Zero Plus Tick or Zero Uptick

Updated on 2023-08-29T11:56:59.252318Z

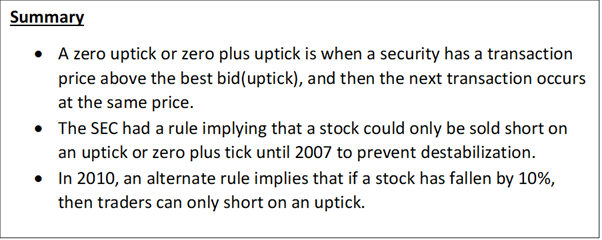

What do you mean by Zero Plus Tick?

A zero plus tick, also known as zero uptick, is a security trade executed at a similar price as the previous trade, but at a price higher than the last trade. For example, if trades happen at US $100, US $100.01, and US $100.01 once again, the last trade would be considered as zero plus tick, or zero uptick trade, since it is a similar price as the past trade. However, a higher price than the last trade at an alternate price.

The term zero plus tick is relevant for stocks, bonds, items, and other traded protections, yet it is frequently utilised for recorded value protections. Something contrary to zero plus tick is a zero short tick.

Copyright © 2021 Kalkine Media

Understanding Zero Plus Tick

An uptick, and zero plus tick, implies the price of a stock moved higher and afterward remained there, but momentarily. Consequently, for over 70 years, there was an uptick rule as set up by the U.S. Protections and Trade Commission (SEC), which expressed those stocks must be shorted on an uptick or a zero plus tick, not on a downtick.

The uptick rule was proposed to balance out the market by keeping dealers from destabilizing a stock's price by shorting it on a downtick. Preceding the execution of the uptick rule, it was not unexpected for gatherings of dealers to pool capital and offer short to drive down the price of a particular security. The objective of this strategy was to cause a frenzy among investors, who might then sell their offers at a lower price. This control of the market made protections decrease considerably further in value.

It was assumed by the experts that the financial trade crash of 1929 was due to the short selling on downticks. The uptick rule was executed in 1938 and lifted in 2007 after SEC presumed that markets were progressed and systematic enough not to require the limitation. It is likewise accepted that decimalisation on the significant stock trades assisted with making the standard unnecessary.

During the 2008 recession, SEC got widespread recommendations for the reset of the uptick rule, which ultimately made it bring in the elective uptick rule in 2010. This standard expressed that short selling would just be permitted on an uptick if a stock dropped over 10% in a day. When the 10% drop has been set off, the other uptick rule stays for the remainder of the day and the next day.

For example, Company ABC has a bid price of US $273.36 and an asking price of US $273.37. Trades have happened at both of these prices as of now as the value holds there. A trade happening at US $273.37 is an uptick. If another trade happens at $273.37, that is a zero plus tick/uptick.

Mostly, this doesn't make any difference. In any instance, the stock has fallen by 10% from the earlier close price at one point in the day; at that point, the upticks matter because a broker could be short if the price is on an uptick. This implies they can just get filled on the offer side. They can't cross the market to eliminate liquidity off the bid. This is per the elective uptick rule set up in 2010.

Frequently Asked Questions

- What are the Uptick Rules?

The Uptick Rule is a previous law set up by the Securities and Trade Commission (SEC) that requires each short deal trade to be entered at a higher price than the past trade. It is popularly known as the "plus tick rule". This standard was presented in the Securities Trade Act of 1934 as Rule 10a-1 and carried out in 1938. It keeps short merchants from adding to the descending energy of a resource previously encountering sharp decreases.

A short deal request with a price over an ongoing bid can be made and a short merchant guarantees their request is filled on an uptick. The uptick rule is dismissed when exchanging a few monetary instruments like futures, single stock futures, monetary forms, or market ETFs like the QQQQ or SPDRs. These instruments can be shorted on a downtick since they are profoundly liquid and have enough purchasers willing to go into a long position, guaranteeing that the price will infrequently be headed to low levels.

The uptick rule was dispensed within 2008 and later restored, yet it is possibly enacted when an individual organisation's offers have fallen 10% on an exchanging day.

The uptick rule can disappoint short merchants (individuals who are wagering that a stock will fall) since they should trust that the stock will settle before their request can be filled.

A few financial backers contend that uptick rules repress exchanging and recoil liquidity. To short a stock, a financial backer should initially get the offers from somebody who claims them. This provokes interest in the offers. Short selling gives liquidity to business sectors and keeps stocks from being offered to absurdly undeniable degrees of promotion and over-idealism.

The 2010 elective uptick (Rule 201) permits financial backers to exit long situations before short selling happens. The standard is set off when a stock value falls essentially 10% in one day. By then, short selling is allowed if the price is over the current best bid. This plan is to protect financial backer certainty and advance market strength during times of pressure and instability.

The standard's "duration of price test restriction" applies the standard for the rest of the exchanging day and the next day. For the most part, it applies to all value protections recorded on a public protections trade, regardless of whether traded through the trade or over the counter.

For the futures, there are limited exclusions to the uptick rule. These instruments can be shorted on a downtick since they are profoundly liquid.

To meet all requirements for the exception, the prospects contract should be considered to be "owned by the dealer". As per SEC, it means that the individual holds a security futures agreement to buy it and has an indication that the position will be taken care of.