With latest news on government tightening the rules in the telco sector and National broadband network customers getting the flexibility to request speed tests from their internet provider, the telco sector companies were again under spotlight in the month of December. With some ups and downs in the nbn roll-out, it will be worth to keep a watch on the following key stocks –

Telstra Corporation Limited (ASX: TLS)

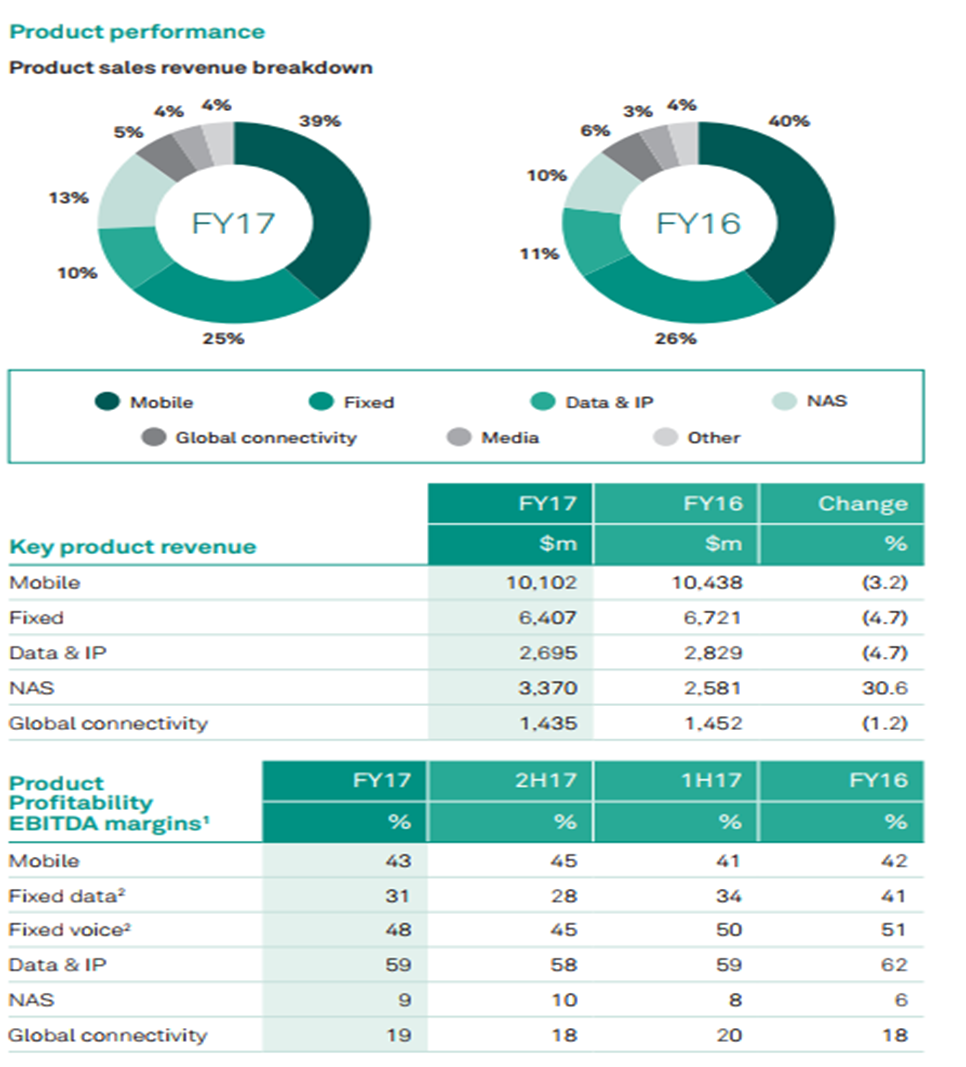

NBN Rollout delay impacts 2018 outlook: The outlook for Telstra has been on the brim with market expectations that its mobile business is under some pressure. 2017 has been a rough year as its share price crashed by nearly a third. It has been stated that ALDImobile uses Telstra’s network and the margins which Telstra is making are less appealing than that from signing up customers directly. Recently, it was reported that Telstra revised its full-year guidance to a lower level because of NBN delays. As per the revised guidance, TLS FY18 total income is expected to be $27.6b to $29.5b after $0.7b reduction, EBITDA to be $10.1b to $10.6b after $0.6b reduction, and free cash flow to be $4.2b to $4.7b after $0.2b reduction at the back of the delay in nbn co.’s hybrid fibre co-axial technology for six to nine months from December 2017 and nbn’s Corporate Plan 2018. On the other hand, it is expected that the rollout of 5G will bring TLS back on track in terms of competition. However, 5G is not expected to enter Australia until 2020, thus TLS has a long-way to benefit from the scenario. In the past one year, the stock price decreased by 28% but rose over 5.49% in the last one month (as at December 27, 2017). We give a “Hold” at the current price of $3.68, until new growth pillars are found to support the stock momentum.

