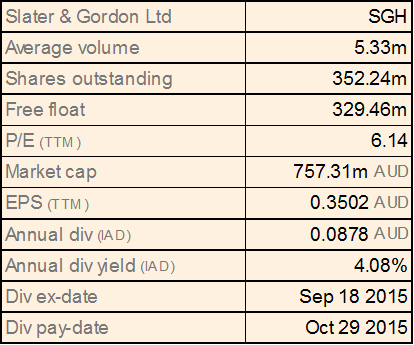

Slater & Gordon Ltd

SGH Dividend Details

Performed Accounting changes to enhance financial reporting transparency; Ongoing business growth: Slater & Gordon Limited (ASX: SGH) stock plunged 64.87% from the last six months (as at November 23, 2015), as Australian regulators started an investigation on the errors in company’s financial reporting in June. Rumors also surrounded the stock on its possible share price manipulation by hedge funds which further led to the downfall. British regulators have launched an investigation on Quindell as well, as Slater & Gordon acquired Quindell’s professional services division for $1.3 billion. As a result, SGH changed its extremely aggressive accounting practices, by shifting to early adoption of AASB 15 - revenue from contracts with customers during fiscal year of 2016. SGH also adopted other measures to enhance its balance sheet transparency as well as made re-classification of the acquisition consideration of some completed transactions for accounting purposes only. On the other hand, Slater & Gordon Limited reported a revenue surge growth of 27% year on year to $521.9 million in fiscal year of 2015, wherein its Australian Personal Injury Law (PIL) practice revenues increased 12.1% yoy boosted by better performance of Victoria and NSW, while brand awareness at Queensland is increasing. Australia’s GL practice revenues also increased 30.9% yoy to $56.7 million, while EBITDAW improved 23.1% yoy to $1.6 million, during the period. The Schultz Toomey O’Brien acquisition, WSW and Leo Abse Cohen acquisitions as well as Business and Specialized Litigation services (BSLS) drove the performance. SGH United Kingdom Personal Injury Law (PIL) practice surged 47.6% yoy to $211.6 million for the fiscal year of 2015, driven by the rise in new cases opened including cases in the multi-track (significant injury) area. SGH investments for United Kingdom’s General Law practice (to become the major provider for specialized personal Legal services in UK) also paid off with Revenues for UK GIL practice improving by 22.3% yoy to $47.8 million for FY15.

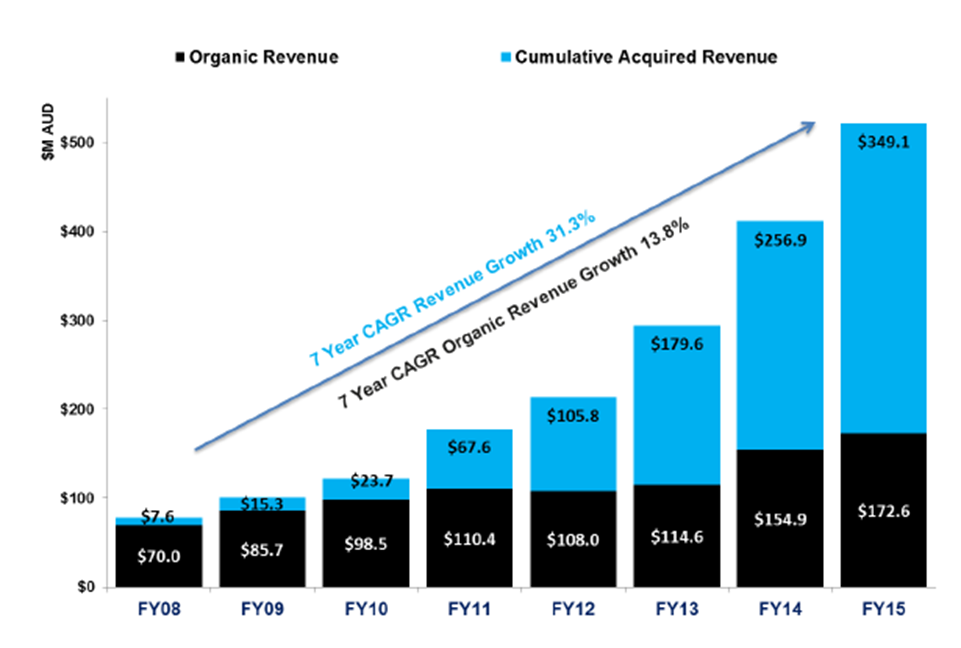

Growing revenues over the years (Source: Company reports)

Attractive Opportunity: SGH issued positive FY16 guidance of more than $205 million EBITDAW and a Gross Operating Cash Flow to EBITDAW of 100%. The total Group Fees (including SGS) is expected to be more than $1,150 million. Investigations by ASIC and UK Financial Conduct Authority may be looked as a risk but SGH’s efforts to deal with these also cannot be ignored. Nonetheless, the stock is trading at very cheap valuation and at a discount to its fair value presenting an attractive entry opportunity for investors seeking for bargain stocks. We remain bullish on this stock given the above and reiterate our “BUY” recommendation at the current price of $2.00

Shine Corporate Ltd

.png)

SHJ Dividend Details

Solid performance via acquisitions: Shine Corporate Ltd (ASX: SHJ) reported a revenue increase of 30.4% to $150.6 million in fiscal year of 2015, as compared to $115.5 million in FY14 driven by solid growth across its Personal Injury and Emerging Practice segments as well as acquisitions’ contribution. The group’s Personal Injury segment’s revenues rose to $116.4 million during the year, boosted by new branches in NSW and Victoria as well as Stephen Browne contribution. Emerging Practice segments revenues delivered outstanding performance during the year and surged over 90.8% yoy to $33.7million as the group’s diversifying strategy paid off while Emanate practice also contributed to the overall performance. Meanwhile, SHJ’s normalized NPAT rose by 37.8% yoy to $30.6 million during the period against $22.2 million in FY14 and the company declared an unfranked final dividend of 1.75 cents per share for FY15. SHJ delivered a positive commentary in its AGM while reaffirming FY16 guidance for EBITDA of $52m-$56m.

.png)

Fiscal year of 2015 performance (Source: Company reports)

Stock Performance: SHJ recently finished the acquisition of Best Wilson Buckley Family Law at Queensland for $5.4 million and the group estimates this transaction to be earnings accretive from fiscal year of 2016. On the other hand, Shine Corporate stock fell over 24.73% (as of November 23, 2015) in the last six months on investors’ concerns over its dependence on acquisitions to drive growth as well as tough market conditions. But, the recent fiscal year of 2015 indicates the group’s ability to derive synergies via acquisitions and we believe SHJ would be able to improve its earnings further in the coming periods. In addition, the correction in the stock placed SHJ at a reasonable valuation with the stock trading at a P/E of about 12x. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $2.09

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.