Chevron Corp

CVX Details

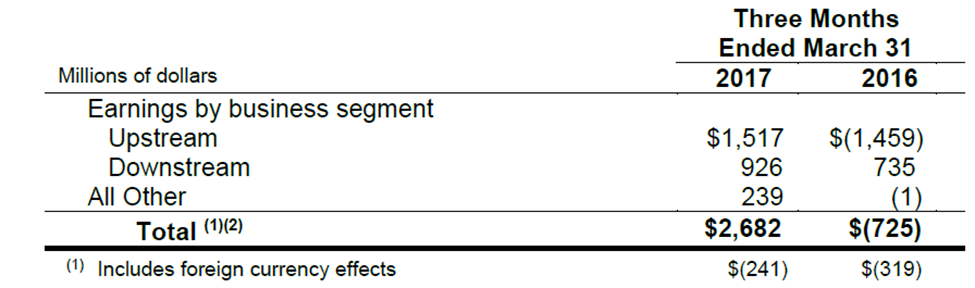

Earnings driven by increased crude oil realizations:Chevron Corp (NYSE: CVX) has recently witnessed a pull back from its investors as they withdrew a proposal related to the company reporting on the risks from policies to address climate change. On the other hand, CVX recently announced for significant non-core asset sales with streamlining in overall operations. During Q1FY17, Chevron’s revenue grew by 39.1% year on year (yoy) to about $32 billion, while earnings stood at $2.7 billion (against a loss of $725 million in Q1FY16) led by higher crude oil realizations, gain of ~$600 million from the sale of the Indonesia geothermal business, higher natural gas sale volumes and lower operating expenses. Foreign currency effects, however, reduced earnings in Q1FY2017 by $241 million against a decrease of $319 million in Q1FY16. The average sales price for crude oil was $49 per barrel against $29 in Q1FY16 and the average price of natural gas was $4.36 per thousand cubic feet, compared with $3.91 in Q1FY16. Further, cash flows improved significantly benefitted by increasing crude oil prices in international upstream division and ongoing efficiencies implemented across the company. Importantly, CVX has continued to make substantial progress on reducing spending and the operating expenses slipped by 14% yoy in Q1FY17 and capital spending declined over 30% yoy. Further, the company started several new projects while progressing on asset sales. Overall net oil-equivalent production in Q1FY17 increased 3% compared to the 2016 full year and looks to be on track to meet the 4-9% target for 2017. Recent milestones include commencement of production from the main facility of the Mafumeira Sul Project in Angola while achieving first LNG from Train 3 at the Gorgon Project in Australia. Further, the group announced an agreement to sell the upstream operations in Bangladesh and signed an agreement to sell refining and marketing assets in British Columbia and Alberta.

Q1FY17 earnings break-up (Source: Company reports)

Cash flow from operations in Q1FY17 stood at $3.9 billion against $1.1 billion in Q1FY16. Excluding working capital effects, cash flow from operations stood at $4.8 billion, compared with $2.1 billion in Q1FY16. The company incurred $4.4 billion in capital and exploratory expenditures compared with $6.5 billion in Q1FY16, primarily for upstream business as it accounted for 90% of the company’s total capex in Q1FY17. The group’s oil brand, Caltex, has been said to have retired CF diesel engine oils range in the UAE as per the recent regulatory requirements. Over the past six months, the stock marginally declined by 1%, on account of fluctuations in global crude oil prices. We give an “Expensive” rating on stock at the current market price of $ 105.47

CVX Daily Chart (Source: Thomson Reuters)

