.png)

Stocks’ Details

LiveTiles Limited

LiveTiles to Acquire CYCL:LiveTiles Limited (ASX: LVT) is a global software company, which is engaged in the development and sale of business software in Australia and other countries. The market capitalisation of the company stood at ~$245.34 million as on 28th November 2019. LiveTiles Limited is going to widen its global leadership position in the intranet software market by acquiring CYCL AG, a leading intelligent intranet software business.

It will be a complementary technology to LiveTiles’ intelligent workplace offering. The deal comprises of an upfront purchase price of CHF12.9 million ($19.0 million) and two-year earn-outs of up to CHF9.0 million ($13.2 million), and the completion is expected by 2nd December 2019.

.png)

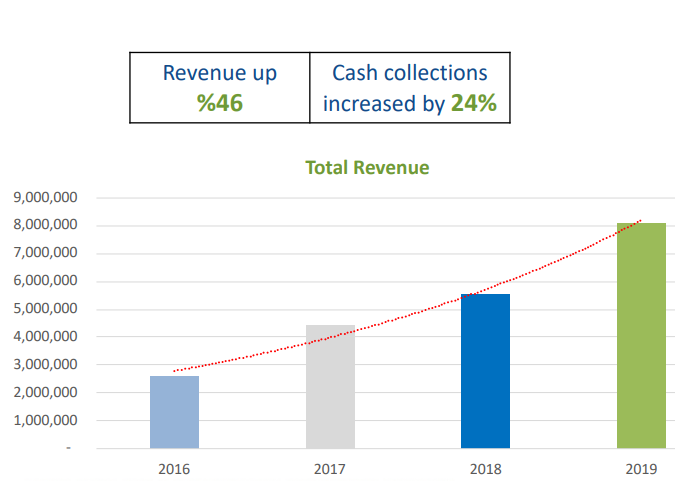

Combined operating metrics (Source: Company Reports)

Outlook for FY20: With the continued investment into products, partners and sales and marketing channels, the company expects to deliver another year of strong customer and revenue growth in FY20. In the last 12 months, the company’s ARR grew by 131%, and now its objective is to organically grow ARR to at least $100 million by 30th June 2021.

Stock Recommendation: As per ASX, the stock is trading below the average of 52-week high and low and has corrected 36.17% in the last six months. The company has reported an outstanding CAGR growth of 197.80% in its revenue in a time period of the last five years, i.e., from FY15 to FY19; thus, it can be said that company has decent capabilities to generate revenues, which might support its long-term growth prospects. Therefore, considering its current trading levels, revenue growth and favourable outlook, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.295 per share, down by 1.667% as on 28th November 2019.

Oliver’s Real Food Limited

Commonwealth Bank of Australia Approves Rollover Facility:Oliver’s Real Food Limited (ASX: OLI) is engaged in the management of Quick Service Restaurants (QSR) in Australia under the branding of “Oliver’s Real Food”. The market capitalisation of the company stood at ~$9.53 million as on 28th November 2019. The company has announced that CBA has confirmed that it will renew its existing $1 million facility with Oliver’s (without covenants) for a period of 18 months to 21st July 2021. The company has also announced that it has reported EBITDA of $0.162 million for the month of October, which represents the beginning of the 3rd quarter of continuous profitability.

Quarterly Cash Flow Report to 30th September 2019: The company had a strong first quarter as sales stood at $8.06 million and EBITDA stood at $0.466 million due to ongoing cost controls and good management.The company reported net cash outflow from operations of $221k. This includes a reduction of trade payables during the quarter of $250k as well as the payment of a rent adjustment related to the Wyong stores of $420k, which was accounted for in FY19 results, but was actually paid in July 2019.

.png)

Financial Performance (Source: Company Reports)

Stock Recommendation: In the past five years (FY15 to FY19), the company has registered a CAGR growth of 28.69% in the top-line. In FY19, its gross margin stood at 73.5%, which is above the industry median of 52.8%. Currently, the stock is trading at an EV/Sales ratio of 0.3x on a TTM basis, which is below the industry (speciality retailers) average of 2.0x on TTM basis. Thus, it can be said that stock is currently undervalued at the current juncture. The stock has also corrected 13.64% in the past three months. Based on current trading levels, reported EBITDA for October month and valuation metrics, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.038 per share.

