Woodside Petroleum Limited

-

Enhancing resource potential and productivity: Woodside Petroleum Limited (ASX:WPL) reported an operating revenues decline by 28% to $2,556 million in 1H15, against $3,551 million in 1H14 impacted by the falling oil prices. The group’s reporting profit slumped 38.6% yoy to $679 million, and accordingly WPL decreased its dividends by 40.5% yoy to 66 cents per share during the first half of 2015. On the other hand, WPL is focusing on productivity costs and targets to achieve $800 million of enduring benefits by 2016. The group finished acquiring interests in Wheatstone LNG, Kitimat LNG and Balnaves oil projects during April 2015. Consequently, the proved (1P) developed and undeveloped reserves rose by 18.3% to 191.8 mmboe, while the proved plus probable (2P) developed and undeveloped reserves grew by 19.5% to 260.9mmboe. The Contingent resources (2C) surged by 151% to 2,632.0 mmboe. Meanwhile, the group’s joint venture partner, Browse entered into the front-end engineering and design (FEED) phase for the planned floating LNG development. WPL is enhancing the NWS Project value and developing the Julimar Project which is estimated to be ready by second half of 2016

Exploration Acreage (Source: Company Reports)

-

Stock Performance: Woodside Petroleum stock slumped by 12.2% over the last four weeks (from Aug 6 to Sep 4), as its revenues were impacted by the falling oil prices. However, Woodside is making efforts for cost optimization and maximizing utilization from its present assets. The stock is trading at a very cheaper P/E of 8.85x and has a huge dividend yield of 9%. Any recovery in oil prices would also drive the stock higher, and accordingly we give a “BUY” recommendation to the stock at the current price of $29.95.

.PNG) Finbar Group Limited

Finbar Group Limited

-

Received approval for springs rivervale project: Finbar Group Limited (ASX: FRI) recently received a development approval for its new Springs Rivervale Joint venture project, which has 183 one, two and three bedroom apartments with amenities. The project also comprises seven ground floor commercial lots for entire Springs area. The group has 50% interest in the project profit which has an end value of around $97 million, and would also earn project management fee. The project’s marketing is estimated to be launched by the end of the year. Meanwhile, Finbar also acquired four vacant lots at Springs through its wholly owned subsidiary for $5.15 million for merger and redevelopment, to develop over 185 apartments within a 10 level building. The project end value is forecasted over $83 million. The group also received development approval for JV project at West Perth, which has 242 apartments with amenities and 2 commercial lots. FRI has 50% interest in the project’s profit, while the end value of the project is over $125 million. On the other hand, Finbar Group’s performance has been under pressure with the group’s profit after tax declining to $25.9 million for the fiscal year of 2015, from $40.9 million in FY14.

Springs Rivervale Project (Source: Company Reports)

-

Stock Performance: Finbar Group shares corrected over 9.5% in the last four weeks (Aug 7 to Sep 4) on the back of its earnings pressure. However, investors need to note that the group achieved a record pre-sales level of over $408 million and has a $2 billion project pipeline to boost its future profit growth. The recent project approvals at Springs Rivervale and West Perth, would also add support to the stock in the coming months. Finbar Group is trading at a cheaper valuation with a P/E of 10.03 x and has a huge dividend yield of 8.7%. We recommend a “BUY” on the stock at the current price of $1.12.

Insurance Australia Group

Insurance Australia Group

-

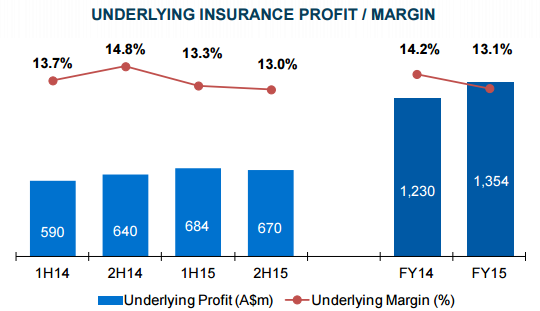

Disappointing FY15 Performance: Insurance Australia Group Ltd (ASX:IAG) gross written premium improved by 17% to $11.4 billion during fiscal year of 2015, as compared to $9.8 billion in FY14, partly driven by the first time volumes contribution from former Wesfarmers business. However, the group’s Insurance profit fell to $1.1 billion during the year, as compared to $1.6 billion in FY14, impacted by the severe peril outcome resulting in a net cost of $1.048 billion against the $700 million allowance. TC Marcia and east coast low impact during second half of 2015 also led to the Insurance profit decrease. Even the underlying insurance margin decreased to 13.1% in FY15 from 14.2% in pcp due to lower margin Wesfarmers business and challenging market conditions. On the other hand, the group improved its cash return on equity to 15.3%, which is ahead against the 15% long term target. The group also declared a fully franked dividends of 29 cents during the year, from 14.4 cents in FY14. Accordingly, the dividend payout ratio improved to 70.2% of cash earnings from 69.9% of cash earnings in FY14.

Underlying performance (Source: Company Reports)

-

Stock Performance: IAG formed strategic relationship with Berkshire Hathaway, entering into 20% quota share agreement across the group’s insurance business to decrease its earnings volatility and capital requirements for the next ten years. However, the stock fell more than 15.5% in the month (Aug 6 to Sep 4) due to its poor earnings performance and unexpected increase in severe peril outcomes in the second half of the year. But IAG is trading at a relatively attractive P/E of 16.35x, and has a strong dividend yield of 5.8%. Given its long term potential, we reiterate our “BUY” recommendation on the stock at the current price of $5.04.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.