Seven West Media Ltd

.png)

SWM Details

FY 16 performance was as forecasted: Seven West Media Ltd (ASX: SWM) lately signed a contract to acquire Sunday Times and PerthNow and expect these to increase the shareholder value and deal with the challenges of fragmented market in Western Australia. The group delivered as per the full year guidance in FY 16 and reported a 0.9% fall in underlying net profit after tax (excluding significant items) to $207.3 million. The group reported about 3% fall in the revenues to $1,726.6 million against fiscal year of 2015.

.png)

FY 16 Financial Performance (Source: Company Reports)

Moreover, SWM is accelerating the transformation of its business across all platforms. The program sales and 3

rd party productions is expected to deliver greater than 25% growth and strengthening the position for the future. In addition, the digital is expected to deliver greater than 150% revenue growth. We give a “Hold” recommendation on the stock at the current price of $0.68

SWM Daily Chart (Source: Thomson Reuters)

News Corp

.png)

NWS Details

Ongoing performance pressure:News Corp (ASX: NWS) reported the total revenues of $1.97 billion in the first quarter of FY 17, against $2.01 billion in the corresponding period of last year. The performance pressure is mainly due to foreign currency fluctuations of $36 million. The income from continuing operations for the quarter is nil against $143 million in the prior year. Moreover, NWS has posted loss per share of $0.03 in 1Q FY 17 against earnings per share (EPS) of $0.22 in the prior corresponding period while the adjusted loss per share reached $0.01 during the quarter against EPS of $0.05 in the 1Q FY 16.

.png)

1Q FY 17 Segment Performance (Source: Company Reports)

Even though NWS is making efforts to strengthen their business by the acquisition of Wireless Group plc, we believe the performance pressure could continue in the coming months. NWS stock fell over 16.7% in the last four weeks (as of November 10, 2016) while we give an “Expensive” recommendation on the stock at the current price of $15.97

.PNG)

NWS Daily Chart (Source: Thomson Reuters)

Prime Media Group Limited

.png)

PRT Details

Second half of FY 17 is expected to be subdued against first:Prime Media Group Limited (ASX: PRT) will hold its AGM on November 22, 2016. PRT has posted a rise of 16.0% for the first quarter of FY 17 of the total advertising revenue in the three aggregated regional markets of New South Wales and Victoria from 1Q FY 16. Moreover, PRT expects the core net profit after tax for the 1H FY 17 to be between $15.3 million and $16.3 million.

However, PRT does not expect similar gains in the second half of the FY 17. There is also a decline in regional viewership. PRT stock is also removed from S&P/ASX 300 Index after the market close on September 16, 2016. We give an “Expensive” recommendation on the stock at the current price of $0.31

PRT Daily Chart (Source: Thomson Reuters)

Ten Network Holdings Ltd

.png)

TEN Details

Ongoing core TV segment performance pressure: Ten Network Holdings Limited (ASX: TEN) will conduct its AGM on December 08, 2016 and reported 7.5% growth in fiscal year of 16 for the television revenue which reached $676.4 million while the Television EBITDA reached $4.5 million as compared to the loss of $12.0 million in FY 15.

.png)

FY 16 Financial Performance (Source: Company Reports)

Additionally, the net loss for the FY 16 is of $156.8 million as compared to the net loss of $312.2 million in FY 15. Meanwhile, TEN stock fell 30.31% in last one month (as of November 10, 2016) and, given the limited prospects, we still give an “Expensive” recommendation on the stock at the current price of $1.00

TEN Daily Chart (Source: Thomson Reuters)

Nine Entertainment Co Holdings Ltd

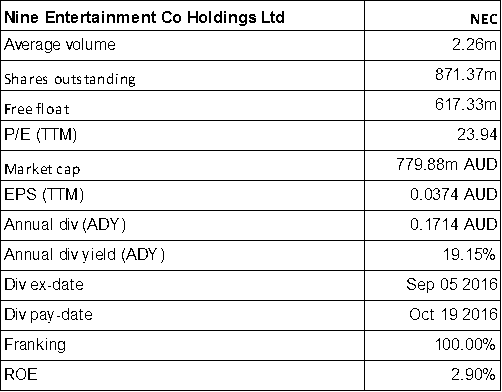

NEC Details

Made Profit from the Sale of Southern Cross Media Group Limited stake: Nine Entertainment Co Holdings Ltd (ASX: NEC) has sold its entire 9.99% stake in Southern Cross Media Group Limited at a price of $1.54 per share at a profit. The stake was acquired in March this year at a price of $1.15 per share. The proceeds would enhance NEC flexibility in executing its growth strategy in the future. In April 2016, NEC and Southern Cross had entered into a five-year regional television affiliate agreement which has brought significant commercial benefits to both the parties.

