Company Overview: Origin Energy Limited is an integrated energy company. The Company is engaged in exploration, production, generation and the sale of energy to households and businesses across Australia. Its segments include Energy Markets, Integrated Gas, Contact Energy and Corporate. The Company's exploration and production portfolio includes the Bowen, Surat and Cooper/Eromanga basins in Central Australia, the Otway and Bass basins in Southern Australia, as well as interests in the Browse and Perth Basin in Western Australia, and the Bonaparte and Beetaloo Basin in the Northern Territory. It also has exploration projects located in New Zealand in the Taranaki and Canterbury basins, as well as in Vietnam. It jointly owns and wholly operates gas-producing facilities in Australia and New Zealand, including the BassGas and Otway Gas Production plants in Victoria, coal seam gas (CSG) production plants as part of the Australia Pacific LNG Project in Queensland, and the Kupe Gas Project in New Zealand.

.png)

ORG Details

Decent Performance in FY19 and Achievement of Target Capital Structure: Origin Energy Limited (ASX: ORG) is primarily engaged in the operation of energy businesses, which includes exploration and production of natural gas, electricity generation, wholesale and retail sale of electricity and gas, and sale of liquefied natural gas. As on September 18, 2019, the market capitalisation of Origin Energy Limited stood at ~A$14.02 billion. The company has recently released its financial numbers for FY19 in which its statutory profit amounted to $1,211 million. The company’s underlying EBITDA stood at $3,232 million, while underlying profit came in at $1,028 million, reflecting a decent rise of 41.6% from $726 million in FY18. It was stated that robust earnings by the Integrated Gas were witnessed from a higher effective oil price, cost efficiencies and stable production at Australia Pacific LNG, which delivered net cash flow of $943 Mn to Origin Energy Limited. However, the energy markets witnessed moderately reduced earnings in the electricity because of price relief measures which were provided to the customers, continued impact of increased retail competition as well as lower average customer numbers and usage. The following table provides a broader overview of the performance summary, which is important for the shareholders:

.png)

Performance Summary (Source: Company Reports)

The fall in financing costs associated with the reduced debt of $5.4 billion at June 30, 2019, along with the lower average interest rate, helped the company’s improved financial performance. The Board of the company has made an announcement about the new dividend policy and determined the fully franked final dividend amounting to 15 cents per share and, as a result, total dividends stood at 25 cents per share in FY19. The company’s CEO named Frank Calabria stated that the result was supported by the contributions from 2 robust cash-generating businesses. The efforts to simplify the organisation and a $1.1 billion reductions in debt led the company to achieve the lower end of its target capital structure range of 2.5-3.0x. As at 30 June 2019, adjusted Net debt/ Adjusted Underlying EBITDA stood at 2.6x.

The company witnessed a turnaround in FY18 in terms of profitability from losses in FY17, and the profit grew enormously in FY19 as compared to figure reported in FY18. Moving forward, there are expectations that the decent capabilities to garner revenues and build cash levels along with a stable balance sheet might support ORG to grow over the long-term.

Top 10 Shareholders: The following picture provides a broader idea of the top 10 shareholders in Origin Energy Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Decent Rise in Net Margin and Return Ratios: The net margin of Origin Energy Limited stood at 8.2% in FY19, which is higher than FY18 figure of 1.9% and, thus, it can be said that ORG’s capabilities to convert its top-line into the bottom-line have improved. Additionally, the company’s operating margin stood at 3.9% in FY19, which is marginally higher than the previous year’s figure of 3.8%. ORG’s return on equity (or RoE) grew by ~730 bps to 9.7% in FY19 as compared the prior year and, thus, it looks like that ORG has delivered better return to its shareholders, which might help it in gaining traction among market participants. The company’s current ratio at the end of FY19 stood at 1.21x, which has improved from 0.85x in FY18 and, therefore, it can be said that ORG is in a better position to meet its short-term obligations as compared to the prior year. Additionally, the improved liquidity levels provide it with decent headroom to make further deployments towards the key strategic business that could help in long-term growth. In FY19, debt/equity ratio came in at 0.58x, which reflects fall from 0.63x, and it looks like that ORG has been focusing towards deleveraging its balance sheet. Generally, the lower debt on the balance sheet reflects stability and might help a particular company to focus on long-term growth objectives.

.png)

Key Metrics (Source: Thomson Reuters)

BidEnergy Signs Agreement With ORG: BidEnergy Limited has recently made an announcement that it has inked an agreement with ORG to deploy BID’s Robotic Processing Automation (or RPA) platform and analytics throughout ORG’s Commercial and Industrial (or C&I) customers. The signing of an agreement follows ORG’s successful pilot of the BidEnergy’s RPA platform with customers earlier in the year. BidEnergy Limited anticipates rollout of its platform to be completed by the month of December 2019. Additionally, it was mentioned that the scope of services for this subset of ORG’s customers is for a 3-year term.

