Computershare Limited

-

The statutory results for FY 2015 show a decline of 3.2% over the previous year in total revenues to $ 1.98 billion an increase of 1% in total expenses and a decline of 38.9% in statutory net profit (Post NCT) $ 153.6 million. EPS (Post NCT) was down 38.9% to 27.61 cents per share. The company uses management results along with other measures to assess business performance because the exclusion of certain items allows a better analysis and provides better measure of underlying operating performance. Non-cash management adjustments include the significant amortisation of intangible assets asset disposals and other one-off charges Cash Management adjustments include mainly the the expenditure relating to acquisitions and restructuring and will be discontinued when full integration has been completed. Accordingly, the management adjustments to the statutory results show total revenues of $ 1.97 billion and NPAT of $ 179.2 million.

-

Given the range of known headwinds when starting FY 2015, the company considers the operating performance to be sound and management EBITDA grew by 2.5% compared to the previous year in actual terms and 5.3% in constant currency terms. Management revenues was down 2.3% but up 1.4% in constant currency terms. The revenue benefits from the impact of acquisitions and disposals were partly offset by the headwinds.

-

Register maintenance revenues were down 2.8% in actual terms but up 1.4% in constant currency terms because of the benefits of recent acquisitions in Canada and the United States. Revenues from Corporate Actions declined to the lowest levels in many years because of reductions in cash rates in Canada and Australia and the majority of the USD deposit facility in FY 2014. Employee Plans revenue fell by 4.6% over the previous year and were also down 1.8% in constant currency terms and the segment was impacted by lower margins and income contribution and weaker transaction volumes.Business services reported overall revenue growth though there was an impact on Australian revenues though the company lost its largest client the aftermath of being acquired. UCIA benefited from the acquisition of HML and growth in voucher services revenue. The growth in class action administration was offset by the weaker revenues generated by bankruptcy administration. There was margin growth in US mortgage servicing offsetting the revenue losses from the sale of Highland Insurance in June 2014 and the loss of a substantial contract in sub-servicing. Stakeholder relationship management revenues declined significantly as a result of the sale of the Peppers Group. Revenues from Communication Services also fell and was further affected by currency translation because of the significant AUD component of this segment. Costs went down by 4.1% because of the strong USD. The Management effective tax rate was 26.1%.

-

The company has a number of strengths. It has a leading position in all its major markets for equity investor record keeping and employee stock plan administration because of its sustainable advantage in technology, the superiority of its quality and its operational efficiency and a global platform allowing seamless execution of cross border transactions. It is continuing to consolidate its position and to extract synergies from its acquisitions in its chosen areas of business. In general terms, over 70% of its revenues is recurring in nature, it has a long track record of substantial cash generation from operations and it has a strong balance sheet and prudent leverage with the average maturity of debt facilities of 3.8 years.

-

For the year ahead, the company expects business performance which will be broadly in line with FY 2015. However, it expects to see considerable headwinds in the area of earnings because of the currency translation impact of the strong USD and the lower yields on client balances. The company is also expecting some cost increases including the costs of investments in product development and efficiency increases. After considering all these factors, management EPS for FY 2016 is expected to be 7.5% lower than FY 2015. Assessment of the future outlook is based on the assumption that equity, foreign exchange and interest rate markets remain at current levels and corporate action activity will continue at FY 2015 levels.

