.png)

Stocks’ Details

Navigator Global Investments Limited

Enhanced AUM Performance:Navigator Global Investments Limited (ASX: NGI) is an asset management company that provides hedge fund services to retail, wholesale and institutional investors across the globe. Recently, the company announced that IOOF Holdings Limited, a substantial holder of Navigator Global Investments Limited’s changed its holding from 7.970% of interest to 10.380%. Group’s US subsidiary, Lighthouse Investment Partners, has also acquired Mesirow Financial’s Multi-Manager Hedge Fund Business to provide a unique offering to its clients.

.png)

Asset Under Management (AUM) Performance (Source: Company Reports)

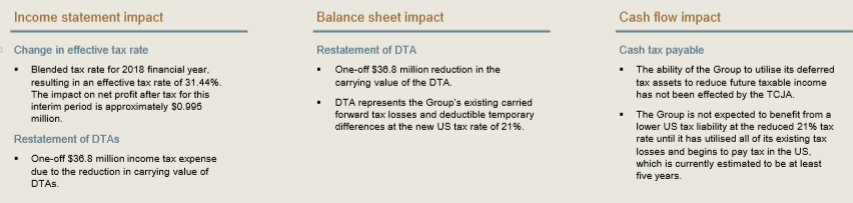

On the other hand, group’s AUM has grown by about $990 Mn over the half year with 66% of growth due to net inflows and the rest 34% of growth due to positive investment performance. EBITDA grew by 14% to $16.1 Mn in 1HFY18 from $14.1 Mn in 1HFY17. During the period, operating expenses increased by $3 Mn due to high employee cost and occupancy cost. Net Loss after tax stood at $26.7 Mn in 1HF18 from profit after tax at $8.4 Mn in 1HFY17 due to one-off impact and non-cash income tax expenses adjustment. The Group continues to execute its strategy to retain and to grow AUM through providing high level of quality services to clients and proactively follow the approach to ensure meeting client’s investment needs. The group has also highlighted the impacts from the December 2017 US tax reform. The group has no debt (hence capital light) and has more than A$55m of cash and investments on balance sheet. While slight impact from US tax reform is expected, the business has the potential to generate revenue and cash at the back of organic growth.

Impact from US Tax Reform (Source: Company Reports)

Meanwhile, the stock has risen 36.06% in last six months but slipped by 2.5% on March 23, 2018 with the majority of stocks in red owing to the market meltdown. Looking at the overall picture and potential to grow further, we recommend a “Speculative Buy” on the stock at the current market price of $3.57

Hub24 Limited

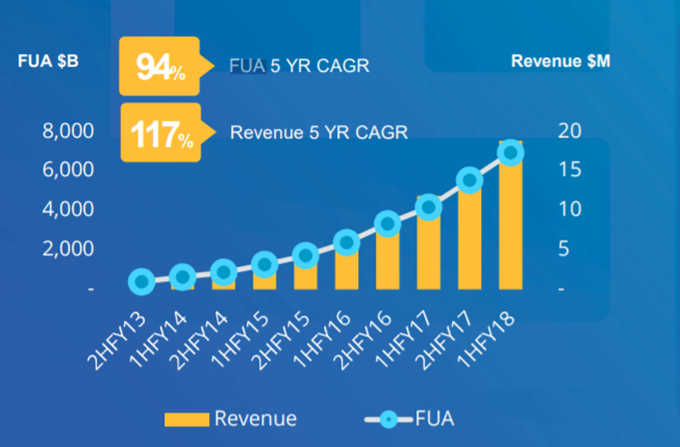

Well Positioned for Growth: Slipping by 1.4% on March 23, 2018, HUB has been trading at high levels as seen in the last six months. The group’s revenue during 1HFY18 was recorded at $41.01 Mn against $27.52 Mn in 1HFY17, marking a solid year on year (YoY) growth of 49%. The sales spiked up due to increased inflow from broader client base during 1HFY18. Underlying EBITDA grew by 185% to $4.9 Mn in the first half of the year from $1.7 Mn in 1HFY17. Underlying NPAT grew to $2.1 Mn in 1HFY18 from $1.2 Mn in 1HFY17. Fund under Administration (FUA) increased by 66% to 6.9 bn in 1HFY18 from $4.1 bn 1HFY17. Further, HUB maintained its position as a market leader in managed accounts which is best in terms of mobile access and best navigation and user interface. In 1HFY18, HUB increased its investment in technology development to maximise opportunities on the back of key acquisitions and favourable trends in the financial service industry. Momentum is continuing into 2HFY18 with solid net inflows to date and continued conversion of HUB’s growing opportunity pipeline. The management expects that the business will continue to invest for expanding market opportunities and to leverage the changing market dynamics to create superior client and advisor solutions.Looking at trading levels and on-going potential, wegive a “Hold” recommendation at the current price of $9.95

Revenue and FUA Highlight (Source: Company Reports)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.