NEC’s subscriber growth for Stan is on plan and cash break-even is projected in FY18. The group will conduct its AGM on November 19, 2016. NEC stock fell 51.7% this year to date (as of November 10, 2016). We give a “Hold” recommendation on the stock at the current price of $0.94

.PNG)

NEC Daily Chart (Source: Thomson Reuters)

Fairfax Media Limited

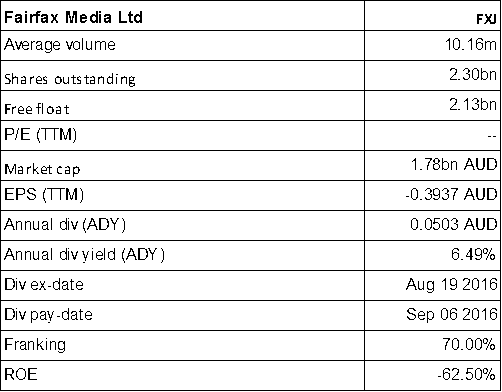

FXJ Details

Cost savings initiatives are ongoing across the group: Fairfax Media Limited (ASX: FXJ) had recently announced about its plan of merger of NZME Limited and the New Zealand subsidiary of FXJ, while the finalization was said to be over by 15

th March 2017. On the other hand, under the New Zealand Commerce Commission (NZCC) process for the approval of the proposed merger, NZCC’s preliminary view is to decline the merger owing to unquantified concerns relating to plurality of media. The groups in question will review the draft determination and intend to take it up with NZCC. FXJ’s FY17 year-to-date overall group revenues for continuing businesses have been slightly below estimations but this subdued condition is expected to recover.

Domain’s overall revenue enhanced 2% while its total digital business grew 11%. In addition, the cost savings initiatives are ongoing. We maintain a “Buy” recommendation on the stock at the current price of $0.795

.PNG)

FXJ Daily Chart (Source: Thomson Reuters)

Southern Cross Media Group Ltd

.png)

SXL Details

SXL stake sold by Nine Entertainment Co Holdings: Southern Cross Media Group Ltd (ASX: SXL) had reported that their stake sale by Nine Entertainment Co Holdings (NEC) would boost the growth in FY 17. Moreover, SXL reported a 5.1% growth in the revenue in FY 16.

.png)

FY 16 Financial Performance (Source: Company Reports)

SXL made a five-year television affiliation agreement with Nine Entertainment, while renewed the affiliation agreement with Network Ten for NNSW, and executed long term agreement with the Australian Traffic Network.

Meanwhile, SXL stock rose 17.37% in six months (as of November 10, 2016) while trading at a slightly high P/E. Accordingly, we give an “Expensive” recommendation on the stock at the current price of $1.37

SXL Daily Chart (Source: Thomson Reuters)

Macquarie Media Ltd

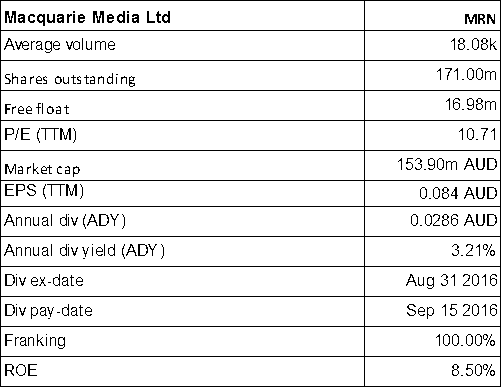

MRN Details

2CH was not sold within set timeframe:Macquarie Media Ltd (ASX: MRN) is conducting its AGM on November 15, 2016. The group has confirmed that 2CH was not sold within the timeframe allowed by its enforceable undertaking given to the ACMA in January 2015. This is after the ACMA objected to the terms of two separate proposed purchaser notices submitted by MRN prior to the required date of divestiture, which was 30th September 2016. The group otherwise remains confident of selling 2CH consistent with its expectations. We give an “Expensive” recommendation on the stock at the current price of $0.81

