Seven West Media Ltd

.png)

SWM Dividend Details

Diversifying business to offset FTA market pressure: Seven West Media Ltd (ASX: SWM) commented on its trading update at the AGM stating FY16 EBIT expected to be at the bottom end of the minus 5-10% guidance range. SWM also stated about the flat TV market growth given performance in 1Q16 and challenges in the publishing advertising segment. However, group costs have been expected to be below prior corresponding period. The company reported a revenue decrease of 4.7% on a year over year basis to $1,774.7 million for fiscal year of 2015 due to ongoing impact of its core TV segment revenues (which accounts 72% of the overall revenues). TV segment revenues plunged by 2% year on year (yoy) to $1,279.2 million during the year impacted by the declining advertising revenues for TV. Therefore, the group has been diversifying business to offset Free to Air (FTA) market pressure and also focusing on online as well as other communications. The group’s Yahoo7 (partnership with Plus7) has over 3.1 million daily active users, wherein its mobile audiences rose by 31%. More than 130 million video streams were served during the fiscal year, which is an improvement by 15%. SWM’s Presto SVOD (launched during third quarter of 2015) service growth is also on track. The group is also making new distribution agreements with third party platforms and entered into media partnership with Racing Victoria on Racing.com. SWM improved its digital video revenue by 66% and witnessed a 17% growth in content sales.

.png)

Total Revenue (Source: Company Reports)

Outstanding dividend yield: The group entered into a new 6-year deal with the Australian Football League (AFL) for the 2017 to 2022 seasons which would add some support to its TV business. Moreover, SWM cost control efforts generated a 2.4% yoy decrease in operating costs during FY15 and the group continues to focus on improving its efficiency. Seven West is also boosting its balance sheet and raised over $310.7 million cash through entitlement offer. Accordingly, Seven west decreased its net debt by 36.7% or $425.6 million, while the debt leverage ratio reduced to 1.8x EBITDA, as compared to 2.5x EBITDA during the earlier fiscal year. On the other hand, Seven West Media stock delivered a negative year to date returns of 45.75% (as at November 17, 2015) partly impacted by declining overall FTA revenues and the group’s poor performance. However, Seven West now estimates a better outlook driven by its newspapers, magazines and digital business. The group also approved on-market buy-back of shares worth over $75 million for the coming twelve months. SWM’s focus on live-streaming, performance from Yahoo7 and digital businesses of The West Australian and Pacific Magazines might support its revenues to an extent. Other drivers may be the licence fee cuts and digital monetization. The firm has an attractive dividend yield. We reiterate our “BUY” recommendation on the stock at the current price of $0.715

SWM Daily Chart (Source: Thomson Reuters)

G8 Education Ltd

.png)

GEM Dividend Details

Ongoing strengthening of the network via acquisitions: G8 Education Ltd (ASX: GEM) recently acquired over 13 premium childcare and education centers from several vendors for a total purchase price of $29.7 million (without transaction costs). The group reported that the purchase price is 4.1 times estimated EBIT in the 12 months after settlement. Post the acquisition, G8 Education’s network number of places would increase by 1,000 while the overall number of places in the firm’s Australian portfolio would be over 36,125 per day. Meanwhile, the group is also improving its organic growth and accordingly delivered solid performance with a 5.6% yoy revenue growth (for its 229 centers-Like for Like growth) during the first half of fiscal 2015, while its underlying EPS soared 60% yoy on a year over year basis during the same period, indicating its capabilities of deriving synergies through acquisitions. The company is also about to conduct a tender process to appoint a new auditor.

