G8 Education Ltd

.png)

GEM Dividend Details

Outstanding Dividend Yield: Recently, G8 Education Ltd (ASX: GEM) announced for early redemption of $155 million Singapore dollar notes in view of the funds raised with regards to Affinity takeover that did not finally succeed. Lately, the company also completed the acquisition of 13 premium childcare and education centres from a number of different vendors. The total purchase price of $29.7 million (excluding transaction costs) will be funded from existing cash reserves. The purchase price is 4.1 times the expected EBIT for the 12 months post settlement (completed November 30, 2015). These centres are foreseen to contribute to EBIT immediately upon settlement. With these acquisitions, the number of places have increased by 1,000 and this leads to total number of places of 36,125 per day in the company's Australian portfolio. In fact, acquisitions announced prior to November 12, 2015 were settled. For the half-year ended 30

th June, 2015, GEM recorded a growth of 66% in its total revenue to $310.9 million, while net profit after tax grew 73% to $28.2 million.

.png)

Group centre portfolio (Source: Company reports)

Meanwhile, earnings before interest and tax surged 93% to $58.1 million led by acquisitions and organic growth. Operating cash flow increased to $35.4 million for the first half 2015 compared to $14.5 million in the year ago period. With high dividend yield and strong company fundamentals, we rate this stock a “Buy” at the current share price of $3.38

.png)

GEM Daily Chart (Source: Thomson Reuters)

FlexiGroup Ltd

.png)

FXL Dividend Details

Strong outlook: Recently, FlexiGroup Ltd (ASX: FXL) recently completed retail component of its 1 for 4.46 accelerated non-renounceable entitlement offer of new shares announced on October 27, 2015. The company also announced a transformational acquisition of Fisher & Paykel Finance that comprises upfront cash consideration of $ 234 million and deferred consideration of A$ 61 million, and is expected to be high single digit Cash EPS accretive to FlexiGroup on a pro-forma basis, including expected synergies. On closure of the F&P Finance acquisition, FlexiGroup will achieve a significant foothold in the New Zealand consumer market with approximately 38% of its receivables originating in New Zealand compared to 11.6% contribution in FY15.

.png)

Consistent profitability and returns (Source: Company reports)

FlexiGroup also reaffirmed full financial year 2016 cash NPAT guidance, with the group remaining on track for the full year cash NPAT of A$92 million - A$94 million (excluding F&P Finance acquisition) driven by leveraging capex investment and acquisitions. Dividend guidance is also reaffirmed, with full financial year 16 dividend expected at the lower end of 50% - 60% of cash NPAT. Full year 2015 dividend payment of 17.75 cents per share, indicated a growth of 8% over the prior year.

For full financial year 2015, FlexiGroup recorded cash NPAT growth of 6% to $90.1 million. Group volumes increased 5% to $1,136 million and receivables rose 8% to $1,428 million driven by strong performance in Interest Free Cards, Certegy and the high growth New Zealand portfolio fuelled by the Telecom Rentals Limited (TRL) acquisition. With high dividend yield and a moderate P/E, we rate this stock a “Buy” at the current share price of $2.74

FXL Daily Chart (Source: Thomson Reuters)

