Spotless Group

-

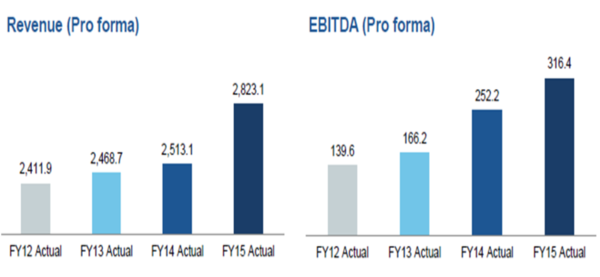

FY15 performance exceeded guidance: Spotless Group Holdings Ltd(ASX:SPO) statutory revenues rose 9.6% yoy to $2,872.9 million during the fiscal year of 2015, boosted by five acquisitions as well as organic growth. The statutory EBITDA surged 70.2% yoy to $316.4 million, while the pro forma EBITDA soared 12.3% yoy, as SPO’s cost savings efforts as well as efficiency programs from the last three years have been paid off. The adjusted NPAT surged 31.9% yoy to $150.2 million in FY15. SPO is well positioned to fund its future opportunities and has a low leverage with net debt to EBITDA of 1.8 times. Meanwhile, spotless Group declared an unfranked dividend of 5.5 cents. The group got further debt facilities of $200 million with extended debt maturity profile.

Growing revenue and EBITDA base over the last three years (Source: Company Reports)

-

Building revenue streams through Client Wins: Spotless Group has been building a long term client base and has renewals of over $1,300 million per annum and approximately $350 million per annum of new contract wins. Some of the new wins include Facilities management contracts for the Melbourne Airport Terminal, Australian Department of Defense, the University of Western Australia, New Zealand Defense Force, Catering contracts for Newcastle Airport, Emirates lounges nationally and Jetstar at Brisbane. The group’s contracts have a combined average tenor of ~27 years, offering a long-term security to SPO’s revenue stream. Spotless’ PPP revenues reached over $112 million during the fiscal year of 2015

-

-

Recent Acquisition to boost Service offerings: Spotless Group finished Aladdin Laundry, International Linen Service and TechGuard Security acquisitions in the first half of fiscal 2015. The group also reported that it would be acquiring Utility Services Group, Australia’s leading provider of retail meter reading and installation services, which has annual revenues of $200 million at the time of acquisition. SPO is also acquiring AE Smith, Australia’s leading air-conditioning and mechanical services provider, which has $100 million of annual service and maintenance revenues.

-

Positive Outlook: The shares of Spotless Group have touched a high of $2.52 during April this year, but have declined by 20% over the last three months on concerns over its funding abilities for its acquisitions. However, the recent full year FY15 results have been very positive and Spotless Group said that its fiscal year of 2016 results might be better than FY15 results, based on the market conditions. The group estimates an incremental annualized revenue of over $130 million from PPP projects which would achieve a full operational phase during FY16 and FY17. Therefore the stock surged over 6% yesterday (on August 25th) and we believe this upbeat on the stock would continue. Based on the foregoing, we recommend a “BUY” on SPO at current price of $1.88.

Lend Lease Group

-

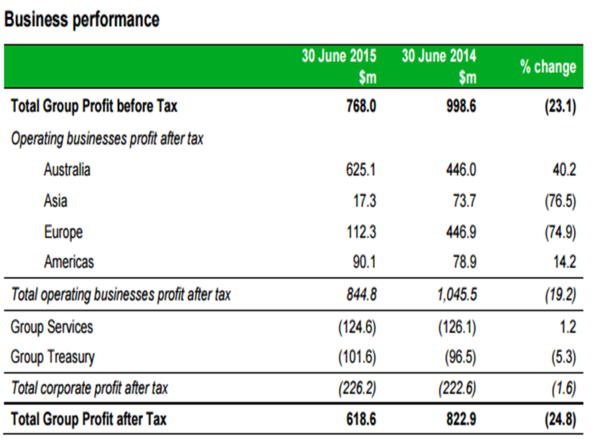

Fiscal 2015 results: Lend Lease Group (ASX: LLC) Profit after tax fell to $618.6 million for the year ended on June 2015, against $822.9 million in pcp (PAT included sale contribution from the Bluewater Shopping Centre asset in the UK for $485.0 million).Consequently, earnings per stapled security reduced to 106.8 cents, as compared to 142.7 cents per share. Meanwhile, LLC reported a franked dividend to 25%, with annual payout ratio of 51%. On the other hand, LLC’s pre sold residential apartments and communities revenues surged 109% on a year over year basis to $5.2 billion, and has development pipeline end value of $44.9 billion, which is 19% higher as compared to previous year. Construction backlog revenue surged 7% yoy to $17.3 billion, while the Funds under Management soared 31% yoy to $21.3 billion. LLC raised a capital of over $2.1 billion from third party. The group is sitting on a cash of $2.2 billion.

FY15 performance highlights (Source: Company Reports)

-

Building business from International Markets: LLC is building international projects in Asia and America, with the pipeline achieving a record level of over $45 billion, wherein over 70% represent the urbanization projects. On the domestic front, Barangaroo South project in Sydney introduced further residents to the zone, took leasing commitments across all three commercial towers to 66%; sold Tower 1 and build a new circa of $2 billion fund to own that tower; made an agreement with Crown Resorts to bring a world class resort and hotel. Meanwhile, global backlog revenues witnessed an increase of 7% yoy to $17.3 billion during the year while the profit rose 10% yoy, despite a lower contribution from the Australian region. Two new investment vehicles, Lend Lease One International Towers Sydney Trust and the Paya Lebar Central investment mandate were formed in the year, due to which the FUM balance rose 31% yoy to more than $21 billion

-

-

Outlook: LLC stock has delivered a negative year to date returns of around 12.6% impacted by challenging market conditions. However, the stock rose 4.5% yesterday (Aug 25) driven by the positive outlook. LLC’s solid pre sold residential revenues would drive its profit as well as cash from next year. LLC developed a diverse project base over the years. The group’s pre sold residential revenues of $5.2 billion are estimated to generate earnings from FY18. International markets would also support the stock, as it already has a circa of $8 billion of new major urban regeneration projects in Asia and the Americas. Having a relatively cheaper P/E of 9.5x, and strong return on equity of 18%, we give a “BUY” recommendation on SPO at the current price of $13.19

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.