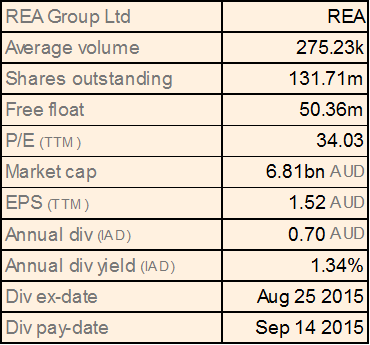

REA Group Ltd

REA Dividend Details

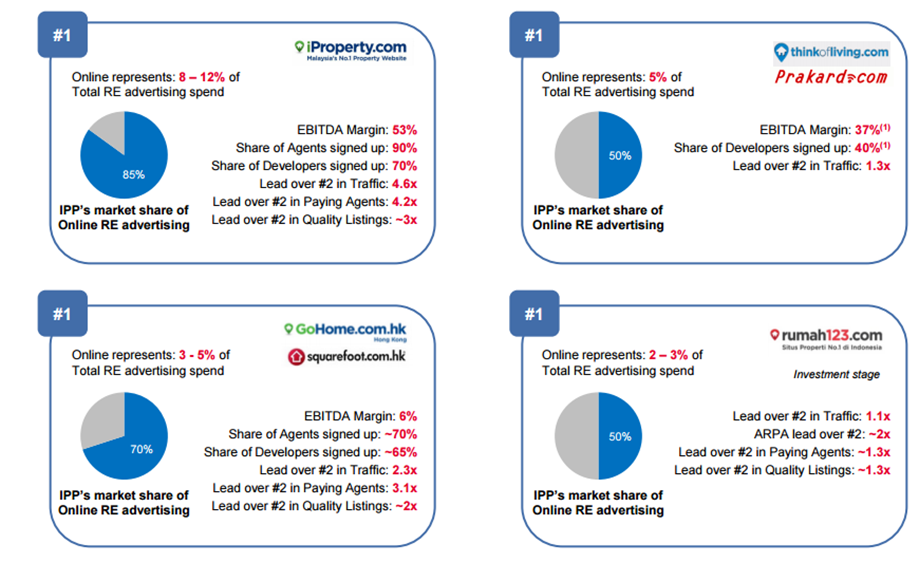

Expanding Asia’s penetration: REA Group Ltd (ASX: REA) acquired iProperty Group, which is a major property portal at Malaysia, Hong Kong, Thailand and Indonesia, to boost its presence in booming South East Asia market. IPP delivered a solid third quarter and reported a cash collections rise by 67% to $8.6 million as compared to the corresponding quarter in 2014. Meanwhile, REA also generated outstanding revenue growth of 21% on a year over year basis to $146 million for the September quarter of 2015 while reported an EBITDA increase of 30% from core operations to $82 million during the period.

Strong Return to Shareholders (Source: Company Reports)

The group’s Australia site, realestate.com.au continued to be a dominant player across all devices as well as developed highly engaged property audience during the first quarter of 2016. The site’s average monthly visits during the first quarter of 2016 improved by 33% year over year to 42.7 million while the consumers spent 257.3 million minutes a month on realestate.com.au’s main and mobile site. The site continued to outpace the average monthly time of the number two portal site by 5.5 times.

iProperty solid market penetration would benefit REA (Source: Company Reports)

REA’s international markets growth momentum is also strong with the realtor.com at US being the number two site.

This solid business performance by REA across its domestic as well as international markets drove its shares by over 34.38% in the last six months and over 5.47% in the last four weeks alone (as of December 03, 2015). We remain bullish on the stock and reiterate our “BUY” recommendation at the current price of $51.34

.png)

REA Daily Chart (Source: Thomson Reuters)

