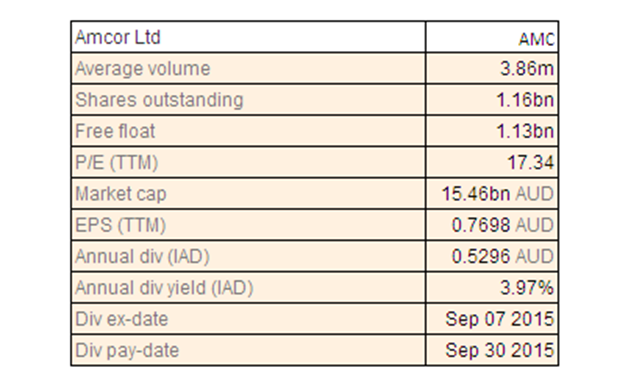

Amcor Ltd

AMC Dividend Details

Acquisition Update and Market Share Improvement: Amcor Ltd (ASX: AMC) has fallen about 8.18% in the last six months (as at December 11, 2015). The company lately announced the acquisition of privately owned Encon’s preform manufacturing business and the consideration payable will be USD 55 million. The acquired business will form part of the company’s Rigid Plastics business group. The acquisition is expected to reduce future capital requirements for the company’s existing Rigid Plastics business. Encon generated revenues of approximately USD 110 million from services proffered to both the company’s existing customers as well as new customers within the beverage, food and household segments.

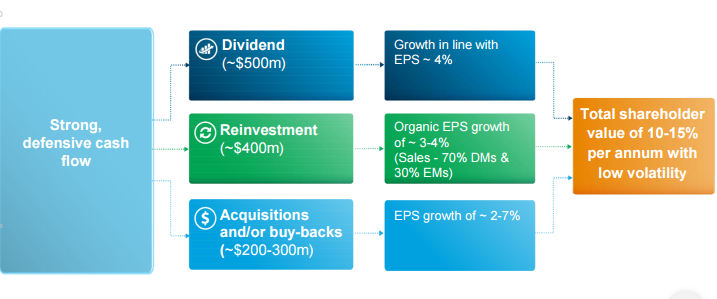

Shareholder Value Creation Model (Source: Company Reports)

The company is in a strong position today with a strong foundation for future growth. It is a focused portfolio of market leading businesses with a sizeable exposure to emerging markets with about one third of sales distributed across 27 emerging countries. The company has developed what it calls The Amcor Way, which is a set of unique and differentiated capabilities in areas like Sales and Marketing and procurement, which provides a real competitive advantage. Over many years, significant resources have been invested in developing these capabilities because they are critical for success and a real source of value. The USD 500 million share buyback announced sometime back has been completed; and under the program, the company repurchased a total of 48.5 million shares which represents 4% of shares on issue at the time when the announcement was made.

The performance in the first quarter of FY 2016 is consistent with the expectations outlined earlier and there are no changes to the outlook statements. The company has had a good start to the year and remains confident of delivering increased earnings during FY 2016 in constant currency terms. The Flexibles segment, accounting for approximately 2/3 of sales, have remained generally stable in terms of first quarter volumes in developed markets; and within emerging markets, volumes have continued to grow organically though below the long-term trend. The outlook for the full year is modestly higher earnings on a constant currency basis. In the Rigid Plastics Segment, in the North American Beverage Business, warm summer and some modest gains in market share have resulted in a solid start to the year with volumes ahead of the first quarter of FY 2015.

The Diversified Products and Bericap businesses have also had a good start for the year. However, at the current price, we consider the stock to be expensive and do not recommend a buy at this point in time.

AMC Daily Chart (Source: Thomson Reuters)

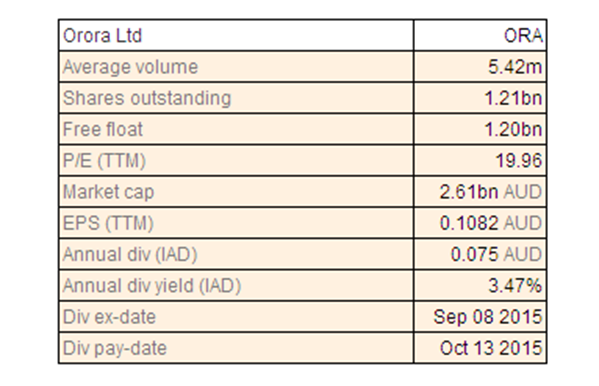

Orora Ltd

ORA Dividend Details

Improvement in sales and market share: Orora Ltd (ASX: ORA) surged 10.88% this year to date but corrected 6.55% in the last one month (as at December 11, 2015). The company was demerged from Amcor and has customer led operations in two business segments Australasia (Fibre Packaging and Beverage) and North America (Landsberg Packaging Solutions and Fibre Manufacturing businesses). FY 2015 result drivers comprised production ramp up of the B9 recycled paper mill in Botany, New South Wales, delivery of the remaining “self-help” cost reduction programs and double-digit earnings growth in both Australasia and North America irrespective of the weak market conditions.