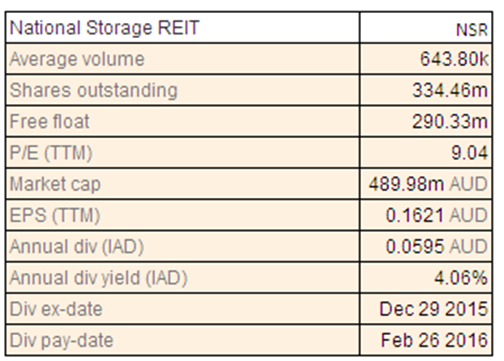

National Storage REIT

NSR Dividend Details

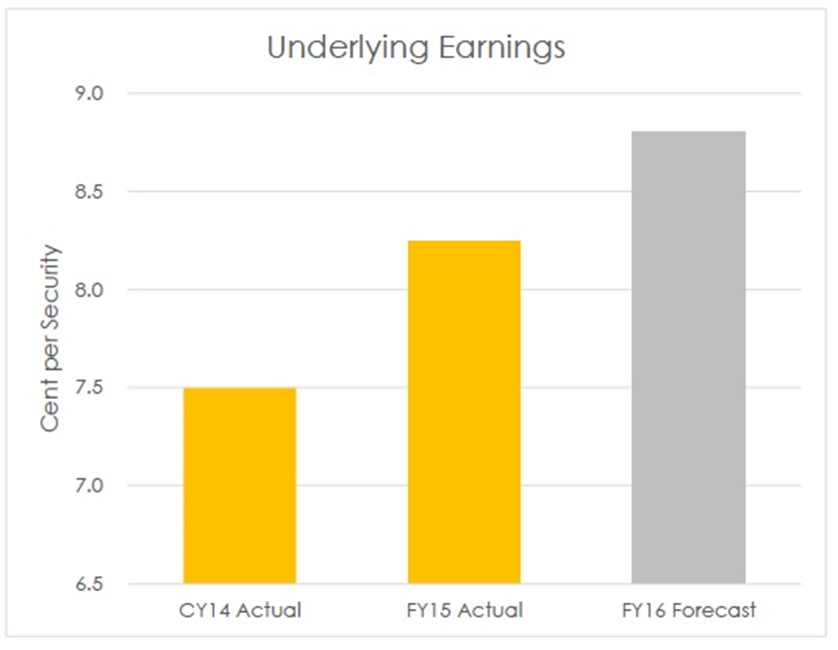

Expanding presence in Sydney: Recently, National Storage REIT (ASX: NSR) announced that the estimated distribution payable for the July to December period is 4.3 cents per stapled security, indicating a 100% pay-out ratio of the estimated year end underlying earnings of $14.3 million. Besides, the company also affirmed its previous earnings guidance of $29 - $29.5 million (8.7 - 8.8 cents per security) for financial year 2016. Distribution pay-out ratio is expected to remain in between 90% to 100% of underlying earnings.

Earnings Forecast (Source: Company reports)

National Storage recently announced that it has entered into arrangements to acquire the business and long term leasehold for three self-storage centres in Sydney for $10.7 million which will be funded from the company's debt facility. The management believes that this acquisition will strengthen its Sydney footprint and bring the total number of centres owned or operated in New South Wales to 13. In FY15, National Storage completed 21 acquisitions with a further four until November 2015. In total it has 91 centres under ownership, operation or management. NSR management commented that its 2015 results were in line with its guidance with total revenue rising 39% to $63.7 million led by delivery of company's strategy to maximize returns through multiple revenue streams. A-IFRS profit after tax stands at $48.7 million, an increase of 213% from previous year.

Total assets under management in FY15 rose 35% to $740 million. With decent dividend yield, we rate this stock a "Speculative Buy" at the current share price of $1.50

NSR Daily Chart (Source: Thomson Reuters)

Village Roadshow Ltd

.png)

VRL Dividend Details

Focusing on Digital business growth: Recently, Village Roadshow Ltd (ASX: VRL) announced that a U.K. subsidiary has acquired 80% of the UK-based Opia business for GBP 24 million, adjusted for surplus cash, with deferred consideration payable if future earnings targets are met. Existing senior management will retain a 20% holding in Opia, which will become part of VRL’s Digital Division along with earlier acquired Edge Loyalty Systems Pty Ltd. The acquisition of Opia is expected to be earnings accretive and contribute positive cash-flow to VRL from acquisition date and synergies from the combined Edge/Opia businesses are expected to generate incremental revenue. Opia’s EBITDA is expected to be approximately GBP 6 million per annum in the first full year of acquisition and VRL’s share of this will be 80%. The net profit after tax contribution from Opia in the first full year of consolidation is expected to be about A$5.8 million. For FY15, VRL's revenues increased to A$ 967.6 million from A$ 939.2 million from previous year. The VRL group reported a lower attributable net profit of A$ 43.9 million for the year ended 30 June 2015.