Key Takeaways from the Presentation Made to Analysts and Financial Markets: Origin Energy Limited has recently released a presentation which was made to the analysts and financial markets in which key financial numbers for FY19 was given. In the presentation, it was mentioned that ORG has a continued focus on the shareholder value, and it is also maintaining the balance between growth and returns. It has a disciplined capital allocation and is executing the growth options. The following image has been extracted from the company’s presentation:

.png)

Disciplined Capital Allocation Framework (Source: Company Reports)

With respect to the dividend policy, the company stated that it is targeting an ordinary dividend pay-out range in between 30%-50% of free cash flow per annum. The free cash flow reflects cash from the operating activities and investing activities (excluding the major growth projects), less interest which has been paid. The Board, at its discretion, can adjust shareholder distributions for the economic conditions. It was further stated that the Dividend Reinvestment Plan (DRP) will operate at nil discount and ORG will purchase shares on the market in order to satisfy the DRP.

Understanding Performance of Energy Markets and Integrated Gas: The underlying EBITDA in Energy Markets amounted to $1,574 million, which represents a fall of $77 million from FY18. Even though there were reduced earnings, Energy Markets business posted a 27% rise in the operating cash flow after improvements in the working capital and favourable movements in the electricity futures exchange collateral. The below picture gives a broader overview of the operational performance:

.png)

Operational Performance (Continuing Operations) (Source: Company Reports)

The company stated that implementation of a new leaner, asset-led structure and efficiencies in well design and drilling execution, helped Integrated Gas in achieving unit cost targets. ORG resumed exploration activities in Beetaloo Basin after lifting of moratorium on the onshore gas development last year by Northern Territory Government. In the remainder of 2019, the company has intentions to drill 2 horizontal wells and then undertake extended flow testing of liquids and gas in 2020.

What To Expect From ORG Moving Forward: Origin Energy Limited has provided the guidance for FY20 on the basis that market conditions do not change materially and that the regulatory and political environments do not result in further adverse impacts on the company’s operations. With respect to energy markets, the company has provided guidance for the underlying EBITDA in the range of $1,350 to $1,450 million. The gross profit of natural gas portfolio is anticipated to be relatively stable, and there are estimations that there would be a reduction in the electricity gross profit reflecting impacts of government default market offers ($100 million), lower green scheme prices flowing through to business customer tariffs and lower customer usage. Further, the cost to serve retail and business customers is expected to be $40 million- $50 million lower, showing ongoing productivity efforts.

In the recent sustainability report, it was stated that Australia Pacific LNG happens to be a joint venture between Origin (37.5%), ConocoPhillips (37.5%) and Sinopec (25%) and it is Australia’s leading producer of coal steam gas (CSG). Australia Pacific LNG’s production has been estimated to be in the range of 680- 700 petajoules. Its distribution breakeven has been estimated to be between US$33-US$36/boe. It was further stated that the sale of Ironbark asset to Australia Pacific LNG for $231 million, which was settled on August 5, 2019, would be contributing to the debt reduction in FY20. There are expectations that the corporate costs would be in the range of $70 million to $80 million and the capital expenditure and investments (excluding Australia Pacific LNG) are expected to be in the range of $530 million to $580 million.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

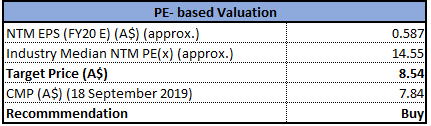

Method 1: PE- Based Valuation

PE- Based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

Method 2: EV/EBITDA Multiple Approach

.png)

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters.

Stock Recommendation: The stock price of ORG has delivered the return of 12.82% in the span of previous one month, while in the time span of previous three months, the stock’s return was 14.62%. The company’s top-line has witnessed a CAGR growth of 5.49% in the span of FY15- FY19, which can be considered at decent levels. Its cash receipts have witnessed a CAGR growth of 1.60% between FY15- FY19. In the annual report for FY19, it was stated that Australian economy’s transition to the lower emissions would be presenting new challenges and opportunities for the company and it is well-placed to meet those. Based on the foregoing, we have valued the stock using two relative valuation methods, i.e., P/E multiple and EV/EBITDA multiple and arrived at a target price upside in the range high single-digit to low double-digit (in percentage terms). Hence, considering the aforesaid facts and decent outlook, we give a “Buy” recommendation on the stock at the current market price of $7.840 (down 1.508% on 18 September 2019).

ORG Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.