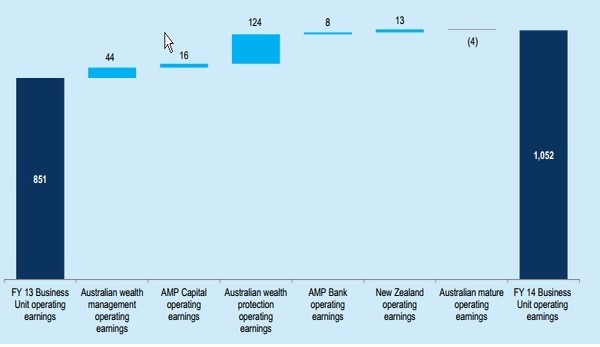

AMP Limited (ASX: AMP) touched a fifty two high of $6.8 during Feb, after delivering better than expected full year fiscal 2014 results. AMP reported a 25% increase of total operating earnings to $990 million in fiscal year 2014, as compared to $789 million in fiscal year 2013.

SMSF market opportunity

AMP Limited had recently reported the acquisition of Justsuper, SMSF administration business to boost its market share in Australia’s $500 billion SMSF sector. Justsuper holds more than 1,000 funds under administration, and through this acquisition, customers can leverage the broader range of market leading SMSF administration platforms from Justsuper and also have access to AMP SMSF’s technical experts.

Operating Earnings (Source - Company Reports)

Operating Earnings (Source - Company Reports)

Based on the SMSF Investment Patterns Survey, SMSF trustees have been improving their portfolio diversification through a significant increase in allocation in international shares during the first quarter of the year. The managed funds continue to be the desired option to invest overseas with 88.2% of trustees investing in pooled structures, as investing directly in the overseas is quite complex. The holdings in international shares have improved by 1.9 percentage point to 14.4% during the quarter. On the other hand, the flow of funds into international shares has witnessed a decrease of allocation to Australian equities to a year-low of 38.6% in March 2015 quarter, as compared to 41.6% during the previous quarter.

Accordingly, the representation of top 10 stocks in SMSF portfolios has decreased from 19 % to 16.8% during the first quarter of 2015. The average pension payment made by SMSFs also dropped in to $11,588 in March 2015 from $21,105 in December 2014. Over 37% of the entire property holders had gearing arrangement in place, against 35.9% in the last quarter. Meanwhile the average loan amount for property purchases rose $10,000 during the March quarter as compared to the previous quarter to $273,000.

Other highlights

As per the recent highlights, AMP Capital as well as 3i Infrastructure have entered into an agreement to acquire 100% share of Danish company ESVAGT from Maersk Group. AMP Capital would be infusing funds of worth of around £109 million to get a 50% interest in ESVAGT while 3i Infrastructure would get the remaining share. Esvagt is based in Esbjerg and offers emergency response and rescue services in the offshore oil and gas industry in Denmark and Norway as well as expanding penetration into UK and offshore wind services segments. AMP Capital can now enter the Scandinavian markets which otherwise has high barriers to entry and the firm believes that Esvagt could be best fit for the company’s Global Infrastructure Fund.

AMP Capital’s global infrastructure platform raised funds from global investors and has secured commitments in excess of US$1 billion. The platform intends to achieve a final close of US$2 billion, while the completion of the transaction remains conditional upon receiving clearance from the European Commission under the EU Merger Regulation. Meanwhile, AMP Capital has given the Stage 2 Development Application for the commercial office tower within its landmark Quay Quarter Sydney precinct in Circular Quay. The total project value is worth over $1 billion.

Guidance

AMP capital intends to achieve $200 million pretax run rate savings by the end of 2016 through its business efficiency program. The group expects the fiscal year 2015 underlying cost growth in the range of 2.5% to 3% prior to the expected efficiency program benefits of $50 million. The business efficiency program pretax costs is estimated to be $90 million in FY15 and $31 million in FY16. The group’s business efficiency efforts is expected to deliver a cost benefit to P&L of $69 million and $138 million in FY15 and FY16 respectively. Cost to income ratio target is at the lower end of the range 60% to 65% over the medium term.

.png)

Business efficiency program (Source: Company Reports)

With regards to the wealth management outlook, the division’s MySuper Plan transition is ongoing. The company forecasts the average margin compression of over 4.5% per annum by June 2017. Margin compression might reduce to the longer term average, after the MySuper transition period. The group intends to achieve a long term lapse rate of over 13.5% by FY17. AMP capital estimates to maintain its payout ratio in the range of 70% to 80% of the underlying profit. The company declared an 80% franked dividend of 13.5 cents per share, resulting to a payout ratio of 74% of underlying profits.

.png) AMP Daily Chart (Source - Thomson Reuters)

Outlook

AMP Daily Chart (Source - Thomson Reuters)

Outlook

After touching a five year high of $6.83 during February, the stock could not able to sustain these levels, and have been declining by approximately 4.85% in the last three months. Despite having a dividend yield of 4.08%, the stock is trading at a relatively high P/E of 21.23x, as compared to its industry peers. Moreover management had admitted that the financial advice industry had been challenging, while the insurance business is still on the recovering mode. Apart from its business efficiency program, AMP capital’s management have not implemented any solid efforts to boost its business in the long term. Given the tough market conditions, and relatively higher valuations, we believe the stock is “

expensive” at the current price of $6.37.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376