VRL’s Cinema Exhibition division was the standout performer in its segment portfolio in 2015. Looking ahead, VRL is all set for future growth with developments across its divisions. Majorly, it has signed binding framework agreement and joint venture agreement for establishment of a funds management business with CITIC Trust Co. Ltd., for development opportunities throughout Asia, with a specific focus on China. We rate this stock a “Buy” at the current share price of $6.89

.png)

VRL Daily Chart (Source: Thomson Reuters)

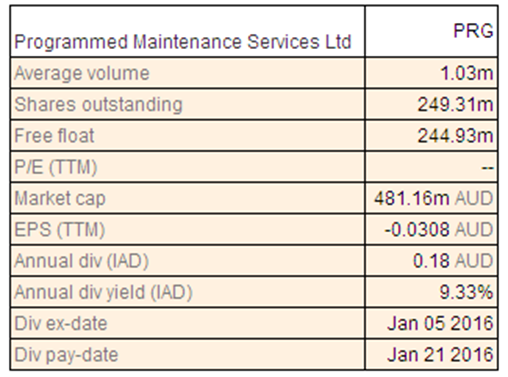

Programmed Maintenance Services Ltd

PRG Dividend Details

Retiring debt from sale of vessels: Programmed Maintenance Services Ltd (ASX: PRG) announced a conditional agreement to sell its vessels (excluding one remaining vessel), plant and other equipment operated by its subsidiary Broadsword Marine Services to Bhagwan Marine Services subject to further procesess including due diligence, bank and board approvals. Based on further inspection and other normal vessel sale terms, the remaining vessel’s sale has been reported to be subject to a separate offer from an overseas buyer. The combined sale price for all vessels is $ 25 million and payment terms for the former are spread over two years. Proceeds from the sale will be used to retire debt. The company belives that the above transaction with regards to the Broadsword business will remove the risk of further volatility in earnings.

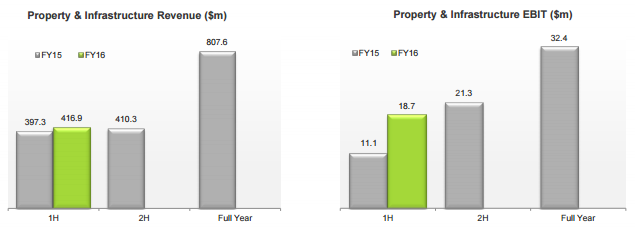

Property & Infrastructure Result (Source: Company reports)

Results for the first half to 30 September 2015 showed an after-tax profit of $ 12.8 million before non-trading items compared to $ 12.1 million in the previous year. Group revenues at $ 710 million was similar to the previous period with a 5% increase in the Property and Infrastructure division revenue being offset by lower revenue witnessed by the Resources division. The Workforce division revenue increased after three years of decline providing evidence of positive signs of the growth. In our opinion, the company looks to have growth potential in the future with prospects of an upside and we would recommend a “Speculative Buy” at the current price of $1.97

PRG Daily Chart (Source: Thomson Reuters)

Service Stream Ltd

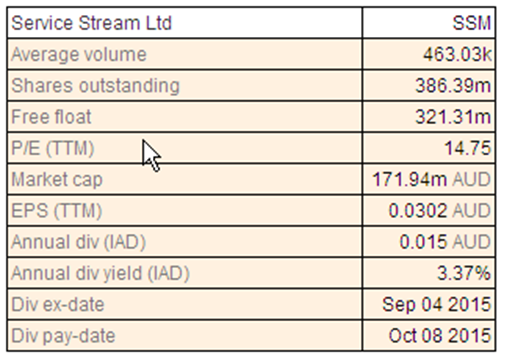

SSM Dividend Details

New Operations and Maintenance Agreement with nbn: Service Stream Ltd (ASX: SSM) announced that it has signed a new four year Operations and Maintenance Master Agreement for the provision of operations and maintenance field services to nbn. Accordingly, SSM will be performing operations and maintenance field service works, including service activation, service assurance, network assurance and preventive maintenance to be provided across the nbn fixed line multitechnology network. Fieldwork is expected tp begin in March 2016, with services being delivered within the defined contracted areas across Queensland, New South Wales and other states. With an expectation of volume growth under the contract in synergy with expansion of the nbn infrastructure rollout program, the company expects to have revenues of approximately $ 40 million in the first year. The financial highlights for FY15 show revenue growing to $ 411.3 million from $ 389.6 million of FY14 with the increase driven by growth in fixed communications associated with the ramp up in nbn-related activities. However, this was offset by decline in Energy and Water. EBITDA was up to $ 25.4 million from $ 16.6 million.

A steady focus was maintained on managing productivity and cost control. However, we consider that the current stock price overvalues the stock at the moment.

SSM Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.