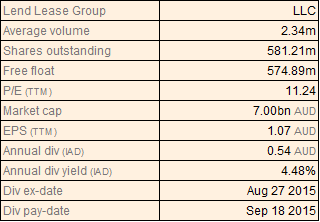

Lend Lease Group

LLC Dividend Details

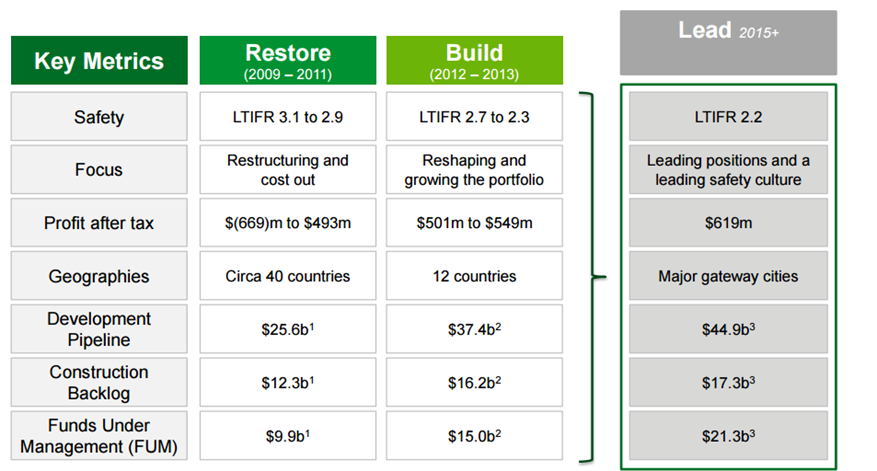

Built solid development pipeline:Lend Lease Group (ASX: LLC) has been developing a solid development pipeline and improved its development pipeline’s end value to $44.9 billion during 2015, against $34.7 billion in 2011. LLC enhanced its residential development business by 24% year on year (yoy) to 4,262 during fiscal year of 2015, as compared to the 2014 fiscal year. Lend Lease major urban regeneration projects reached over $8 billion driven by the new developments in Singapore, Malaysia and the United States. The group’s Investment management business rose by 31% yoy in funds under management to $21.3 billion in fiscal year of 2015. LLC enhanced its construction backlog revenue by 7% yoy to $17.3 billion, which includes $11.8 billion of new work and further $7 billion of building and engineering work. The group invested over $2.2 billion of production capital into its development pipeline leading to over 25 major residential apartment buildings and five commercial buildings in conversion or delivery globally. LLC already achieved a residential pre-sales book of over $5.2 billion for the coming three to four years, with over 45% likely to be settled before June 2017. Around 20% of the apartment pre-sales were from mainland China buyers, from which 30% of this would be settled before June 2017. Management reported that the group is the preferred bidder for over $7 billion worth of new work which is not included in the backlog revenue.

LLC’s major metrics (Source: Company Reports)

Stock Performance: Lend Lease profit after tax decreased to $619 million during fiscal year of 2015 as compared to $823 million in FY14. On the other hand, LLC has a decent balance sheet to fund its development pipeline with cash and equivalents of $750.1 million and gearing of 10.5%. The group has built a solid pipeline and improved pre sold residential revenue by 109% yoy in FY15 in Australia as well as UK. Meanwhile, the shares of Lend Lease corrected over 26.84% (as of November 13, 2015) year to date on investor’s concerns of the group’s performance given the tough market conditions. But, the group’s focus on urbanization projects and retirement living would drive support to the stock in the coming months. LLC enhanced its urbanization projects to over $33 billion in FY15 (comprising over 70%) against $16 billion in FY11 (comprising over 45%). The group’s retirement living units increased to 14,193 in FY15 from 12,417 in FY13. Lend Lease is also trading at attractive valuations with a P/E of 10.72x as well as has a decent dividend yield of 4.48%. Based on the foregoing, we give a “BUY” recommendation on the stock at the current price of $11.81

LLC Daily Chart (Source: Thomson Reuters)

