Domino's Pizza Enterprises Ltd

.png)

DMP Details

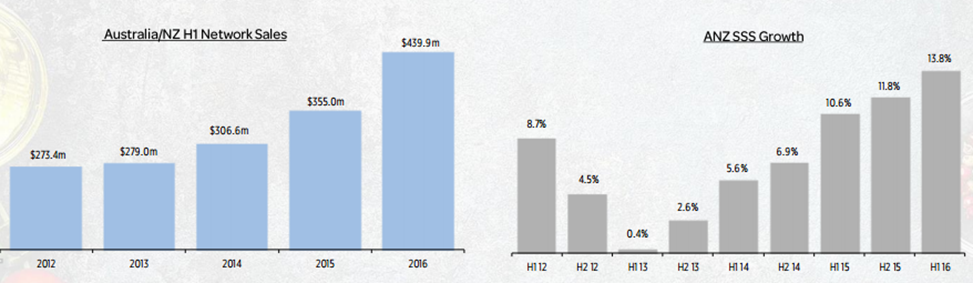

Facing allegations on its GPS Driver Tracker Technology: Domino's Pizza Enterprises Ltd. (ASX: DMP) recently clarified investors that their dispute with Precision Tracking, an IT firm related to GPS Driver Tracker Technology were irrelevant. On the other side, the group’s stock surged over 65.01% (as of April 29, 2016) in the last one year driven by its outstanding performance across its segments. DMP delivered a Net Profit after Tax rise by 56.7% yoy to $45.6 million supported by same stores performance which increased by 10.3% for the first half of 2016. There has been a 41.1% increase in interim dividend to 34.7 cents. Accordingly, the firm’s underlying revenues surged by 29.6% to $445.3 million during the period, while underlying EBITDA rallied by 44.9% to $87 million against the pcp.

Consistently increasing network sales (Source: Company Reports)

Meanwhile, the group also finished the acquisition of the 212 store Joey’s Pizza chain in Germany. With this move DMP would add over 210 franchised stores to its brand. However, the recent rally in the stock placed DMP at very high levels with the stock is trading at an unreasonable P/E. Therefore, we rate the stock “Expensive” at the current price of $62.80

DMP Daily Chart (Source: Thomson Reuters)

Retail Food Group Limited

.png)

RFG Details

Delivered outstanding performance: Retail Food Group Limited (ASX: RFG) reported a strong performance for the first half of 2016, with revenues surging by 90.2% yoy to $148.3 million while reported EBITDA rose by 42.7% yoy to $49.2 million. The group’s underlying NPAT increased by 27.1% yoy to $32.1 million in first half of 2016. New Outlets Commissioning rose by 67 to 142 while International Territories increased by 5 to 63. Recently, RFG reported that Andre Nell would be replacing A J (Tony) Alford as Managing Director starting from July 2016. The group got six new Master Franchise Agreements during the first half of 2016 leading to a total of 63 international licensed territories.

.png)

Proven business model delivering positive shareholder returns (Source: Company Reports)

The coffee & allied beverage throughput reached 3.04m kg during the first half of 2016 as compared to the fiscal year of 2015 annualized throughput of 5.92m kg. The group has also confirmed the purchase of properties in Ashmore on the Gold Coast for its new global head office.

Meanwhile, RFG stock surged by 21.68% in the last three months (as of April 29, 2016) and we believe this strong performance would continue in the stock given its aggressive expansion efforts. Based on the foregoing, we give a “Hold” on this dividend yield stock at the current price of $5.47

.PNG)

RFG Daily Chart (Source: Thomson Reuters)

Collins Foods Ltd

.png)

CKF Details

Improving working capital: Collins Foods Ltd (ASX: CKF) recently reported that they are refinancing their present syndicated debt facilities of $165 million with expansion of $65 million (fully drawn). The group also extended its working capital facility of $15 million to more terms. Meanwhile, the group’s revenues rose by 5.1% to $269.7 million for the first half of 2016 while KFC same store sales increased by 5.2% against the prior corresponding period (pcp).

On the other hand, the group’s Sizzler Australia’s same store sales fell by 12% during the first half of 2016. This poor same store performance coupled with tough market conditions in Australia drove the stock lower by 22.99% in the last three months (as of April 29, 2016). Despite this decrease, we believe the stock is “Expensive” at the current levels of $4.04

CKF Daily Chart (Source: Thomson Reuters)

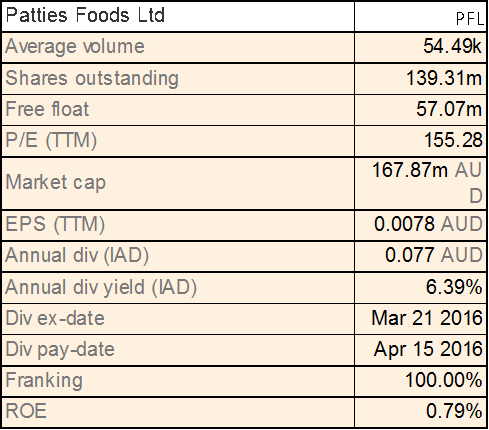

Patties Foods Limited

PFL Details

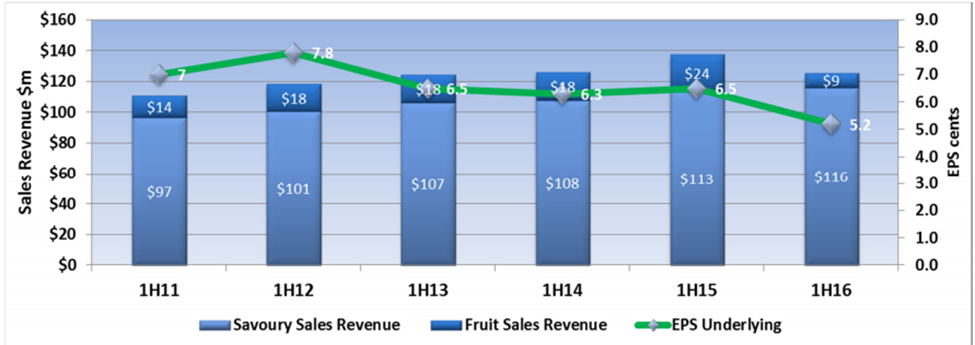

Top line pressure: Patties Foods Limited (ASX: PFL) reported weak revenues for the first half of 2016 which fell by 8.6% to $126.2 million on the back of decrease in Frozen Fruit sales and margins as compared to the first half of 2015. But, the group’s core Bakery revenues performance continued to deliver a decent performance during the period which rose by 2.8% during the period. The underlying EBIT (excluding Fruit) rose by 7.2% to $13.1 million. However, its In-Home channel sales fell by 16%, due to decrease in Frozen Fruit revenues coupled with exit of two unprofitable Private Label contracts. Meanwhile, the group’s FOUR’N TWENTY, Patties, Herbert Adams and Nanna’s reported a decent performance across their divisions and target markets. Out of Home channel sales improved by 6.9% on a yoy basis while core savory business rose by 9.6% on a yoy basis. FOUR’N TWENTY brand enhanced by 10.6% on track with its business channel growth strategy.

Weakness in 1H16 performance (Source: Company Reports)

The stock has risen 5.70% in the last five days (as of April 29, 2016). Moreover, the stock is trading at a very high P/E despite having a strong dividend yield. As a result, we give an “Expensive” recommendation on the stock at the current price of $1.22

PFL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2016 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.