Cash Flow Statement

Updated on 2023-08-29T11:59:27.635010Z

What is Cash Flow Statement?

Cash flow statement is one of three crucial financial statements used in evaluating the business performance of a firm. It reflects the net cash generated by a firm during a given financial period after breaking down cash flows of the company into specific types.

Cash flow statement allows information seekers to know how the business is generating cash and spending cash. Information users also analyse the business trends and results of decision-making through the cash flow statement.

The essence of cash flows is vital in a business. As the saying goes: ‘turnover is vanity, profit is sanity and cash is reality!’. Cash generation becomes imperative for the going concern of business and reflects the ability of a firm to honour its obligations.

As a result of accrual-based accounting, the expenses and revenue are recorded when incurred and earned, – cash flows are impacted when money is debited/credited to the bank account of a business.

The revenue of an enterprise may not necessarily match the amount of cash received from customers; it is the reason why turnover is vanity. Cash flow statement shows the net cash position of the company in a given period after making adjustments to information recorded in the income statement and balance sheet.

What is the scope of the Cash Flow Statement?

Liquidity: It shows the liquidity of the business, precisely the level of operating cash generated by a firm. Operating cash generation is an essential aspect of an organisation, depicting how efficiently the company uses assets.

It also shows the potential capital need of the business for other activities like repayment of the debt, capital expenditure, investing in machinery, dividends or share buybacks. In general, it will allow the information users to assess the ability of a firm to meet its investing and financing needs.

Assets, Liability and Equity: Cash flow statement reflects the changes in the assets and liabilities of the business. As the name suggests cash flow, it shows the cash movement in assets and liabilities such as decrease/increase in accounts receivable or payable, repayment of the debt, proceeds from equity/debt issue, purchase of machinery etc.

Moreover, the changes in the balance sheet that have caused cash movement are enlisted in the cash flow statement of the business.

Estimating future cash flows: Past cash flow statements, along with other financial statements, will enable the information users to predict the future cash flows of the business. For instance, if the balance sheet had $100 million of debt in current liabilities last year, the cash flow estimate for next year will incorporate $100 million outflows.

What are the main components of the cash flow statement?

There are two methods of furnishing a cash flow statement: direct and indirect method. Under the direct method, the cash flow statement is prepared by summing up total cash transactions and excluding non-cash transaction completely.

Under the indirect method, the non-cash and cash transactions are added and deducted to the net income of the company. Moreover, this method helps to assess the divergences in the net income and ending cash balance of the company.

Cash flow statement is prepared with the help of the income statement and balance sheet of the business. Income statement enables to assess the potential cash outflow and inflow, while the balance sheet shows the impact of these transactions in the assets and liabilities.

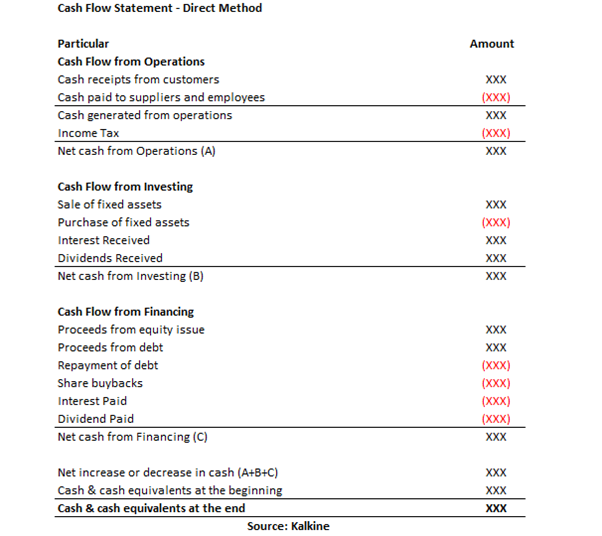

Basic Cash Flow Statement Sample

Cash Flow from Operations

Operating activities reflect the principal revenue-generating activities. It also includes activities that don’t fall under investing and financing activities. In general, this type of cash flows includes cash transactions related to producing and selling goods and services.

Under the direct method, the cash inflow is deducted by cash outflow to suppliers and employees, and the sum is then subtracted by the amount of income taxes paid by companies. The total sum (A) in the above image is net cash flow from operations.

Cash Flow from Investing

As the name suggests investing, in this type of cash flows the transactions that are related to investments are recorded. These items can be purchase or sale of the property, plant and equipment, purchase/sale of intangible assets, interest received on advances, dividends received etc.

It is important to record cash from investing because the cash flow represents the capital expenditure incurred by the firm to generate future cash flows or income. Expenses or income arising out of the assets in the balance sheet are classified in investing activities.

Cash Flow from Financing

In this type of cash flows, those cash flow items are recorded arising out of the capital structure of the company. It represents the claims on future cash flows of capital providers. Financing activities can include proceeds from shares, dividends paid to shareholders, buyback of shares, proceeds from the issue of debt, repayment of debt.

To understand free cash flow watch: What is Free Cash Flow?