Idiosyncratic Risk

Updated on 2023-08-29T11:55:03.430744Z

What Is Idiosyncratic Risk?

Idiosyncratic risk, also called as unsystematic risk, is a category of risk associated with specific assets or asset class. Unsystematic risk is different for each investment made by a corporation, and it considers the asset's possible consequences if a particular occurrence happens that has the potential to adversely affect the investment. These are factors that have an adverse effect on a particular security.

Diversification is a measure employed to mitigate such risks. Microeconomic influences are the reasons for idiosyncratic risks. Microeconomic influences are those that impact a relatively smaller part of the economy as compared to a macroeconomic force like market risk or interest rate. The unsystematic risk may be caused by financing decision, operating decisions, management changes, malpractices by the company, corporate governance policies, working culture etc.

Some examples of idiosyncratic risk -

- Strike by pilots affecting the operations of the airlines company

- A company’s financial fraud harming its reputation

- Spread of bird flu that affects poultry industry

- Government restriction on the mining of certain metals will impact the operation and valuation of companies in the mining industry alone

- Stoppage of construction activity due to a lockdown will affect the performance of construction industry based companies

Summary

- Idiosyncratic risk is a category of risk associated with specific assets or asset class

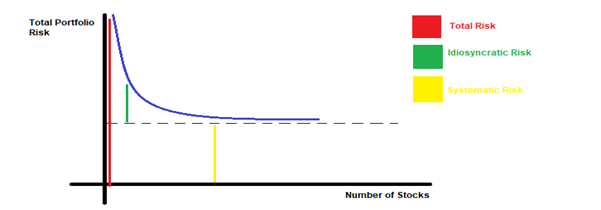

- Total risk in a portfolio is the sum of idiosyncratic risk and systematic risk.

- Microeconomic influences are the reasons for idiosyncratic risks.

- Diversifying investments and increasing the total number of investments will help to minimise idiosyncratic risk.

- The idiosyncratic risk may be attributed to financing decision, operating decisions, management changes, malpractices by the company, corporate governance policies, working culture etc.

Frequently Asked Questions

What May Be the Causes of Idiosyncratic Risks?

Copyright © 2021 Kalkine Media

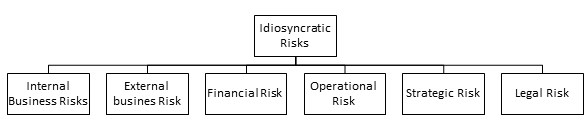

Idiosyncratic risks may include internal business risks like management reshuffling within a company. There may be external business risk like, for example, a government ban on medicine – it may impact pharma industry based companies. A financial risk like unstable cash flows of the company too is idiosyncratic risk. Similarly, an operational risk like undetected fault in distribution mechanism or a strategic risk like the launch of an unwelcome product feature due to insufficient sample size in market research or a legal risk like a case filed on a company due to violation of environmental laws are all cases of idiosyncratic risk.

How could unsystematic risk be assessed?

The main steps involved in assessing idiosyncratic risk are assessing the market capitalisation or market concentration and studying the impact of industry performance determinants like technology, political factors, technology, economic and international factors and computing company-specific risk by studying the man and material management in the company. All such factors can be added up to estimate unsystematic risk.

Can the idiosyncratic risk be mitigated in a portfolio of stocks?

The organisation risk that is inherent in an investment is referred to as unsystematic risk. Diversifying investments and increasing the total number of investments will help to minimise unsystematic risk. The residual risk for investment is another word for unsystematic risk. The beta coefficient of a business represents the systematic risk of an investment. In a stock portfolio, idiosyncratic risk is measured by estimating the difference between total portfolio variance and market variance.

Copyright © 2021 Kalkine Media

For an investor holding a portfolio of stocks, the risk of an asset is the risk added by the asset to the entire portfolio. In the Capital Asset Pricing Model (CAPM), which assume that all investors hold a portfolio, the risk of any asset is equivalent to the change in risk to the portfolio due to the addition of the asset to his/ her portfolio. Thus if we were to assume that an asset’s movements are independent of the market portfolio, then it would imply that it would not add risk to the portfolio. Total risk in a portfolio is the sum of idiosyncratic risk and systematic risk. Unsystematic or idiosyncratic risk can be reduced gradually by adding more and more stocks to the portfolio. Efficient diversification can reduce the total risk to the extent that only systematic risk remains and unsystematic risk is almost zero.

How to calculate idiosyncratic Risk?

To measure idiosyncratic risk in a stock portfolio, you will need to calculate the difference between total portfolio variance and market variance.

Following is a step-by-step process to calculate Idiosyncratic Risk

- Assessing Beta of Stock Portfolio

Beta values, the co-movement of an asset with the market, can be looked up for the investments on websites like Yahoo Finance or Google Finance. Once the beta values have been identified, a weighted beta average can be calculated on the basis of investment percentage each account holds. For each holding, beta value is multiplied by the percentage of the portfolio value with respect to its investment. By adding up each product of each holding, the average beta for the entire portfolio is calculated.

For example, investment consists of two companies – A and B. Company A has a beta coefficient of 1.02 and Company B of 1.35.

Determine the amount of investments to place in each company. A company with a lower Beta can be allocated a greater percentage of your investment. However, 50 per cent of the investment has been allocated to each company.

By applying the following formula:

Copyright © 2021 Kalkine Media

- Assess the market variance and market risk of the portfolio

Market risk of the portfolio can be calculated by multiplying the average portfolio beta with the historical volatility of an stock market index or fund, which is diversified.

Once can find the historically volatility of a diversified stock market index or fund, listed as “volatility” or “standard deviation” on financial websites. The index or fund should have a beta value near 1.

The market variance of the portfolio can then be calculated by squaring the market risk of the portfolio.

Market Variance = (Market Risk of the Portfolio)2

Market Variance = (Average portfolio beta X historical volatility of a stock market index or fund)2

- Estimate the Total Risk and Total Variance of Your Portfolio –

- The total risk of the portfolio is estimated by calculating the standard deviation of the portfolio's historical returns using a portfolio back-testing calculator that will report the volatility or risk or standard deviation.

- The total variance of the portfolio is calculated by squaring the total volatility of the portfolio.

Total Variance = (Total volatility of the portfolio)2

- Assess the Idiosyncratic Variance and Risk of the Portfolio

- The idiosyncratic variance is measured by subtracting the square of the portfolio’s market volatility from the square of the portfolio’s total volatility.

Formula "Idiosyncratic Volatility = Total Variance – Market Variance

- Take the square root of idiosyncratic variance calculated to calculate the idiosyncratic risk.

Idiosyncratic Risk of Portfolio = Ö idiosyncratic variance

What is the difference between systematic and unsystematic risk?

Since unsystematic risks are company or industry-specific, it may not be possible to predict them in general, but in case of systematic risks where macroeconomic factors are at play, such as central bank announcements, political situations, geographical instabilities may help us to judge risk in the offing and plan to counter it.

Also, in the case of unsystematic risk, diversification may help to mitigate the risk by diversifying the portfolio. But the systematic risk is to do with the economy in general, so the possibility of mitigation is bleak. For example, tax rate announcements, monetary policy announcements, fiscal policy decisions.