Company Overview - Woodside Petroleum Ltd (Woodside) is an oil and gas company. The Company is engaged in exploration, development and production of hydrocarbons. The Company operates in five segments: North West Shelf Business Unit, Pluto Business Unit, Australia Oil Business Unit, Browse Business Unit and Others. North West Shelf Business Unit segment develops, produces and sales liquefied natural gas (LNG), pipeline natural gas, condensate, liquefied petroleum gas and crude oil. Pluto Business Unit segment develops, produces and sales liquefied natural gas and condensate in assigned permit areas. Australia Oil Business Unit segment evaluates, develops, produces and sales crude oil in assigned permit areas. Browse Business Unit segment evaluates and develops liquefied natural gas and condensate in assigned permit areas. Other segment consists of activities undertaken by the trading and shipping, United States, exploration, International and Sunrise Business Units.

.png)

WPL Dividend Details

Strengthening portfolio by acquisitions: Woodside Petroleum Limited (ASX: WPL) continues to expand its portfolio by making acquisitions and developing projects. The group acquired interests in Wheatstone, Balnaves and Kitimat during fiscal year of 2015. Woodside Petroleumfound more 2C Contingent resources of 68 MMboe (net) through the Pyxis-1 exploration wellduring the year as well as identified gas at Block A-6 in the Rakhine Basin at Myanmar. Meanwhile, Woodside Petroleum even finished its Xena Phase 1 project before the schedule and started its production in June 2015 leading to net reserves (2P) of over 197 Bcf dry gas and 2.3 MMbbl of condensate.

Consequently, WPL reported a proved plus probable (2P) annual total reserves replacement ratio of 276% during 2015 mainly driven by the acquisitions. As a result, the group’s 2P developed and undeveloped Reserves enhanced by 19.1%, to 264.8 MMboe while 2C Contingent resources surged by 151% to 2,632 MMboe. Woodside Petroleum started production from the Greater Western Flank Phase 1 Project in December 2015 and got US$2.0 billion approval for developing Greater Western Flank Phase 2 Project off the north-west coast of Australia.

.png)

Proved plus Probable (2P) Annual Total Reserves Replacement Ratio (Source: Company Reports)

Ongoing impact of falling oil prices on financial performance: The group’s annual production fell by 3% to 92.2 MMboe, during fiscal year of 2015 as compared to prior corresponding period (pcp) on the back of planned Pluto turnaround decrease coupled with declining natural fields. Woodside Petroleum delivered weak sales revenue performance during the period, and reported a decrease of 36% against pcp. Falling realized prices across the portfolio due to ongoing oil prices pressure had hurt the group’s top line performance. The average price of Brent oil fell by 46% to US$53.60 during 2015 as compared to the average Brent price in 2014. As a result, the group’s operating cash flow plunged 50%, while its net profit after tax (NPAT) declined by 99% to US$26 million against fiscal year of 2014.

The impacted top line performance coupled with heavy impairments charges on the back of lower near-term and long-term forward price assumptions had contributed to huge NPAT losses. Meanwhile, WPL used the NPAT adjusted for special items of US$1.126 billion to calculate its fiscal year of 2015 dividends of US109 cents per share.

.png)

Weak NPAT performance in 2015 (Source: Company Reports)

Group’s productivity program offsetting top line pressure to a certain extent: Woodside Petroleum is controlling its costs and accordingly cut over 650 positions in the last two years. The group achieved a better production volume increase of 9% in 2015 as compared to its estimated target range of 3% to 5%. WPL targeted over 10% to 20% process improvement and accordingly finished more than 5,900 internal improvement projects. The firm achieved the top range of its forecasted expenditure savings by 20% (estimated 10% to 20%) during 2015. Woodside Petroleum financial discipline paid off with breakeven cash costs of sales plunging 33% to $11 per barrel of oil equivalent during 2015 as compared to 2013, and from US$14.27 in 2014 which is a decrease of 22% yoy. The group decreased its unit product cost by 9% in 2015 against 2011 even though they added an asset in Pluto during 2012 as well as its other maturing oil assets. WPL’s Production rose by 43% since 2011 while barrel of oil equivalent for full time equivalent employee ratio surged by 60%, indicating the efforts undertaken by WPL to improve its productivity. Woodside aggressively expanded its exploration acreage by 95% from 2011 till 2015. WPL is also making efforts to improve its Browse project by decreasing costs, as well as enhancing the project’s facility capacity and reliability.

WPL made a front-end engineering and design (FEED) for Browse in 2015 and got Commonwealth and State retention lease renewals. WPL is targeting to further its decrease costs for Browse and intends to achieve net present value positive at low price assumptions. Meanwhile, Woodside Petroleum had raised $4.1 billion leading to its pre-tax portfolio cost of debt to 2.9% by fiscal year of 2015. The group had $1.7 billion in cash and undrawn facilities as of 2015. Woodside Petroleum intends to achieve a liquidity of $2 billion for 2016 to position itself in the continuing oil prices pressure.