ConocoPhillips

COP Details

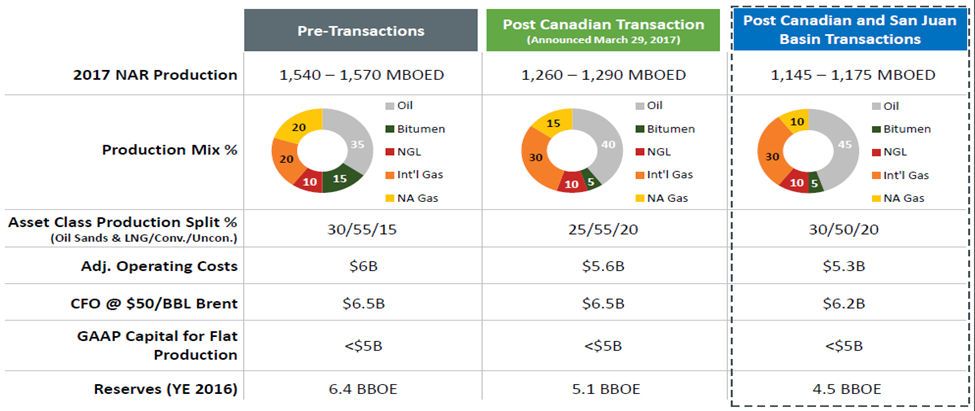

Leveraging the recovery of global commodity prices and improving cash flow profile:For Q1FY17, ConocoPhillips (NYSE: COP) has highlighted that its current dividend can withstand low prices and there is room for annual increases. Further, the group expects the recent transactions to reduce average cost of supply to ~$35/BBL. The group had also witnessed a net profit after tax at $0.6 billion against a loss of $1.5 billion in Q1FY16. However, excluding special items, adjusted earnings posted a loss of $0.2 billion against adjusted loss of $1.2 billion in Q1FY16. Special items for the current quarter were primarily driven by a financial tax accounting benefit related to the Canadian disposition, partially offset by non-cash impairments in Alaska and the Gulf of Mexico. Further, the company’s revised $400 million of full-year guidance for dry hole expense resulted in adjusted dry hole and leasehold impairment expense of $450 million. The company’s total realized price stood at $36.18 per barrel of oil equivalent (BOE) against $22.94 per BOE in Q1FY16, reflecting higher average realized prices across all commodities. On production front, the company reported 2% yoy growth at 1,584 MBOED (barrels of oil equivalent per day) excluding Libya, led by production ramp up from several major projects and improved well performance, partly offset by normal field decline and dispositions. However, there was 4% yoy decline in production and operating expenses. Further, some strategic asset dispositions in Canada and San Juan Basin for total consideration of more than $16 billion were announced by the company. It has come into picture that Cenovus Energy will buy out the joint venture with COP and acquire several other assets. Another key highlight to note is that the group has strengthened its balance sheet through $0.8 billion of early debt retirement and revised a debt target of $15 billion by year-end 2019. For Q2FY17, production is expected to be 1,495-1,535 MBOED excluding Libya and impacts from the recently announced Canada and San Juan Basin dispositions.

Estimated Pro Forma Metrics for FY17 (Source: Company reports)

