Ramsay Health Care Limited

.png)

RHC Details

Positive outlook despite short term challenges: Ramsay Health Care Limited (ASX: RHC) withdrew its joint venture with Chinese company Jinxin in the city of Chengdu, indicating the group’s cautious stance while expanding its business.

Investors have been positive on the stock despite the Brexit outcome, even though RHC has over 36 hospitals in the U.K. and derives over 11% of its revenue from the region. The stock rose over 13.1% in the last four weeks (as of July 28, 2016) and delivered 21.7% returns in the last three months. In addition, Ramsay has upgraded the guidance of Core NPAT and Core EPS growth to 15% to 17% for full FY 2016 (previously 12% to 14%). We give a “Hold” recommendation on the stock at the current price of $78.79

.PNG)

RHC Daily Chart (Source: Thomson Reuters)

Sydney Airport Holdings Limited

.png)

SYD Details

Weak domestic demand: Sydney Airport Holdings Ltd (ASX: SYD) may think of cutting back on plans to put new or larger planes in operation, and the possibility of the airlines cutting capacity plans, in turn reducing overall capacity growth, may happen in case the domestic demand remains weak. Moreover, the oil prices recovery could also affect the fuel prices.

.png)

June Sydney Airport Traffic Performance (Source: Company Reports)

In line with the above, SYD reported that airport traffic from domestic passengers rose only 5.3% during this year to date as of June 2016 as compared to international growth of 9.3% for the same period. Trading at a high P/E, we give an “Expensive” recommendation on the stock at the current price of $7.56

.PNG)

SYD Daily Chart (Source: Thomson Reuters)

Woolworths Limited

.png)

WOW Details

Restructuring efforts to drive growth: Woolworths Limited (ASX: WOW) reported about selection of a new supplier over Murray Goulburn to manufacture and pack a range of its private label products including cheese, UHT, adult milk powder and cream. Moreover, the group is incurring huge restructuring efforts and implementing a new operating model to enhance accountability and performance.

Accordingly, the group expects to incur restructuring costs of $959 million ($571 million non -cash) or $766 million after tax for financial year 2016 results. We believe that the group’s investment in pricing would deliver returns in the coming periods. Trading at a decent dividend yield, we maintain our “Buy” recommendation on the stock at the current price of $23.41

.PNG)

WOW Daily Chart (Source: Thomson Reuters)

Telstra Corporation Ltd

.png)

TLS Details

Declining fixed voice revenue: Telstra Corporation Ltd (ASX: TLS) reported that the company is positioning itself in a manner which would change the mix of its existing products given the migration to NBN. Telstra has also recently acquired HCS Business Assets for $4.5m from Inabox Group Ltd. On the other hand, the group’s core fixed voice revenue has declined even though the NAS revenue has grown strongly. Moreover, fixed voice has better margins than the NAS margins.

The market expects TLS to report for flat earnings before interest tax depreciation and amortization for fiscal 2016 given the dip in mobile and fixed voice revenue. There are also challenges in terms of sluggish growth in industry top line, high competition, higher customer churn and softness in profitability. Amidst all the above, TLS’ chief operations officer, Kate McKenzie is all set to retire. We believe that the stock is “Expensive” at the current price of $5.77

.PNG)

TLS Daily Chart (Source: Thomson Reuters)

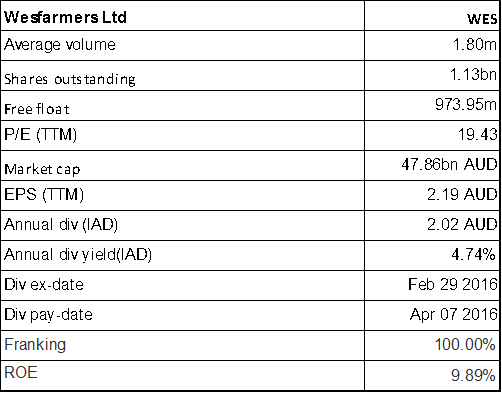

Wesfarmers Ltd

WES Details

Challenging Outlook: Wesfarmers Ltd(ASX: WES) recently reported that for Curragh, the metallurgical coal production fell 19.3% to 7,316,000 tonnes for twelve months ended on June 2016, while steaming coal production rose by 2.4% to 3,263,000 tonnes. On the other side, the Brexit outcome could hurt the group’s Homebase acquisition in UK as there could be a slowdown in UK. This investment in the UK is likely to be under pressure due to negative currency impact, with the value of sterling versus the Aussie dollar declining. Moreover, WES has high levels of seasonal stock of more than $100 million in the first half of 2016.