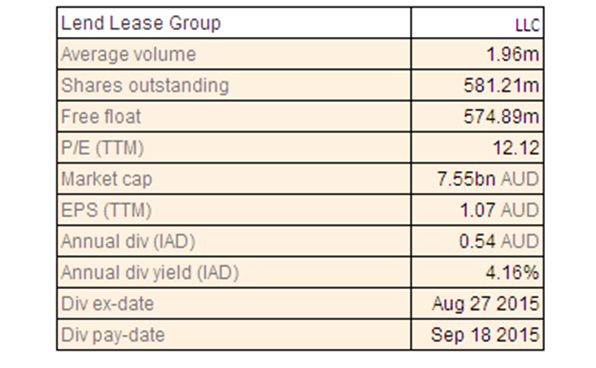

Lend Lease Group

LLC Dividend Details

Building strong development pipeline driven by urban and retirement living projects:Lend Lease Group (ASX: LLC) shares fell over 18.29 in the last six months (as of December 03, 2015) as the group reported a profit after tax decrease to $619 million during fiscal year of 2015 as compared to $823 million in FY14. On the other hand, LLC built a solid pipeline and improved pre sold residential revenue by 109% year on year (yoy) in FY15 in Australia as well as UK. LLC enhanced its urbanization projects to over $33 billion in FY15 as compared to $16 billion in FY11. The group’s retirement living units increased to 14,193 in FY15 from 12,417 in FY13 while development end value reached $44.9 billion during 2015, against $34.7 billion in 2011. LLC enhanced its residential development business by 24% yoy to 4,262 during fiscal year of 2015, as compared to the 2014 fiscal year. Lend Lease major urban regeneration projects reached over $8 billion driven by the new developments in Singapore, Malaysia and the United States. LLC invested over $2.2 billion of production capital into its development pipeline leading to over 25 major residential apartment buildings and five commercial buildings. The group has a residential pre-sales book of over $5.2 billion for the coming three to four years, with over 45% likely to be settled before June 2017. Around 20% of the apartment pre-sales were from mainland China buyers, from which 30% of them would be settled before June 2017.

LLC’s major metrics (Source: Company Reports)

Management reported that the group is the preferred bidder for over $7 billion worth of new work which is not included in the backlog revenue. Meanwhile, the recent correction in the stock placed LLC at attractive valuations with a P/E of about 12x and dividend yield of 4.2%. We maintain our “BUY” recommendation on the stock at the current price of $12.88

LLC Daily Chart (Source: Thomson Reuters)

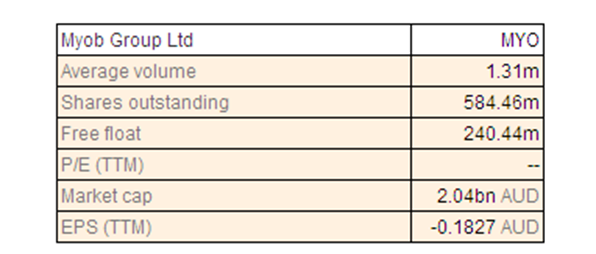

Myob Group Ltd

MYO Details

Focusing on cloud opportunities: Myob Group Ltd (ASX: MYO) shares corrected over 10.54% (as of November 17, 2015) since its listing on ASX on May 4