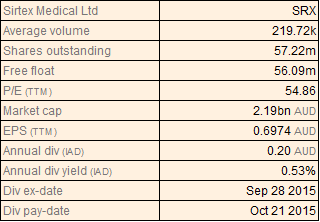

Sirtex Medical Ltd

SRX Dividend Details

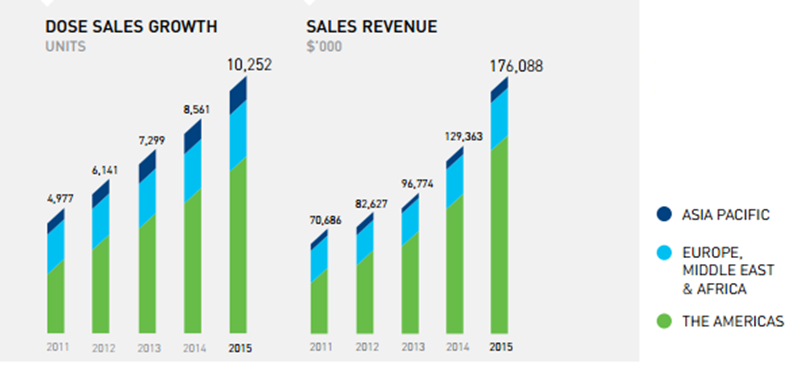

Delivered Outstanding FY15 performance and favorable Sirflox study: Sirtex Medical Limited (ASX: SRX) reported 19.8% yoy of dose sales to 10,252 and 36.1% yoy rise in sales revenue to $176.1 million in FY15, driven by solid SIR-Spheres microspheres business, expanding markets as well as capacity and favorable R&D. SRX Americas revenues surged over 42.5% yoy to $136.7 million driven by the improving SIR-Spheres microspheres in America with number of hospitals rising 17.7% yoy to 493 sites. EMEA revenues surged by 17.3% yoy to $32.4 million with dose sales increasing by 18.6% yoy to 2,273 during the period. The group got reimbursement from Israel further boosting its sales in the region. EMEA’s number of hospitals certified in SIR-Spheres microspheres improved by 11.5% yoy to 291 sites. As per the Asia Pacific (APAC) highlights, the regions revenue increased by 20.5% yoy to $6.9 million in FY15 driven by better selling prices of SIR-Spheres microspheres across many markets. The number of hospitals in SIR-Spheres microspheres across APAC surged by 17.4% yoy to 135 sites.

Sirtex Medical FY15 performance highlights (Source: Company Reports)

Stock Performance: The shares of Sirtex Medical delivered outstanding performance of over 89.74% (as of November 13, 2015) in the last six months, driven by solid results and favorable Sirflox study key findings. The Sirflox study key findings delivered additional 7.9 months’ progress in controlling tumors in the liver in patients with metastatic colorectal cancer treated with SIR-Spheres microspheres plus chemotherapy as compared to only chemotherapy. Patients who were treated with SIR-Spheres microspheres along with chemotherapy delivered a 31% lower risk of the tumors in their liver progressing against the patients treated with just chemotherapy. The five year compound annual growth rate for SRX in sales revenue is now 22.3% that trends above the volume growth. We believe that Sirtex Medical earnings performance would continue to grow in the coming periods and remain bullish on the stock. Accordingly, we give a “BUY” recommendation on the stock at the current price of $37.20

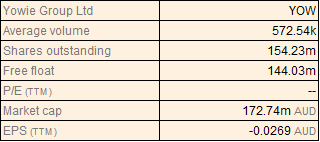

Yowie Group Ltd

YOW Details

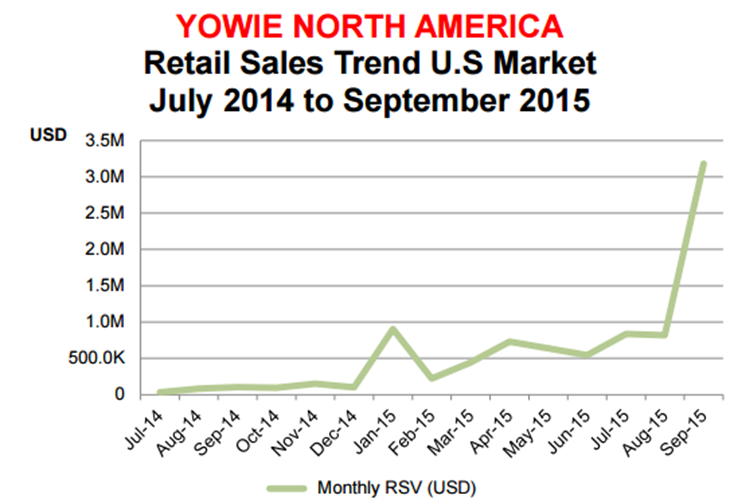

Delivered Spectacular returns to investors: Yowie Group Ltd (ASX: YOW) continued to deliver solid performance even in September 2015 quarter with retail sales value reaching over USD $4.8 million, which is more than double as compared to the last quarter. The group was selling its products in over 3700 Walmart stores. The group targeted to roll out Yowie confectionery all over the over 4300 Walmart stores in the United States, as a part of its strategy to boost the consumer penetration of its chocolate product. YOW is targeting the huge United states market opportunity, and accordingly, Yowie estimates a volume in the range of 700 to 800 million units and projects greater $2 billion value. Apart from the US, Yowie had already built more than 30% volume market share through Ferrero’s Kinder Surprise and secured over 36.2% value share in the Australian children's confectionery market.

Yowie Group North America Retail Trends market (Source: Company Reports)

YOW completed raising of over $10 million equity capital for funding its US rollout and targets to generate growth via national U.S. distribution and sales. Meanwhile, the shares of Yowie generated an outstanding performance this year, delivering over 109.17 %( as of November 13, 2015) year to date returns. We remain bullish on the stock given its focus on the US markets and based on the foregoing, we reiterate a “BUY” recommendation at the current price of $1.105

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.