-

Unexpected resignation from CEO: Greencross Limited (ASX: GXL) shares plunged more than 16.6% over the last five days as the group’s Chief Executive Officer (CEO), Jeffrey David reported that he is stepping down from the CEO role with immediate effect. This news came in as a surprise as there was not even a slight hint on the possible management changes during the 2015 fiscal year results reported on 11 August. Martin Nicholas, the group’s present Chief Financial Officer (CFO) will be substituted for CEO of Greencross.

-

Ongoing business growth: Greencross was able to increase the size of its business by 6x from FY13 to FY15, driven by the Mammoth merger and City Farmers acquisition. The group has fully integrated City Farmers during FY15, wherein 26 stores at Western Australia maintained the City Farmers brand while 16 east coast stores were rebranded as Petbarn. The group’s total store count rose by 65 stores to 200 during the 2015 fiscal year, while the clinics increased by 21 to 132. Greencross added five more stores in FY16 year to date totaling the store count to 205 (first six weeks of the year). Total clinic numbers reached 136 in YTD of FY16. Meanwhile, Greencross overall outlets reached 332 by 2015 fiscal year end. And 341 by YTD of FY16. GXL was also able to enhance its online business by 80%, although it comprises only 1% of the group’s Retail sales. Meanwhile, Greencross increased its retail loyalty membership by 25% yoy to more than 2.9 million members while the Healthy Pets Plus membership surged 43% yoy to >43,000 members during FY15.

.png)

Multiplying business since FY13 (Source: Company Reports)

-

Outstanding Financial Performance: Greencross reported a 45% yoy revenue increase to $644 million for the fiscal year of 2015, driven by the City Farmers acquisition. The group’s vet business and Retail business surged 28% yoy and 52% yoy respectively during the year. Gross margin rose by 50 bps to 55.3%, against pcp driven by improvements at City Farmers stores. As a result, Greencross underlying NPAT climbed 77% yoy to $38.2 million in FY15, while the underlying EPS reached 34.3 cents per share in FY15, as compared to 24 cents per share in pcp . Accordingly, Greencross improved its annual dividend payout by 36% to 17.0 cents, from 12.5 cents in FY14 to sustain its payout ratio of about 50%.

-

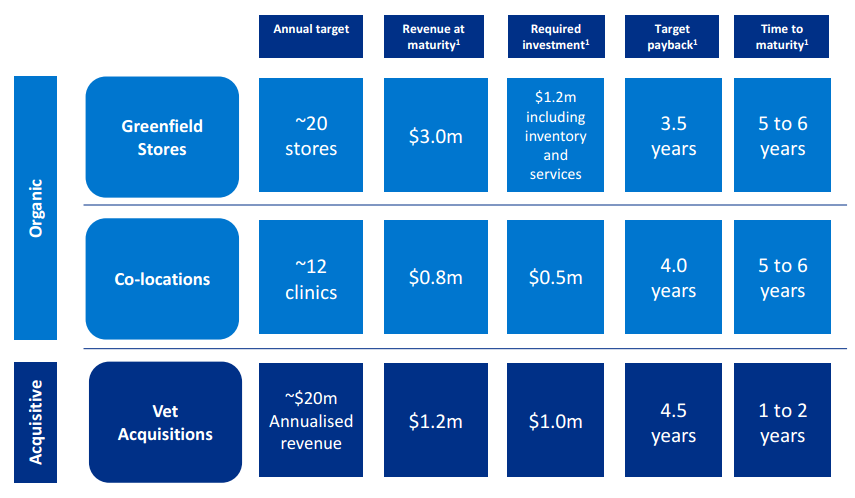

Huge addressable market opportunity: Greencross’ has a huge target pet sector market in Australia worth over $9 billion. Moreover, this market is forecasted to grow at around 4% per annum to reach $11 billion by 2020. Greencross customers spend 5x more at GXL stores which offers retail, vet and grooming services as compared to customers who shop only at its retail stores and 2x spend by customers who use only Greencross vet. Accordingly, the firm has three major growth platforms, with these areas promising attractive returns and significant potential, helping the group to achieve its target to boost the market share from 8% (with 332 outlets) to 20%.

Greencross target pipeline (Source: Company Reports)

-

Year to date FY16 performance: Greencross witnessed a revenue growth of 19% for the first five weeks of this 2016 fiscal year. LFL sales improved by 6.2% with Veterinary rising 5.5.%, Australian retail by 5.0% as well as NZ retail growing by 9.3%. Management said that the group is on track to achieve an organic led growth for the 2016 fiscal year by opening 20 new stores, wherein five stores were already opened in YTD of FY2016. Moreover the firm intends to make Vet acquisitions which would represent $20 million of the annualized revenues of FY16, wherein two vet acquisitions were already finished during YTD FY2016.

GXL Daily Chart (Source - Thomson Reuters)

-

Stock Performance: Greencross stock plunged over 26.5% during this year to date, impacted by investors’ concerns of the firm’s dependence on acquisitions to deliver its target potential. The recent news of CEO resignation also added to the pressure since past few days. On the other hand, investors should note that the CEO’s role is substituted by the equally talented executive, Martin Nicholas. The group is in line to achieve growth through co-locate stores. Moreover, Greencrossalso reported a like-for-like sales (LFL) rise of 6.2% in the YTD of 2016 fiscal year, addressing the investors’ concerns on its organic growth. We believe that investors have recently overreacted on management change news, and need to leverage the recent correction as an opportunity to enter the stock. Based on the foregoing, we recommend a “BUY” on GXL at the current price of $5.68.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.