Aurizon Holdings Ltd

.png)

AZJ Dividend Details

Cost reduction and productivity benefits: Aurizon Holdings (ASX: AZJ) is aimingfor a gross annual savings of AUD 310 million-AUD 380 million by fiscal 2018 from operations and support functions. It is expected that cost reduction and rollover to new commercial haulage contracts will steer the EBIT margin from 26% in FY15 to about 30% in FY18. The September Quarter updates highlighted volume drop for coal (-3% to 52.6mt), freight (-8%) and iron ore (-7%) but this was as expected by the market. The coal volumes were impacted by Goonyella volumes from BHP ramping up at the expense of AZJ along with the loss of German Creek contract. However, there was a 6% rise in coal volumes in NSW driven by the second full quarter of the Whitehaven contract. Iron ore volumes were down owing to contract declines from the previous year, however, this was partially offset by an additional service for Mount Gibson along with incremental volumes for Karara. However, tonnage of 6.3mt is in consensus with full year guidance for 24mt.

.png)

Quarter Performance (Source: Company Reports)

Although, September quarter results were more or less flat AZJ’s cost focus seems to deliver growth up till 2018. The company reported record levels of export volumes of coal and iron ore in FY2015. Statutory net profit after tax (NPAT) for the year was $604m, up 139%, and statutory earnings before interest and tax (EBIT) rose to $970m, a 109% increase over the prior year. AZJ earned on stable revenues of about $3.8 billion (FY2014: $3.8bn). Recently, the company announced for an extension of existing on-market buy-back of up to 107 million shares for a further of 12 months. As reported by the company, Aurizon continues to outperform the market in terms of Total Shareholder Returns (TSR) and has steadily increased its dividends over the last five years. The Company’s TSR increased by 7% in FY2015, and since IPO to 30 June 2015, it has increased by 117%. This compares to 6% and 44% for the S&P/ASX 200 Index in the respective period. Based on the foregoing and given AZJ’s efforts, we put a BUY recommendation for the stock at the current price of $5.47

AZJ Daily Chart (Source: Thomson Reuters)

Simavita Ltd

Rise in cash receipts and expansion of global footprint: Simavita limited (ASX: SVA) released its market updates for the September quarter wherein the highlight was the 148% rise in total cash receipts from customers to $223,816 over the total cash receipts from customers for the corresponding quarter in 2014 of $90,223. The roll out of the Software as a Service (SaaS) business model at the global level would add value. The company has also executed sales and marketing agreement with Paul Hartmann Pty. Ltd. which will boost growth as distribution of SIM™ in the Australian marketplace would be enhanced. At the same time, the company has signed agreements with two Canadian distribution partners to distribute SIM™ on a non-exclusive basis in Canada. The patent portfolio has been upgraded with the grant of six new patents during the quarter depicting SVA’s technology upgrade. The opportunity to expand market potential has also come from the recent funding ($469,450) by the Queensland Department of Health for the deployment of SIM™ in the acute care rehabilitation market. The company now has over 100 deployed and contracted sites.

.png)

Forecast for Global wearable computing devices (Source: Company Reports)

SVAseems to have a first mover advantage within the most dynamic and exciting part of the digital healthcare space. The company is certainly moving in the right direction given the growth so far and current developments. We see a buying opportunity given the above and the stock trading at its 52 week low price of $0.37

SVA Daily Chart (Source: Thomson Reuters)

AVEO Group

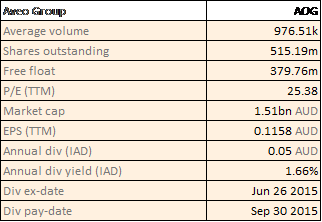

AOG Dividend Details

Robust performance coupled with returns from retiring living to drive growth: AVEO group (ASX: AOG) is expected to get a boost from the returns for retiring living given the increasing demand growth of the Australia’s age profile in the next couple of years, and rising property prices. Primarily, AOG expects to deliver 182 new units during the next year while ramping up its care and support services across the entire portfolio would continue at the back ofrobustsales momentum. The company thus aims to achieve underlying profit after tax of over $80 million in FY16, indicative of at least a 45% improvement on Aveo Group’s performance in FY15 and a full year distribution of 8 cents per security, which would represent a 60% increase on this year. This all comes at the back of the strong performance in FY15 wherein the company’s total retirement contribution was $53 million, an 18% improvement on the prior year. This was achieved given a record total retirement unit sales of 721 for the year. As a consequence, company booked an underlying net profit after tax of $54.7 million, indicative of a 30% rise on its FY14 result. The underlying earnings per security also rose to 10.9 cents per security in FY15, up 15% on FY14. Funds from operations were up 88% to $73.9 million, or14.8 cents per security, while its net assets per security lifted 3% to $2.85. Gearing saw a 2% drop to 13.8% and is at the lower end of its target range. This enabled the Board to declare a distribution of 5 cents per security for FY15, an increase of 25% on the prior year. Further, the commentary at the upcoming AGM is expected to depict robust sales in the residential land projects and insights on performance of the retirement assets. The company recently updated the total number of stapled securities that have been brought back and cancelled since the commencement of the buy-back on 4 September 2015 as 44,886. AOG is currently trading at a Price to earnings ratio of ~25x and a dividend yield of 1.66%. Based on the positive momentum, we give a buy recommendation for the stock at the current price of $2.97

AOG Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.