a platform for greenfield expansion in the region. Looking ahead, the financial year 2016 results are expected to exceed financial year 2015 results mainly led by increases in average Aged Care Funding Instrument (ACFI) per resident from higher care delivery, brownfield/greenfield developments providing an increase in operational bed days and higher revenue from significantly refurbished facilities.

.png)

Result summary (Source: Company reports)

Japara’s aged care business is a strong generator of cash which supports high dividend payout ratios. JHC intends to continue to pay up to 100% of profits as dividends to shareholders, and moving forward, frank those dividends to the maximum extent possible. With a decent dividend yield, we rate this stock a BUY at the current share price of $2.89

JHC Daily Chart (Source: Thomson Reuters)

Healthscope Ltd

.png)

HSO Dividend Details

Increasing beds and Theatres to leverage the opportunity: Healthscope Ltd (ASX: HSO) recently announced financial year 2015 results in line with prospectus forecast. Group operating EBITDA, EBIT & NPAT all stood 0.3%, 0.8% and 4% above prospectus forecast. Meanwhile, group operating EBITDA and EBIT increased 8.7% and 9.4% respectively over the previous year. Revenue rose 4.8% led by strong growth in hospitals and international pathology. Cash conversion ratio stood at 97.3%. Recently, HSO appointed Paul O' Sullivan as its non executive director and expects to gain significantly from his deep operating experience with Optus and Singapore Telecommunications both in Australia and Asia. Meanwhile, in November 2015, HSO announced that it has issued almost 3 million fully paid ordinary shares at an issue price of $2.72 per share as part of the consideration for the acquisition of 100% of The Hunter Valley Private Hospital Pty Ltd (HVPH). Total consideration for the acquisition of HVPH is $71.3 million, comprising $63.1 million in cash proceeds and $8.2 million in the form of shares. The acquisition of HVPH will complement Healthscope’s existing portfolio in New South Wales, following which the company will operate 46 hospitals throughout Australia. Looking ahead, hospital expansion programs are on track with 10 projects under construction and five projects approved which will deliver over 980 new beds and 50 new theatres by the end of calendar year 2018.

Financial overview (Source: Company reports)

Strong cashflow and balance sheet is likely to support pipeline of growth opportunities and HSO targets dividend payout ratio of 70% of NPAT. During the second half of financial year 2016, HSO will also commission some large capital projects (Gold Coast, Knox, and National Capital) which will lay the foundation for accelerated growth in financial year 2017 and beyond. Given the above, we rate this stock a BUY at the current share price of $2.40

HSO Daily Chart (Source: Thomson Reuters)

Virtus Health Ltd

.png)

VRT Dividend Details

Focusing on International expansion: Virtus Health Ltd (ASX: VRT) reported its full year 2015 results with revenue soaring 16.1% to $233.7 million driven by growth in Ireland and Singapore and 15,100 fresh cycles performed during the year. Group EBITDA grew 3.3% to $61.4 million out of which Australian segment EBITDA increased 1.9%. Net profit after tax adjusted pre-minorities increased 5.1% to $33.6 million. Virtus expected to have full contribution from the acquisitions and Greenfield in financial year 2015. Besides, the company looks for international expansion - UK an attractive market for a buy and build strategy, South East Asian markets under review; Australia – selective greenfield investment and/or in-fill acquisitions for ARS and day hospitals.

.png)

Operational highlights (Source: Company reports)

Also, it seeks to invest in diagnostic capability, increase utilisation across infertile and fertile patients, actively identify and grow new ARS customer segments. Meanwhile, in light of expanding its diagnostic services (revenue for FY15 up 14.6%), Virtus recently acquired the business and certain assets of Independent Diagnostic Services (IDS). VRT stock has corrected about 28.97% in the last one year (as at January 18, 2016). With a good dividend yield, we rate the stock a BUY at the current share price of $5.65

VRT Daily Chart (Source: Thomson Reuters)

