Insurance Australia Group Limited

.png)

IAG Details

Mixed FY16 results: Insurance Australia Group Limited (ASX: IAG), engaged in the underwriting of general insurance and related corporate services and investing activities, has announced for a $300 million off-market share buy-back while reported for subdued conditions impacting the Australian and New Zealand market. IAG reported for flat outlook for 2017 premium growth while FY16 gross written premiums (“GWP”) plunged 0.6% to $11,367 million. There was a 14% drop in Net Profit After Tax to $625 million while total dividends rose by 24%. The underlying insurance margin surged by 90 bps to 14%. The group also reported high growth in Asia division.

.png)

IAG’s capital position (Source: Company Report)

IAG had also earlier announced for issuing NZ$350 million of subordinated unsecured notes. The company’s relationship with Berkshire Hathaway is also expected to continue to support the group going forward. So, we maintain our “Hold” recommendation on this dividend yield stock at the current price of $5.67

IAG Daily Chart (Source: Thomson Reuters)

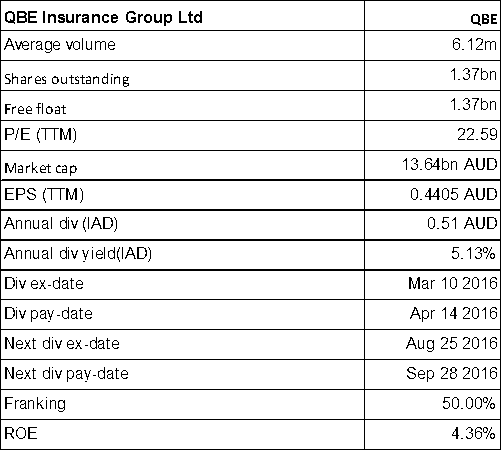

QBE Insurance Group Ltd

QBE Details

Weak half year results: QBE Insurance Group Ltd (ASX: QBE), engaged in underwriting general insurance and reinsurance risks etc., is trading ex-dividend on August 25, 2016. The group has reported quite disappointing results for the half year ended in June as compared to last year. There was 3.1% deterioration in attrition claims ratio in underwriting excellence. The group’s profit after tax fell 46% to $265 million against the corresponding period of last year on the back of $283 million adverse discount rate adjustment as risk-free rates used to discount net outstanding claims decreased. Underwriting profit also slipped about 5%.

.png)

Half yearly results 2016 (Source: Company Report)

But QBE is an award winning company in its car insurance sector wherein “CANSTAR” generated outstanding value in 2016. QBE has also increased its cash remittances from $201 million to $648 million.

On the other hand, we believe that the group would continue to face performance pressure in the coming months and we maintain our “Expensive” recommendation on the stock at the price of $10.10

QBE Daily Chart (Source: Thomson Reuters)

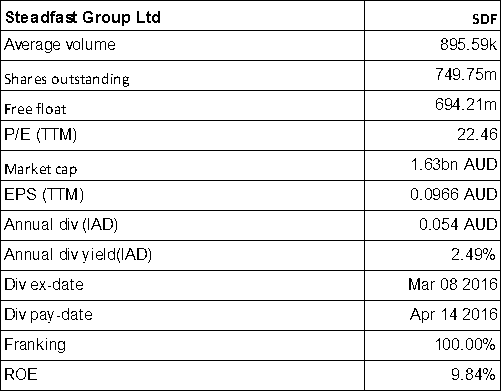

Steadfast Group Limited

SDF Details

FY16 Solid performance: Steadfast Group Ltd (ASX:SDF), the general insurance broker, announced FY16 underlying NPATA growth of 45% to $82.0m while underlying revenue is of the order of $459.5m, up 54%. Underlying EBITA of $129.6m is also up 43% while cash EPS of 11.00 cents per share is up 12.4%. Final dividend (fully franked) of 3.6 cents per share, up 20%. The group has provided underlying NPATA guidance of $85m to $90m for FY17. SDF is continuing its growth efforts by launching new system and focusing on cost effective methods. Meanwhile, the group had reported that 99% of brokers are considering switching based on the survey of Steadfast Network Broker Principals in Apr 2016, at Steadfast Convention. Other underwriting agencies are dependent on third party providers for their systems whereas SDF has acquired underwriter central which not only saves cost but eliminates third party. Accordingly, the group’s GWP enhanced by Calliden and the QBE agency acquisitions.