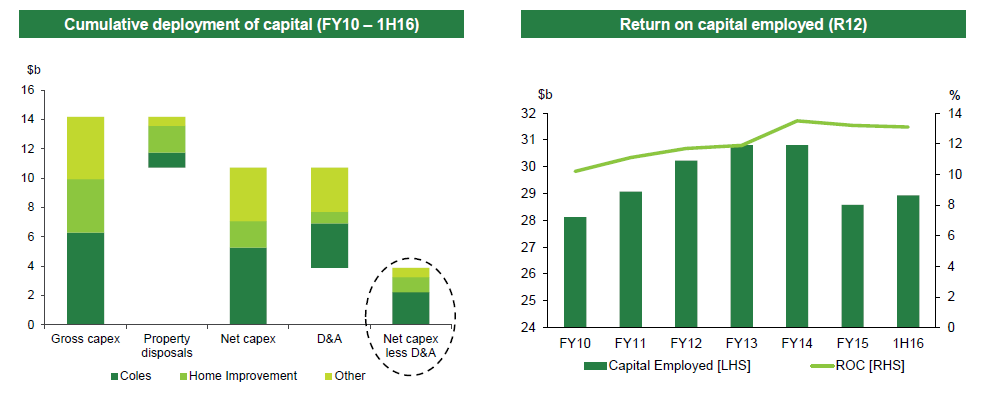

Deployment of Capital and Return on Capital Employed (Source: Company Reports)

The group incurred restructuring costs and provisions of $145 million to significantly rebase Target and expects EBIT loss in Target for FY2016 of approximately $50 million, due to high seasonal clearance activity and lower gross margins. The non-cash impairment of $1,100 million to $1,300 million pre-tax is to be recorded in Target for FY 16. We give an “Expensive” recommendation on the stock at the current price of $42.93

WES Daily Chart (Source: Thomson Reuters)

Transurban Group

.png)

TCL Details

Increase in toll revenue: Transurban Group (ASX: TCL) reported a toll revenue growth of 17.4% in its June quarter 2016 due to increase in revenue to $500 million as compared to prior corresponding period (pcp). The Proportional toll revenue, which gives the most accurate reflection of the portfolio’s performance, increased by 17.5% from the pcp, to $513 million. The revenue growth for the period is favorably impacted by the Easter holiday period which shifted from the June quarter in 2015 to the March quarter in 2016.

.png)

Revenue Data (Source: Company Reports)

Meanwhile, Transurban Queensland would partner with Brisbane City Council for the upgradation project of Inner City Bypass (ICB) for $80 million. On the other hand, TCL is trading at an unreasonable P/E and close to its 52-week high price. We give an “Expensive” recommendation on the stock at the current price of $12.56 , and would review the stock at a later date.

.PNG)

TCL Daily Chart (Source: Thomson Reuters)

REA Group Limited

.png)

REA Details

Ongoing global expansion: REA Group Limited (ASX: REA) has acquired Flatmates.com.au Pty Ltd, which is a market leading player in share accommodation in Australia, as in May 2016. REA has also completed the acquisition of Asia’s focused portal iProperty Group in South East Asia as well as invested in US’s Move Inc. Moreover, REA has increased the marketing initiatives in Italy to continue its expansion in Europe. The company is also looking to expand in other parts of Asia and recently moved from its Melbourne office to a significantly larger site to help achieve its expansions’ targets.

.png)

REA Financial Performance (Source: Company Reports)

On the other hand, REA reported a strong revenue increase of 20% in March quarter against prior corresponding period and expanded its free cash flow by 31% on a year-on-year (yoy) basis. We give a “Hold” recommendation on the stock at the current price of $65.27, ahead of its FY16 result on August 09, 2016.

.PNG)

REA Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.