DigitalX Limited

DigitalX Enters into An Agreement to Acquire BAM:DigitalX Limited (ASX: DCC) is a blockchain company that offers blockchain consulting and development services and asset management services focused on technology, including blockchain and emerging technologies. The market capitalisation of the company stood at $18.77 million as on 28th November 2019.

On 16th April 2019, the company announced that it has entered into an agreement to acquire Bullion Asset Management Services Pte Ltd (BAM), the investment management firm behind xbullion. As per the terms of the agreement, the company acquired shares through a share subscription, received advisory shares and entered into an agreement to acquire existing shares from an existing shareholder. The company has completed the transfer of the shares and has received 800,000 BAM shares, valued at $1 per share in exchange for 9,411,764 DigitalX shares with a deemed issue price of $0.085 each, for a value of AU$800,000.

DigitalX Launches Bitcoin Fund: The company has announced that it has established its second asset management product – the DigitalX Bitcoin Fund.It is available through a standard unlisted fund structure, which allows sophisticated investors like high net worth individuals and family offices a low-cost and familiar vehicle to gain exposure to this growing asset class.

The company’s motive in launching this fund is to grow the FUM within the fund at a rapid rate. Thiswill ensure that the fund achieves critical mass and the company will benefit from the receivable fees from the fund. The approximate value of the company’s investment into the fund will be ~$2.75 million, based on a price per bitcoin of AUD$12,800.

Outlook: With the continued interest from central banks and corporations in digital currency and positive commentary from regulators in China, the outlook of the sector is positive. After the news from Chinese President Xi Jingping to increase the rate of investment and development of blockchain technology in the country, the interest, activity and pricing in the market have strengthened.

.png)

DigitalX price vs. the bitcoin price since 3Q 2017 (Source: Company Reports)

Stock Recommendation: As per ASX, the stock price has corrected 13.89% and 59.74% in the past three months and six months, respectively. Currently, the stock is trading below the average of 52 weeks high and low. Its current ratio stood at 10.30x in FY19, which is above the industry median of 1.75x. Hence, considering its current trading levels and improvement in the blockchain technology market in the coming years, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.032 per share, up by 3.226% on 28th November 2019.

Medlab Clinical Limited

Depression Trial Update:Medlab Clinical Limited (ASX: MDC) is an Australian based medical life science company, developing therapeutic pathways for diagnosed chronic diseases. The market capitalisation of the company stood at $76.45 million as on 28th November 2019.

The company has provided an update of its depression trial, which is progressing ahead of expectations. It involves Medlab’s NRGBiotic™ from its Nutraceuticals range. The current results are implying that the trial will complete earlier than originally required. Depression treatment market is estimated to be of US$864 million in 2015 globally and is expected to reach US$1.2 billion by 2024. Overall, the global depression market is estimated to be US$15.6 billion, at a growth rate of 2.4% CAGR.

Cannabis October Update: The company has achieved record month for the number of cannabis bottles (NanaBis™ and NanaBidial™) with 846 bottles dispensed in October 2019 and achieved record month of revenue for cannabis in October 2019.Medlab currently has some 4,000 units of NanaBis™ in production to meet its short-term needs.

Outlook: For the next 12 months, the company will focus on growing its commercial position domestically and globally. The company will mainly focus on strengthening and expanding its Australian pharmacy position for nutraceuticals and taking the Medlab nutraceutical range to international markets.

Financial Highlights (Source: Company Reports)

Stock Recommendation: The company has reported a CAGR growth of 57.42% in revenues over the last five years (FY15 to FY19). Its debt to equity stood at 0.06x in FY19 as compared to the industry average of 0.19x. The stock is currently trading below the average of 52-week high and low. Based on its sales in October month, current trading levels and past growth in revenues, we recommend a “Speculative Buy” rating on the stock at the current market price of $0.365 per share, up by 2.817% on 28th November 2019.

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.