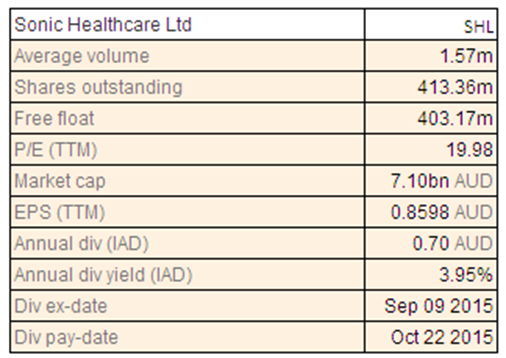

Sonic Healthcare Ltd

SHL Dividend Details

Government healthcare reforms and organic growth: Sonic Healthcare Ltd (ASX: SHL) recently commented that post the Australian government mid-year economic and fiscal outlook, which included the unexpected announcement of Australian Medicare fee cuts to laboratory and imaging services, effective 1 July 2016, the company estimates that this would impact Sonic Healthcare’s Australian laboratory revenues by approximately 3.5% and Sonic’s imaging revenues by approximately 2.7%, with a total revenue impact of approximately A$50 million per annum. With no mitigating actions at all, the impact on Sonic’s total EBITDA would be in the order of 5%-6% for the FY2017 year. Earlier, the company stated that EBITDA for full year 2016 is expected to be around A$ 815 to A$ 840 million at constant currency rates, growth seen exceeding 20%. Strong growth was said to be expected in specialist and esoteric markets, including genetics in 2016. For full year 2015, revenue grew 7.3% to A$ 4,201 million from previous year driven almost 5% growth enhanced by accretive acquisitions.

While Germany, UK and Switzerland recorded strong growth, the U.S. markets are also strengthening. Total dividends paid in FY15 rose 4.5% over the previous year. However, we believe that the stock is trading at an expensive valuation and is overvalued at the current share price.

SHL Daily Chart (Source: Thomson Reuters)

Capitol Health Ltd

.png)

CAJ Dividend Details

Targeting Organic growth: Recently, Capitol Health Ltd (ASX: CAJ) entered into a memorandum of understanding with Enlitic LLC to commercialize Enlitic's deep learning and artificial intelligence protocols in radiology and healthcare. The agreement delivers Capitol exclusive use of Enlitic in Australia and provides for collaboration on international deployment. Capitol has made a partnership investment of up to $10 million expecting to potentially yield revenue and expenditure benefits during financial year 2017. For financial year 2015, CAJ recorded a growth of 23% in its revenue to $111.2 million compared to previous year. Net profit before tax (NPBT) margin expanded 325 basis points to 14.5% while NPBT increased 59% to $16.2 million. Underlying EPS stood at 2.49 cents, compared to 1.68 cents in year ago. Looking ahead, Capitol estimates strong performance to be maintained in financial year 2016 with focus on integrating acquisitions and driving synergies and network benefits. Government initiatives are seen supporting further organic and acquisitive growth of the company thereby driving revenue and profits.

However, impact from the government mid-year economic and fiscal outlook is yet to be ascertained while the company is trying to fetch more details. On the other hand, CAJ board remains committed to a Progressive dividend policy supported by strong cash flows. With a good dividend yield, we rate this stock a BUY at the current share price of $0.17

CAJ Daily Chart (Source: Thomson Reuters)

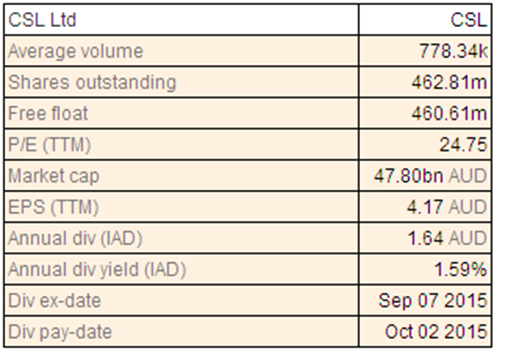

CSL Ltd

CSL Dividend Details

Strong cashflow: Recently, CSL Ltd (ASX: CSL) announced a new on-market share buyback of up to A$1 billion, the largest ever undertaken by the company as part of its regular buyback program. Through its previous buybacks, CSL has purchased 23% of its shares at some A$ 5.16 billion, contributing to a 23% increase in earnings per share. The company believes that another buyback indicates CSL's strong financials and cashflow. Also, this helps the company to increase shareholder dividends and invest in manufacturing expansions and innovation. Company CEO comments that earnings per share growth this financial year will again exceed profit growth expectations as shareholders benefit from the ongoing effect of past and current share buybacks. For full year 2015, CSL recorded a net profit after tax of $1,379 million, an increase of 6% on reported basis from the prior comparable period. Sales increased 2% while EBIT was higher by 7% for the same period. Also, with its latest acquisition of Novartis influenza vaccines business, the company is now the second largest influenza vaccine manufacturer in the world. Looking ahead, CSL expects strong underlying demand for its products to continue in FY16, with sales growth similar to gains achieved in FY15.

Net profit after tax is expected to grow by around 5% with earnings per share growth to exceed profit growth. This does not include the gain on acquisition, integration costs and operational contribution from Novartis deal. With high P/E ratio, we rate this stock "Expensive" at the current share price.

CSL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.