Product Performance (Source: Company Reports)

Vocus Group Ltd (ASX: VOC)

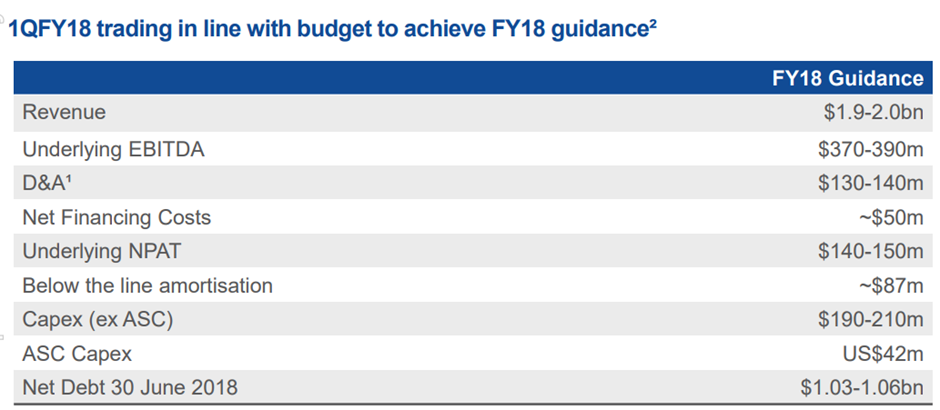

FY18 Guidance Confirmed: In the recent trading update, Vocus announced that consumer NBN share rose from 7.3% to 7.8% and consumer brands (dodo and iPrimus) contributed to 9.25% share of all NBN orders, as at first quarter 2018. Vocus Communication energy services were also launched which targeted SMB segment. Assuming Vocus successfully migrates all existing copper broadband subscribers to the NBN so CPE (Customer Premise Equipment) migration capex is expected to be approximately $22.7 million over the period FY18 and FY20. Enterprise and Wholesale division continues to focus on reducing the capital expenditure which is associated with new connections focusing on the market activities. It also announced its plans to offload its New Zealand based consumer Internet business and if the Company finds a prospect buyer, it will use its proceeds to pay its debt and had appointed Bain Corp for helping it in implementing its ongoing transformation program.VOC expects its FY18 revenue to be between $1.9 billion and $2 billion; underlying earnings before interest, tax, depreciation and amortisation of between $370 million and $390 million; and underlying net profit of between $140 million and $150 million.VOC also secured 4 out of 4 Federal business tenders in 1QFY18 and two more tenders have been said to be secured in 2QFY18. The share price has got some boost recently; and as per the recent guidance, some more positive developments are expected. We give a “Hold” on the stock at the current price of $3.10

Trading Guidance (Source: Company Reports)

TPG Telecom Limited (ASX: TPM)

Year to date performance tracking well: It was reported that at the end of FY17, TPM’s broadband subscribers have risen to 1.94 million. Its operating cash flow also increased from $759.2 million to $869.7 million and the debt balance decreased from $1350 million to $900 million. After the year end in September 2017, the group increased its total committed debt facilities to finance its planned mobile network builds and it increased its total facilities by $750 million to $2,385 million. Capital expenditure expectations regarding both in Singapore and Australia mobile networks builds were also unchanged and the company is expected to make a spectrum payment of $595 million in relation to Australian 700MHZ spectrum in FY 18. TPM’s Singapore project is also on track to achieve the nationwide outdoor service coverage by December 2018, in compliance with FBO license obligations. Its network deployment strategy provides coverage and capacity to densely populated areas by utilising both its 700MHZ and 2600MHZ spectrum and extensive fibre assets.Agreements with multiple partners in Australia for mobile network rollout for small cell and macro network have been put in place. It is expected that EBIDTA will be in the range of $800 million -$815 million in 2018. With the earnings per share coming in at 47.9 cents in FY17, its shares change hands at a trailing 13x earnings, which is a reasonable level. We give a “Buy” recommendation at the current price $6.65

Growth Summary (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.