-

Ongoing performance pressure: Woolworths Limited (ASX: WOW) recently got a BBB+ rating from Moody’s for its long-term senior unsecured note with a stable outlook from A credit rating with negative outlook. The group continued to witness pressure on sales, which decreased by 0.2% yoy to of $60.7 billion impacted by the group’s Australian Food, liquor and petrol as well as General Merchandise segments. Woolworths Earnings before Interest and Tax also marginally fell by 0.7% yoy to $3.75 billion in FY15, affected by the decrease in EBIT for general merchandise and hotels by 25.3% and 14.9% on a year over year basis. Meanwhile, the group managed to slightly improve its net profit after tax by 0.1% yoy to $2.5 billion in FY15, while the earnings per share fell by 0.7% yoy to 195.2 cents. However, the net profit after tax plunged by 12.5% yoy to $2.15 billion during the year.

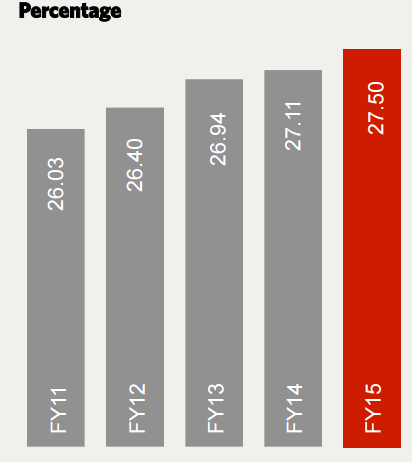

Improving Gross profit margin from continuing operations before significant items (Source: Company reports)

-

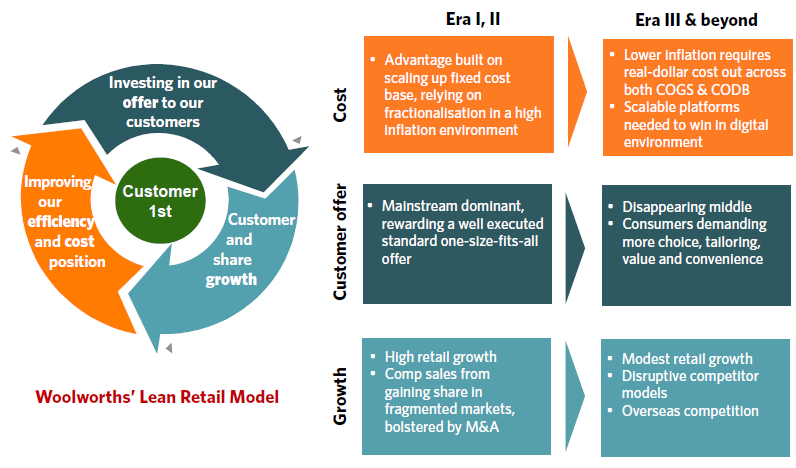

Reorganizing business to battle competition: Woolworths is making efforts to revive its business across all the segments, given the intense market competition. The group launched an Australian Supermarket Customer 1st Strategy, thorough which it estimates an expansion in sales over the next three years. WOW is focusing on improving shopping experience, by giving offers and enhancing communication. The group invested over $200 million on price during the second half of FY15, and estimates to do the same in the first half of FY16. As a result, over 9,000 items from WOW were cheaper as compared to its major competitor Coles during fourth quarter of 2015, based on the Nielsen Homescan reports. Woolworths is also focusing on team hours during FY15 and FY16 to enhance the customer service and availability as well as improving fruit and vegetable offers, leading to a better Net Promoter Score. The group’s transition to Lean Retail Model helped them to achieve significant costs savings of >$500 million, ahead of their targets. On the other hand, the groups fiscal year of 2016 performance would depend on its further investments in price, service and experience.

Lean Retail Model (Source: Company reports)

-

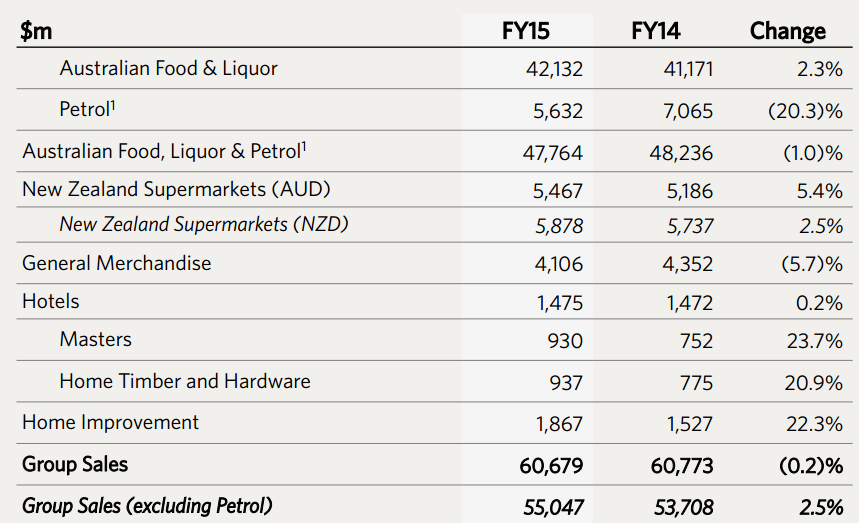

Segment Highlights: Meanwhile, Woolworths Australian Food and Liquor comparable sales during July and August fell by 0.9% as compared to pcp, while the total fiscal year 2015 sales reduced by over 1% yoy to $47.8 billon. Even, the General Merchandise segment got affected, with sales and EBIT falling by 5.7% and 25.3% on a year over year basis for FY15, due to the group’s BIG W business transformation. Systems implementation issues and clearance of unproductive inventory contributed to this decline. This transition to the new merchandising system is estimated to impact the stock availability and inventory clearance even for the second half of the year. The group estimates a better FY16 performance, depending on the Christmas trading period performance. Hotel sales marginally improved by 0.2% yoy to $1,475 million in FY15, but the EBIT plunged 149% yoy to $234.5 million due to additional Victorian gaming tax from May 2014 and the divestment of a portfolio of freehold hotel sites in October. Home Improvement delivered a revenue increase of 22.3% yoy in FY15, with masters and home timber &hardware rising 23.7% yoy and 20.9% yoy respectively. WOW currently has over 20% of Masters stores in the new format wherein the average sales per store is greater than 30% as compared to the original format stores. Woolworths would refit three stores in NSW during first half of 2016 as well as intends to open further new stores in FY16 at major metropolitan markets. The group is also targeting online sales, which rose by 15.6% yoy to $1.42 billion during FY15 across Food, Liquor and General Merchandise.

Segment Performance (Source: Company reports)

-

Stock Performance: Woolworths shares tumbled over 10.7% in just last four weeks, due to credit rating decline from Moody’s and lower than estimated FY15 results. Moreover, the group has been under pressure from quite a while now, due to intense competition from peers like Coles, Costco and Lidl. Accordingly, the shares slumped more than 16% in last six months. On the other hand, the group declared a solid dividend of 72 cents per share, resulting in the total fiscal year of 2015 dividends to 139 cents per share, which is a 1.5% increase as compared to the earlier fiscal year. Woolworths has been heavily rewarding the clients delivering a dividend yield of 5.3%. The recent decline have placed the shares at cheaper valuation with P/E of 13.34x, as compared to its peers. Based on the foregoing, we reiterate our “BUY” recommendation on WOW at current price of $25.23.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.