.png)

Network Brokers (Source: Company Reports)

SDF stock rose over 35.63% in the last six months (as of August 23, 2016) and we recommend a “HOLD” at current price of $2.13

SDF Daily Chart (Source: Thomson Reuters)

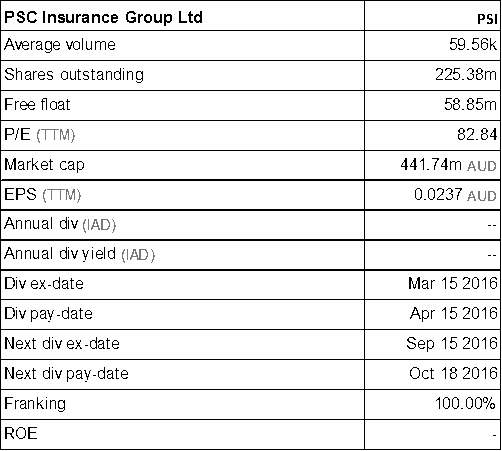

PSC Insurance Group Ltd

PSI Details

Robust revenue growth: PSC Insurance Group Ltd (ASX: PSI), engaged in insurance intermediary business (focusing on general insurance market, underwriting agencies, wholesale insurance broking, etc.), reported for 30.1% growth in statutory revenues from ordinary activities to $67.77m while profit after tax attributable to members as well as net profit have been up 55.4% for the financial year ending June 30, 2016. Underlying revenue is up 34% on the prior corresponding period to $67.5 million and ahead of prospectus expectations of $60.0 million. Revenue growth was the result of a combination of both acquisitions and organic growth from existing businesses. Overall, FY16 was outlined as a landmark year for the group with the completion of a successful IPO. The stock has risen 23.27% this year to date (as at August 23, 2016) and is trading at its 52-week high price and at a high PE ratio. We believe that the stock is “Expensive” at the current price of $2.06

PSI Daily Chart (Source: Thomson Reuters)

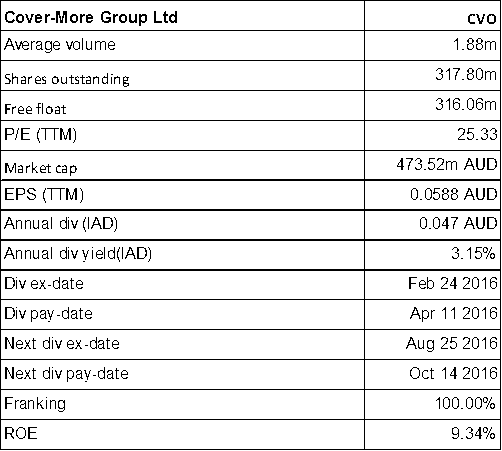

Cover-More Group Ltd

CVO Details

Softness in full year results but other efforts going well: Cover-More Group Ltd (ASX: CVO), the integrated travel insurance and medical assistance provider, soared over 10.4% (as on August 23, 2016) in the last month. CVO has signed an agreement with Great Lakes Australia and this agreement gives a change for underwriter payment on the basis of generalised linear modelling (GLM), effective from 1 July 2016, wherein CVO could hire alternative underwriting partners. GLM is designed to reduce volatility by ensuring payment of underwriting premiums which would more closely reflect expected claims outcomes, and offers greater alignment and certainty to their distribution and underwriting partners. This gives an opportunity to CVO to cover alternative underwriters in Australia, New Zealand and the United Kingdom. However, the full year profits fell by 27.5% while group gross sales increased by 7.6% to $502.1 million over prior corresponding period.

Nonetheless, CVO had a decent performance in the second half given stabilisation in premiums paid out to underwriters. Further, gross sales into Asia grew at more than 20%. The stock is trading ex-dividend on August 25, 2016. We give “Buy” recommendation on this dividend yield stock at the current price of $1.495

CVO Daily Chart (Source: Thomson Reuters)

AUB Group Ltd

.png)

AUB Details

Strong Half yearly performance: AUB Group Ltd (ASX: AUB), engaged in insurance broking services and the distribution of ancillary product, rose over 11.4% (as of Aug 23, 2016) in last six months as the group delivered a solid half yearly result. The group’s reported NPAT rose over 72% on a year on year (yoy) basis in the first half of 2016 while the adjusted NPAT enhanced by 3.5% yoy for the same period. AUB sold its investments worth $6.2m after tax, in Strathearn Insurance Group Pty. AUB also declared fully franked interim dividend of 12 cents to its shareholders and it was paid on April 29, 2016. Meanwhile, the group reported that they would follow “owner-driver” business model to serve their clients with total risk solutions strategy which improves client value proposition and diversifying income generation.

AUB business snapshot (Source: Company reports)

AUB had also enhanced its debt flexibility and increased the limit of its funding facility to $79.45m on improved terms with extended tenure till November 30, 2016. We maintain our “Hold” recommendation on the stock at the current price of $10.20, ahead of its results on August 25, 2016 and would review it again post the result update.

AUB Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.