MRN Daily Chart (Source: Thomson Reuters)

APN News and Media Limited

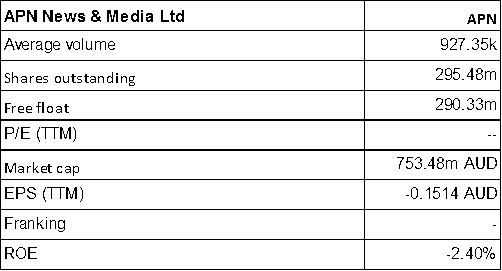

APN Details

Acquisitions and Capital Raising: APN News and Media Limited (ASX: APN) is raising over A$273 million via A$201 million entitlement offer and a fully underwritten A$72 million institutional placement of new shares. APN has already raised over A$254 million via the institutional placement. Moreover, APN has acquired the remaining 50% of Adshel that it did not already own.

The proceeds of the funds raised would be used to fund the acquisition. Additionally, APN has also entered into a binding agreement to acquire Conversant Media which was expected to be complete by the end of October 2016. Despite these efforts, the group’s financial performance is still weak which led to APN stock to fall over 21.8% in the last four weeks (as of November 10, 2016). Accordingly, we give an “Expensive” recommendation on the stock at the current price of $2.52

APN Daily Chart (Source: Thomson Reuters)

APN Outdoor Group Ltd

.png)

APO Details

Upgraded the earning guidance for FY 16: APN Outdoor Group Ltd (ASX: APO) has upgraded the previous earning guidance for FY 16. APN now expects the revenue growth in the range of 8.5% to 9.0% for FY 16 as compared to the previous guidance of 6.0% to 8.0%. EBITDA is expected to be in the range of $84 million to $86 million. Previously, the EBITDA was expected to be in the range of $79 million to $84 million, which the company had downgraded due to the weaker than expected demand between September and November due to an extended federal election and the after effects of the Olympic Games.

Moreover, APO has commissioned 32 new digital Elite screens in this year, and 4 further digital conversions are planned going forward. Despite this, APO stock fell 31.1% in the last three months (as of November 10, 2016), and we maintain an “Expensive” recommendation on the stock at the current price of $5.26

APO Daily Chart (Source: Thomson Reuters)

oOh!Media Ltd

.png)

OML Details

Funds raised for acquisition of Executive Channel Network:oOh!Media Ltd (ASX: OML) has raised $60 million from institutional placement to fund the acquisition of Executive Channel Network (ECN). Moreover, OML had undertaken a Share Purchase Plan (SPP) where the shareholder could apply for up to $15,000 of OML shares and the group now updated about closure of the plan and is said to issue about 415,101 new ordinary shares. However, OML stock is trading at a high P/E while we give an “Expensive” recommendation on the stock at the current price of $4.30

OML Daily Chart (Source: Thomson Reuters)

QMS Media Ltd

.png)

QMS Details

Turnaround to Profit in FY 16: QMS Media Ltd (ASX: QMS) reported a solid top line growth of 88% to $111.8 million in FY 16. Statutory NPAT reached $13.3 million as compared to FY15 pro forma net loss after tax of $4.3 million. The turnaround is due to the growth of digital, an expanded platform and contributions from acquisitions.

.png)

FY 16 Financial Performance (Source: Company Reports)

Moreover, QMS expects revenue and earnings growth in FY 17 based on the strong pipeline of new premium landmark digital sites and full year contribution from acquisitions, FY16 digital conversions, Auckland Transport and the Bali Airport concessions. In addition, QMS in FY 17 expects EBITDA of $35 million. The group will conduct its AGM on November 25, 2016. We give a “Speculative Buy” recommendation on the stock at the current price of $1.205

QMS Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.