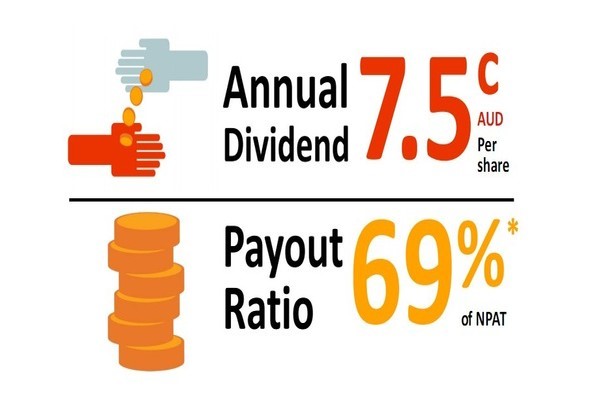

Dividend and Payout Ratio (Source: Company Reports)

Through financial discipline and improved working capital management, the company was able to convert earnings growth into cash thereby strengthening its balance sheet, lowering its debt service costs. ORA delivered about 26% growth in net profit after tax and EPS. The company’s Australasia business delivered EBIT of $ 181.6 million, increase of approximately 11.8% over the previous year. In the Beverage group, the company gained market share in the Class division and Beverage Can volumes remained stable, while the Fibre group reported higher sales of corrugated board in New Zealand and generally stable volumes elsewhere. The operations in North America were repositioned during the year from being a distributor of commodity products to a packaging solutions provider. The business is strongly delivering sales growth in constant currency of 6.2% to USD 1.2 billion and earnings growth of 14.1% to USD 59.9 million. There has been an increase of revenues by 8.7% for the Landsberg Packaging Solutions division through higher sales to existing customers, growth and market share in the benefits of the July 2014 acquisition of Worldwide Plastics. The group is now on track to deliver the target of 20% return on investment acquisition hurdle rate in FY 2016 one year ahead of the criteria.

In the first quarter of FY 2016, the economies of Australia, New Zealand and North America will be flat with such conditions to remain for the rest of the financial year. Trading results for the first quarter are ahead of the same period in the previous year and in line with expectations. However, we note that the company has lost the Asahi liquor beverage can contract from mid of 2016 to Visy which will impact the FY17 earnings. Although the company has reported for initiation of legal proceedings in relation to the tendering process, the impact is yet to be ascertained fully.

ORA is trading at a high P/E ratio, and we believe that the stock is expensive and do not recommend a buy at the current price.

ORA Daily Chart (Source: Thomson Reuters)

Pact Group Holdings Ltd

PGH Dividend Details

Subdued Trading Conditions: In FY 2015, Pact Group Holdings Ltd (ASX: PGH) delivered another year of solid results with product innovation, improved productivity and acquisitions contributing to growth. The company reported statutory net profit after tax and before significant items of $ 85.2 million up 43% over the previous year. Sales revenue grew by 9.3% to $ 1.24 billion and EBITDA before significant items by 5.3% to $ 208.7 million. The directors declared a full-year dividend of $ 0.10 per share franked at 65% and the total dividend for the year was 19.5 cents per share providing good returns for shareholders. The group continues to generate strong cash flows with underlying operating cash flow of $ 215 million, up by 8% over the previous year.

Performance (Source: Company Reports)

The company expects to have underlying profit growth based on the Sulo and Jalco acquisitions that are progressing well. The previous earnings guidance as provided at the FY15 result has been maintained with expectation to achieve higher revenue and underlying earnings in FY16 as compared to FY15. However, the performance is subject to trading conditions that have been identified as subdued with PGH expecting poor demand from the seasonal industries, namely, agriculture in Australia and New Zealand and global dairy markets. However, stability through a diverse end-market and customer mix does exist to some level.

Hot summer may benefit the food and beverage business. The stock has surged 8.47% this year to date (as at December 11, 2015) and is trading at a high P/E ratio of about 21x. We think that at the current price the stock is expensive and overvalued leaving little room for any upside.

PGH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.