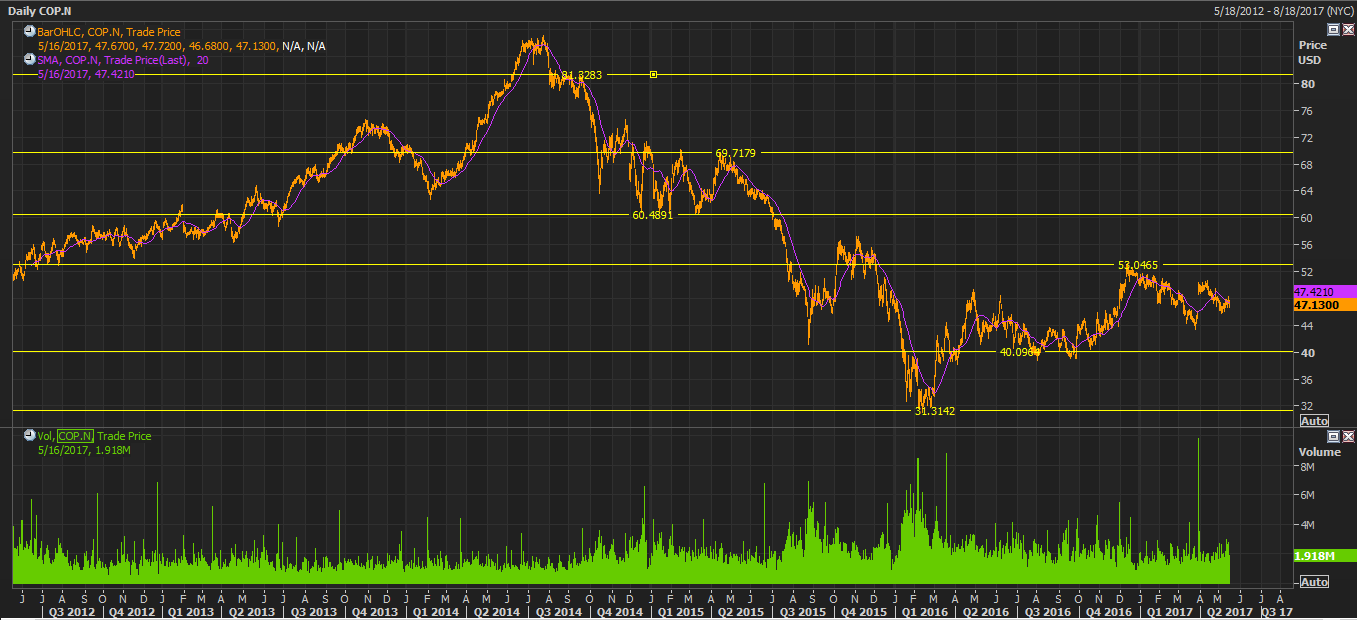

During the quarter, COP also generated cash flows of $1.8 billion from operating activities but the same were slightly impacted by the settlement of a $0.2 billion currency swap, and partially offset by $0.1 billion from a tax loss carryforward in Libya. The company funded $0.9 billion in capital expenditures and investments, repaid debt of $0.8 billion while paying dividends of $0.3 billion. All in all, COP has been continuously putting efforts to improve its cash flow profile and strengthen its balance sheet to rebound from the deep dive of the last few years. We give a “Buy” recommendation on the stock at the current price of $ 47.05

COP Daily Chart (Source: Thomson Reuters)

Exxon Mobil Corp

XOM Details

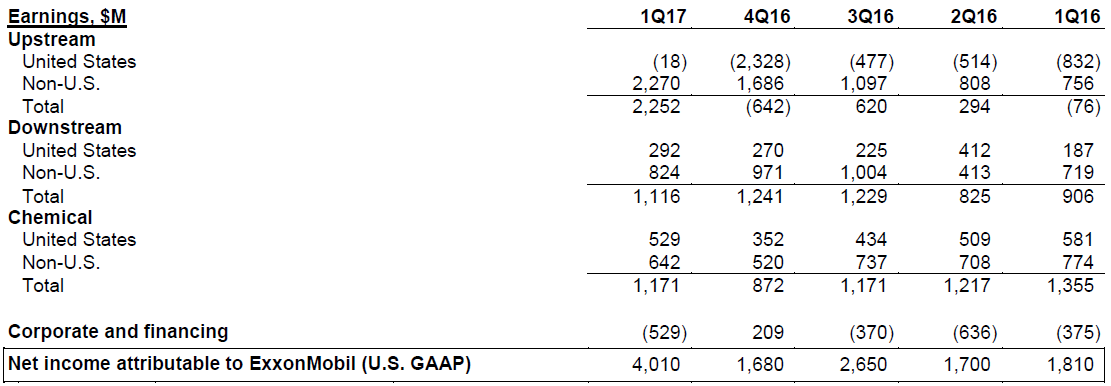

Acquiring assets across the value chain for tactical growth:Exxon Mobil Corp (NYSE: XOM) reported 122% yoy growth in PAT at $4 billion driven by improvements in commodity prices, cost management and refining operations. However, upstream volumes declined 4% yoy to 4.2 million oil-equivalent barrels per day, primarily due to the impact of lower entitlements due to increasing prices, and higher maintenance activity mainly in Canada and Nigeria. While upstream earnings improved to $2.3 billion on higher liquids and gas realizations, downstream earnings benefited from increased refinery throughput but chemical earnings were impacted by lower margins. The company incurred $4.2 billion in capital and exploration expenditure as it advanced investments across its integrated businesses. The company generated cash flows of $8.9 billion from operating activities including proceeds associated with asset sales of $687 million during the quarter.

Earnings summary (Source: Company reports)

Further, XOM continues to make strategic acquisitions and fund long-term growth projects across the value chain. During the quarter, the company acquired Inter Oil Corporation and companies with oil and gas properties primarily in the Permian Basin. Further, it has signed a sale and purchase agreement to acquire a 25% indirect interest in the natural gas-rich area 4 block, offshore Mozambique, for approximately $2.8 billion. Additionally, XOM secured a high-potential exploration acreage in Papua New Guinea, Cyprus and the U.S. Gulf of Mexico and announced positive results from the Snoek well offshore Guyana, confirming a new discovery on the Stabroek Block. Notably, ExxonMobil launched Mobil 1 Annual Protection, which offers consumers the convenience of driving one full year or up to 20,000 miles between oil changes. Mobil 1 Annual Protection has been specifically formulated to offer maximum wear protection, as well as increase resistance to oil breakdown and protect engine parts from harmful sludge and deposits, resulting in extended engine life. The group has the advantage of maintaining free cash flow and paying dividends, with benefits pouring from the downstream business. The group also aims to keep on strategizing while risks appear from oil price scenario. We give a “Buy” recommendation on the stock at the current price of $ 82.41

XOM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.