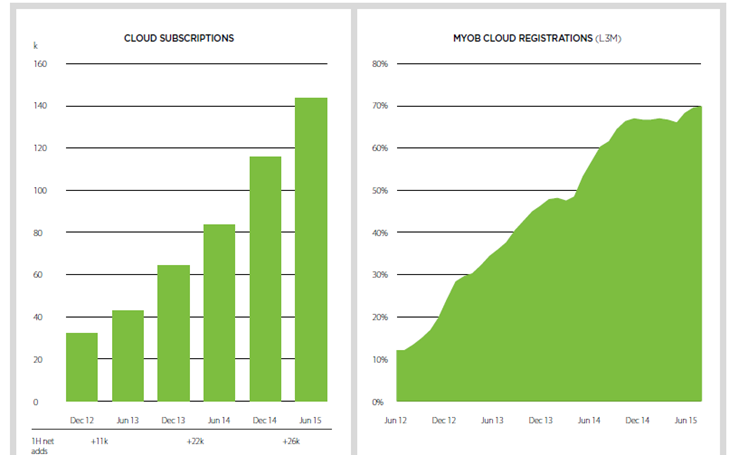

th on investor’s concerns of its outlook in the current challenging market conditions. On the other hand, Myob Group reported a revenue increase of 8% yoy to $161 million, while pro forma EBITDA growth was of the order of 14% yoy to $72 million in the first half of 2015. Around 94% of first half of 2015 revenues were recurring driven by 10% growth in paying user base to 528,000. MYO achieved a record cloud solutions adoption, resulting in SME cloud subscriptions to 142,000 and 150,000 during June 2015 and early August 2015, respectively. Myob Group is making efforts to shift to a cloud accounting solutions provider for micro till mid-tier clients from being software provider. Accordingly, the group introduced MYOB Advanced, a cloud-based ERP solution for mid-sized businesses due to which the group recorded 18% of new client registrations in its enterprise solutions (since its launch in Jan till the first half ending period). The group’s PaySuper is MYOB compliant SuperStream service, and even offers benefits by decreasing the time for small business clients.

SME Cloud Subscriptions and registrations growth as of first half (Source: Company Reports)

MYOB Group acquired Information Management Services Limited (IMS), a New Zealand-based payroll provider to over 10,000 small and medium businesses for NZ$9.7 million to strengthen its core business as well as leverage the attractive online growth potential of the Payroll market in New Zealand. MYO stock seems to have the potential for returns and we therefore maintain our “BUY” recommendation on the stock at the current price of $3.30

MYO Daily Chart (Source: Thomson Reuters)

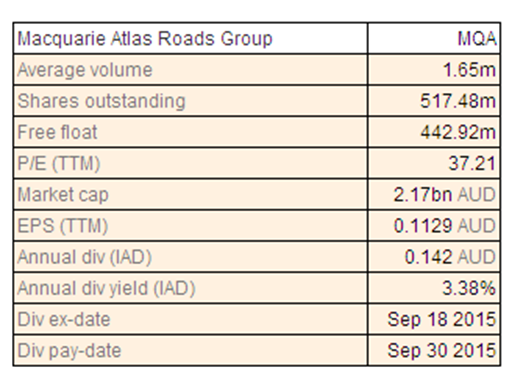

Macquarie Atlas Roads Group

MQA Dividend Details

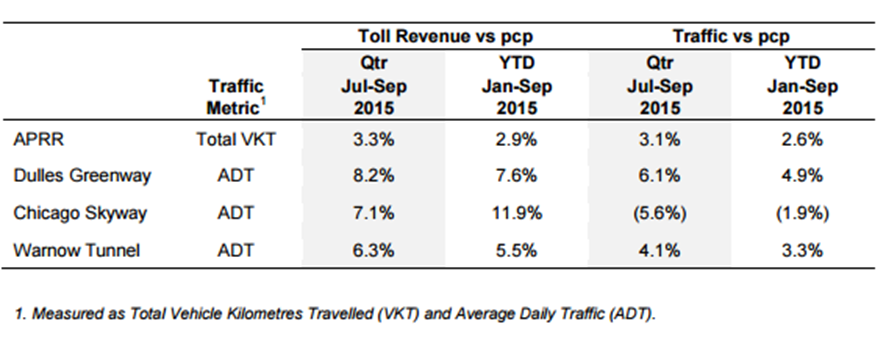

Improving traffic would boost performance further: Macquarie Atlas Roads Group (ASX: MQA) reported a better toll revenue and traffic statistics during the September quarter, wherein weighted average toll revenue rose by 3.8% yoy driven by rising traffic levels and revised toll schedules. Weighted average traffic for the period improved by 3.0% against the corresponding period of last year on the back of rising traffic volumes at APRR network as well as Dulles Greenway. Consequently, Dulles Greenway and Chicago Skyway toll revenue surged 8.2% and 7.1%, respectively, during the September quarter. Moreover, recently MQA entered into an agreement to sell 100% of Skyway Concession Company, the concession owner of the Chicago Skyway in Illinois for US$2,836 million.

September quarter performance (Source: Company Reports)

Accordingly, MQA’s shares surged over 29.48% in the last three months (as of December 03, 2015). We believe that the ongoing improving traffic would boost MQA performance further and accordingly we give a “BUY” recommendation on this 3.38% dividend yield stock at the current price of $4.20

MQA Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.