BHP Billiton Limited (BUY)

BHP Billiton Limited (ASX: BHP) demerged South32 to enhance concentration on its core portfolio of nineteen assets. The group reported a 9% year over year (yoy) increase in the overall production for the fiscal year 2015 driven by the first production of three major projects- Escondida organic growth project, BMA hay point stage three expansion and Escondida oxide leach area project.

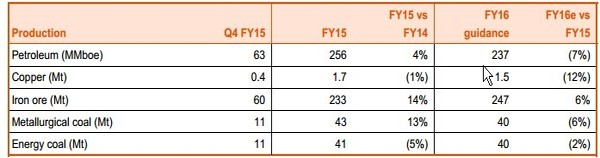

With regards to the segments performance, the petroleum production surged 4% yoy to 256 mmboe on the back of Onshore US liquids volumes growth. BHP Billiton estimates a 19% yoy decrease in the overall production of Haynesville, Fayetteville and Hawkville fields for the fiscal year 2016. The Onshore US liquids volumes delivered outstanding performance during the period, increasing 67% to 56 mmboe, and beating the guidance estimates. Meanwhile, the Natural gas production fell 6% yoy to 787 bcf due to declining demand at Bass Strait and lower onshore US gas volumes during the FY15.

Total iron ore production soared 14% yoy to 233 mt, while the Western Australia iron ore production (WAIO) improved 13% yoy to 254 mt (100% basis), driven by the better output across the integrated supply chain. The group forecasts the full year iron ore production to grow by 6% yoy to 247 mt in 2016 and WAIO is expected to grow to 270 mt (100% basis) by next year, boosted by improving processing efficiency at Mining area C and Newman.

Production Guidance for 2016 (Source: Company Reports)

BHP Billiton Onshore US drilling and development had incurred an expenditure of USD 3.7 billion for the fiscal year 2015, and the group expects to spend further amount of around USD 1.5 billion for the next financial year. On the other hand, in spite of the yearly shale investment cut of over 50%, the firm intends to maintain production in the black hawk and Permian driven by decreasing drilling costs and improved recoveries.

The group’s stock have corrected over 27.4% since it touched a peak price of $34.12 during this year, on March 2nd. The fall was mainly due to the falling iron ore, copper and Oil prices, as the group’s commodities are linked to the index price for the shipment. Consequently, the Iron ore, Oil (crude and condensate) and copper average realized prices plunged 24%, 39% and 12% during the second half of the fiscal year 2015, as compared to first half of 2015. The company also decreased the Onshore US rig count to 10 during the fiscal year from 10 in FY14, due to the falling prices. BHP estimates its iron ore cost to decrease to US$16 per tonne for the next financial year.

However, with stock trading just above approximately 6.5% of its multi-year lows, we believe that it is now poised to raise to higher levels, driven by the operational efficiencies. Improving commodity prices might also add support to the stock. Moreover, despite falling iron ore costs estimates for the next year, the group will be able to maintain competitive margins. The stock has a competitive P/E at 10.92 x, better than its industry peers and a dividend yield of 6.48%. Based on the foregoing, we give a “BUY” recommendation to the BHP Billiton at the current levels of $25.90.

South32 Limited (BUY)

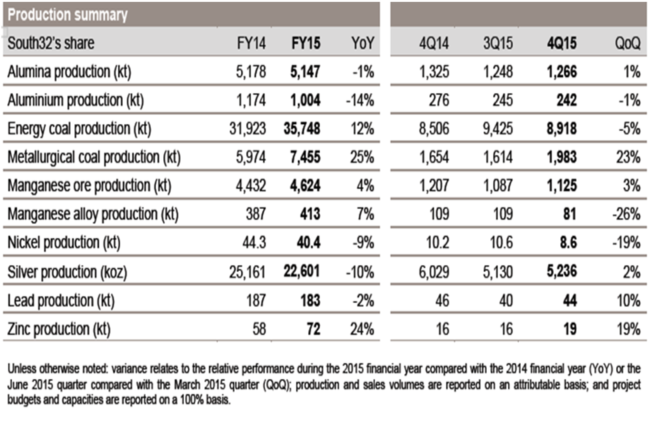

South32 Ltd (ASX: S32) recently reported a decent performance for the fourth quarter of 2015 financial year driven by the Illawarra Metallurgical coal, Saleable alumina at Brazil aluminum, Australia Manganese and South Africa Manganese Ore productions. The group’s total metallurgical coal production, lead production and Zinc production surged 23%, 10% and 19% respectively during the quarter, as compared to the previous quarter. However, the manganese alloy and nickel productions were under pressure, witnessing a decline of 26% and 19% respectively, as compared to the third quarter of 2015 financial year.

Production highlights for fourth quarter of 2015 and Fiscal year 2015 (Source: Company Reports)

South32 got a stable outlook from S&P and Moody’s, who allotted BBB+ and Baa1 credit ratings, and has a net cash of USD 54 million. The group is making efforts to achieve a solid operational efficiency in the coming years, after demerging from BHP on May 2015.

The company started trading on ASX from May 18

th and touched a high of $2.45 on May. However, the falling commodity prices coupled with profit booking by investors (as each BHP Billiton shareholder received a share in South32) have beaten down its share prices by 13.3% since its listing. On the other hand, we believe that the selling by the investors is almost finished, and the stock is poised to grow higher in the coming months. But, investors need to withstand the risks associated with the commodity price fluctuations, to derive good returns from the stock. Having an attractive P/E at 13.86x, we recommend a “BUY” on the stock, at the current levels of $1.715.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.