.png)

Like for like center EBIT growth for acquisitions by year (Source: Company Reports)

Stock Performance: G8 Education’s offer to Affinity which was declined by the latter and the takeover panel ordering GEM to sell the affinity shares acquired from taxonomy in excess of 20% of the total voting power in Affinity with the issuance of withdrawal rights to Affinity shareholders who accepted GEM’s bid, led to a plunge in the stock by over 13.85% (as of November 17, 2015) during this year to date. This was also partly impacted by the investor’s concerns on its heavy dependence on acquisitions for growth along with the Affinity takeover battle. On the other hand, over $3.5 billion worth of government’s federal budget was allotted to childcare, which might benefit GEM’s centers and subsequently drive the group’s price per child revenue, if more parents start working. GEM also reported a decent organic growth and has a track record of deriving decent synergies via its acquisitions. The group also has an outstanding dividend yield of over 6.5%. The stock rallied over 22.74% in the last four weeks (as of November 17, 2015) and we reiterate our “BUY” recommendation on the stock at the current price of $3.67

.png)

GEM Daily Chart (Source: Thomson Reuters)

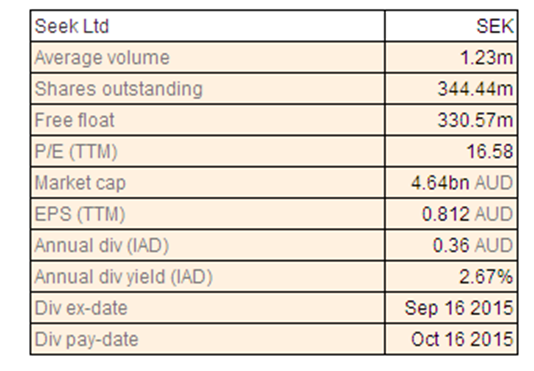

SEEK Ltd

SEK Dividend Details

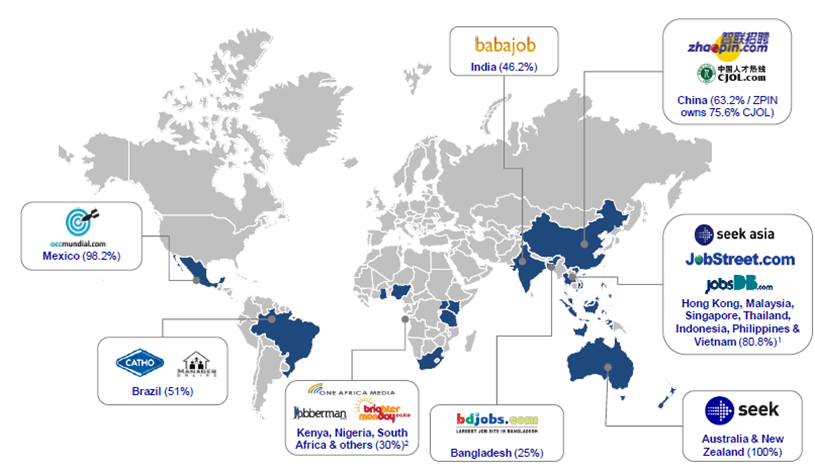

Boosting capital position by Offloading non-core business stake: SEEK Limited (ASX: SEK) recently reported that it would be offloading its 100% stake in its IDP Education (IDP), a testing and student placement business for over $330 million or US$233 million. IDP Education is a 50-50 joint venture between SEEK and a group representing Australian universities, and Seek reported that it arrived at this decision in view of the solid demand for IPO of IDP Education post the marketing phase. Moreover IDP’s EBITDA rose by 13% yoy to $52 million during fiscal year of 2015, with the group’s net profit after tax share from IDP accounting over $16 million. With this move, SEEK would be enhancing its value. Moreover, the group also delivered a revenue increase by 20% yoy to $858.4 million, driven by enhanced Australia and New Zealand online employment businesses, Premium Talent Search promotion, integration of JobsDB and JobStreet to Zhaopin in China. EBITDA delivered a 15% yoy increase to $348.9 million, while NPAT surged 6% yoy to $189.8 million during the year.