-

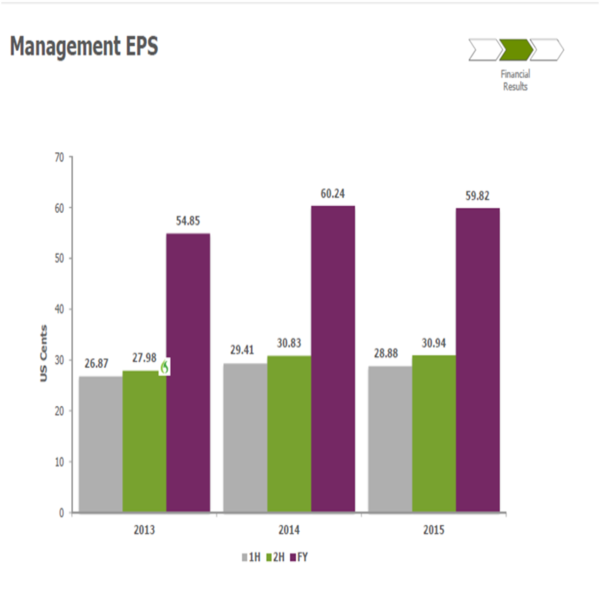

Sales revenue was down 2.3% to $ 1.96 billion and interest and other income was down 11.7% to $ 9.9 million making a total management revenue of $ 1.97 billion which is down 2.3% over the previous year. Accounting for operating costs of $ 1.42 billion and share of profits and losses from associates of $ 2.3 million, management EBITDA was down 2.5% compared to the previous year at $ 554.1 million. Statutory NPAT was down 38.9% at $ 153.6 million and management NPAT was down 0.7% at $ 332.7 million. Statutory EPS was down 38.9% at 27.61 cents per share and management EPS was down 0.7% at 59.82 cents per share.

Management EPS (Source: Company Reports)

Management EPS (Source: Company Reports)

-

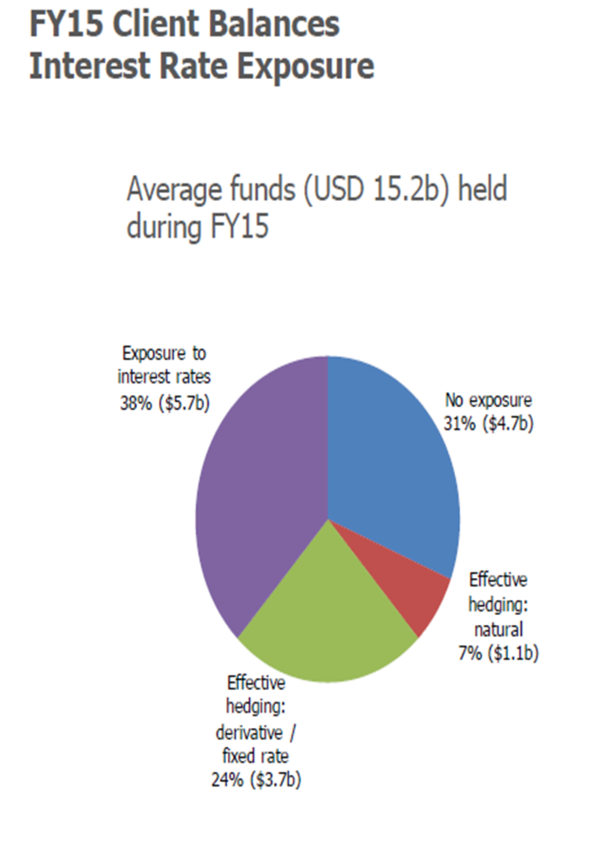

In respect of client balances interest rate exposure, the company had an average of $ 15.2 billion of client funds under management during FY 2015. For 31% of these funds, there was no exposure to interest rate movements as a result of not earning margin income or receiving a fixed spread. The remaining 69% were exposed to interest rate movements. For 24% of these funds, effective hedging by way of derivatives or fixed rate deposits were in place. 7% were naturally hedged against the company's own floating rate debt. The remaining 38% were exposed to interest rate movements.

Average Funds Held ( Source: Company Reports)

-

Group strategy and priorities and delivery - Strategy remains as before. The company is seeking acquisitions and other growth opportunities where where value can be added and returns enhanced for shareholders. Front office skills will be improved for the protection and growth of revenues. Operations quality and efficiency will be driven through technology and benchmarking. Focus will be prioritised by protecting profitability in mature businesses, investing in growth opportunities with good potential, using a disciplined approach to evaluate new business opportunities and investments and simplifying the business where possible. The business portfolio was refined with the HML acquisition opening up new possibilities in the UK mortgage servicing business and the Valiant acquisition strengthening the Canadian market position. Divestitures of non-strategic businesses were also completed.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.