.png)

Cost reduction efforts (Source: Company Reports)

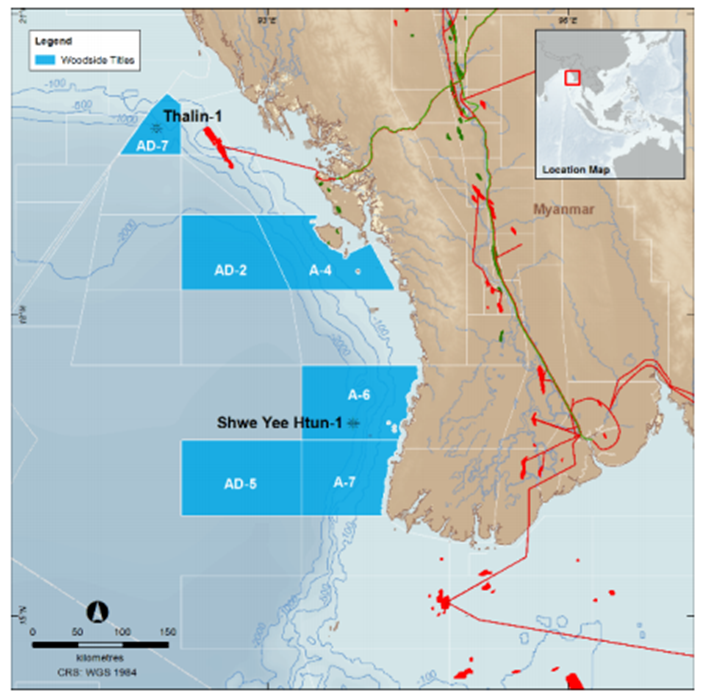

Ongoing discoveries in Myanmar promise solid potential: The group reported that they found a gas discovery at its Thalin-1A exploration well in Block AD-7 (located over 100km offshore of the west coast of Myanmar) in the Rakhine Basin which made an intersection of a gross gas column of over 64m. Over 62m of net gas pay is inferred within the primary target interval. Thalin-1A exploration well intersected a total depth of 3034m, and after drilling, the wireline logging indicated the presence of a gas column as per pressure measurements and gas sampling. This is the second gas discovery at Thalin-1A after the first gas discovery by the firm at the Shwe Yee Htun-1 well in Block A-6. These developments promise a potential exploration and appraisal activity, at Myanmar. The AD-7 is a Joint Venture between Woodside Energy (Myanmar) Pte Ltd (40% interest) and Daewoo International Corporation (60% interest).

The AD-7 Joint Venture is further acquiring 1200km2 of 3D seismic data over this area wherein the seismic survey is expected to start by March 2016. This expansion might lead to more prospects in the future. The group now has interests in six blocks at offshore Rakhine basin leading to over ~47,000km2 and accounting around 20% of its global exploration acreage.

Myanmar portfolio (Source: Company portfolio)

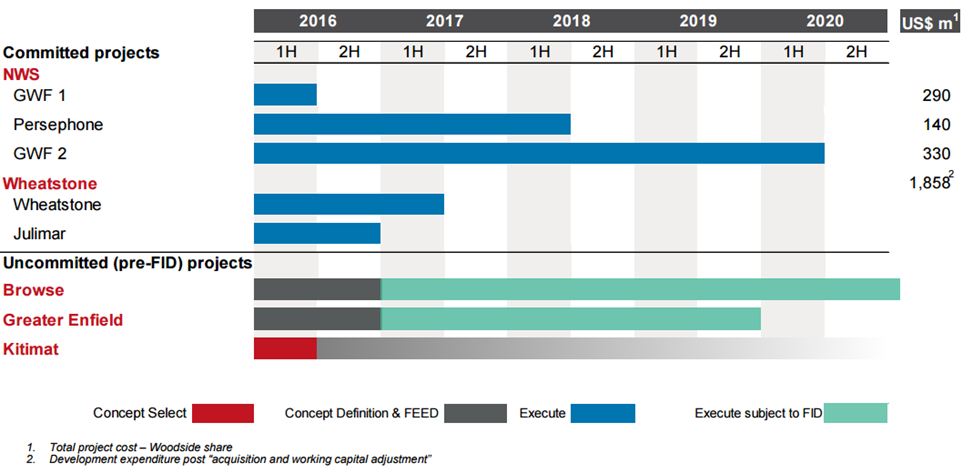

Outlook: Woodside Petroleum continues to maintain a strong balance sheet to withstand the current tough commodity market conditions. The group intends to further cut its cost of operations as well as achieve more capital discipline for generating better shareholder returns. WPL’s Persephone project, is estimated to deliver its first gas in the first half of 2018 while the first gas from the Wheatstone LNG project is forecasted by mid-2017.

As per the Greater Western Flank highlights, the Phase 2 Project is expected to deliver the first gas by the second half of 2019. WPL intends to differentiate itself from its peers via its leveraging technology coupled with reducing costs and commercialization of stranded resources. The group is also enhancing its marketing capabilities by reaching new markets and decreasing shipping costs.

Developing solid pipeline (Source: Company Reports)

Stock Performance: Woodside Petroleum Limited stock continued to face pressure even this year due to poor 2015 financial performance. The stock fell over 13% during this year to date (as of March 15, 2016). On the other hand, we believe that the stock has the capability to recover from these levels given the improving oil prices since the last few weeks. Moreover, the group’s productivity program delivered over $700 million of benefits to WPL in 2015. Woodside intends to continue its productivity enhancement efforts even in the coming periods. WPL has an outstanding portfolio of assets and the back to back gas discoveries at Mynamar might add to the group’s long term potential. Sempra Energy also lately announced for a Project Development Agreement with Woodside with regard to advancement of the earlier announced MOU on the potential development of the Port Arthur Liquefaction Project in Texas, with focus on greenfield development for 2x5mtpa LNG trains.

We believe that the correction in the stock has placed WPL at attractive levels and long term investors could consider adding this stock in their portfolio. The stock also has a decent dividend yield. Based on the foregoing, we remain bullish on WPL and give a “BUY” recommendation at the current price of $26.04

.PNG)

WPL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.