SEEK’s international presence (Source: Company Reports)

Attractive valuation: The group is a leading player in Australia, with 32% of placements and a lead of 10x higher as compared to its nearest competitor. The total visits in Australia witnessed a CAGR increase of 22% to 35+million in FY15, from FY12. Moreover, mobile visits performed even better showing a CAGR of 47% during FY12 to FY15. SEK extended its market leadership in Brazil and Mexico by making acquisitions, which are delivering solid financial results. On the other hand, the group issued a conservative FY16 guidance which disappointed the investors, leading to stock fall of over 2.21% in last three months. But, SEEK recovered over 6.35% (as of November 17, 2015) in the last four weeks and the recent IDP stake offloading announcement would further boost the stock in the coming months. We remain bullish on the stock and reiterate our “BUY” recommendation at current price of $13.78

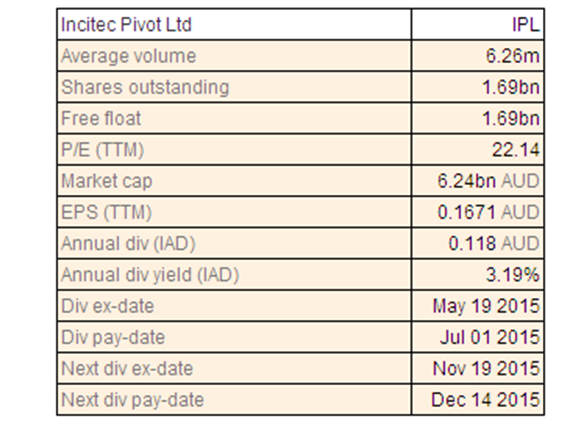

Incitec Pivot Ltd

IPL Dividend Details

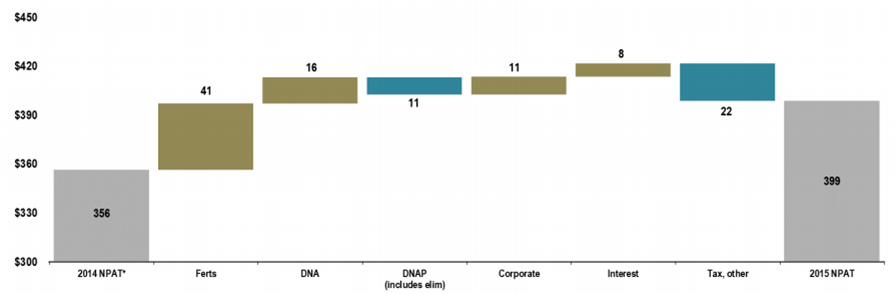

Enhanced performance despite challenging conditions: Incitec Pivot Ltd (ASX: IPL) reported a 12% yoy NPAT increase to $398.6 million while EBIT rose by 11% yoy to $576.5 million during fiscal year of 2015 as the group’s strategy efforts paid off. Moreover, IPL’s Moranbah ammonium nitrate plant also contributed to the overall performance, while its long term contracts with clients for the output offset the current tough resources and agricultural industries impact. The group’s Louisiana ammonia project is 90% finished and would start its first production in the third quarter of fiscal year of 2016. Louisiana ammonia project has the first mover advantage which would leverage the shale gas demand in the USA. IPL reported a 41% rise in operating cash flow to $756.2 million during the period.

NPAT Waterfall (Source: Company Reports)

As per the segment highlights, Dyno Nobel Americas (DNA) EBIT rose by 10% yoy driven by falling Australian dollar. The Fertilizers EBIT rose 22% yoy boosted by solid manufacturing performance at Phosphate Hill which produced 1.043 million tonnes of ammonium phosphates. IPL also entered into a long term gas supply agreement (10-year) with Power and Water Corporation for its Phosphate Hill plant as part of the North East Gas Interconnector pipeline project. The group derived over EBIT benefits of $41 million as its business excellence efforts drove its productivity gains > $100 million during the period. Meanwhile, the shares of IPL surged over 15.13% (as of November 17, 2015) in the last three months. We give a “BUY” recommendation on the stock at the current prices of $3.82

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.