.png)

Stocks’ Details

The A2 Milk Company Limited

A Quick Look at FY19 Results: The A2 Milk Company Limited (ASX: A2M) is engaged into producing, marketing and selling the branded dairy and infant formula products in targeted global markets. The market capitalisation of the company stood at A$10.12 Bn as on 23 August 2019. Recently, the company updated the market with the revised securities trading policy which included the policies related to dealing in securities of the company and securities of other entities by the Directors and employees. The policy also informed about the consequences of insider trading.

Recently, the company released its results for financial year 2019, wherein it stated that A2M has increased its market share to 6.4% for infant nutrition in China. The company invested 13% of 2HFY19 revenue in marketing. The financial performance in FY19 reflected strong growth throughout core markets and product categories. A2M reported revenue amounting to NZ$ 1,304.5 Mn in FY19 as compared to NZ$ 922.7 Mn in FY18, reflecting a rise of 41%.

.png)

Group Revenue (Source: Company Reports)

What to Expect: The company expects continued growth in revenue throughout its key regions, supported by increasing brand and marketing investment in China and the US. A2M anticipates EBITDA as a percentage of sales for FY20 to be broadly consistent with EBITDA margin of 28.2% for 2HFY19. This primarily reflects continued investment in organisational capability in order to support future growth.

Stock Recommendation: The company enjoys a decent balance sheet with significant cash balance amounting to NZ$464.8 Mn. In August 2018, the company increased its investment in Synlait to 17.4%. The basic earnings per share of the company stood at 39.25 cents in FY19, reflecting a rise of 45.4%. Coming to the stock’s past price performance, it produced a return of 32.40% on YTD basis. Currently, the stock is trading marginally higher from the average of its 52-week trading range of $8.140 to $17.30. Stock is available at a price to earnings multiple of 36.70x as compared with the industry median of 13.1x. Hence, considering the above stated facts, we give an “Expensive” rating on the stock at the current market price of A$13.590 per share (down 1.307% on 23rd August 2019).

Costa Group Holdings Limited

1H19 Profitability Impacted on Account of Higher Capex: Costa Group Holdings Limited (ASX: CGC) is a leading horticulture group in Australia, engaged with activities of growing mushrooms, berries, glasshouse grown tomatoes etc. It is also involved in packing, marketing and distribution of fruit and vegetables within Australia. The market capitalisation of the company stood at A$1.21 Bn as on 23 August 2019. The company has recently published its results for the 1HFY19, wherein it reported revenue amounting to $573 Mn with growth of 11.8% on corresponding prior period and delivered EBITDA-SL of $82.4 Mn, reflecting a fall of 8.4% in comparison to the corresponding prior period, on account of lower Produce segment earnings. CGC posted NPAT-SL amounting to $40.9 Mn, a fall of $7.2 Mn against pcp.

.png)

1H19 Financial Summary (Source: Company Reports)

Future Aspects: The company stated that the fundamentals of the business remain strong, despite the current trading challenges. It added that the challenges and uncertainties primarily remain in light of continued lower than expected pricing of mushrooms. Potential pricing pressure on blueberry might also put pressure on the business, going forward. The company has scheduled further 2.67% acquisition of African Blue in late 2019 and 2020, which will bring the company’s total ownership to 90%.

Stock Recommendation: The company has refinanced senior debt facilities with extension of term to three- and four-year tenors as well as upsize of facilities amounting to $500 Mn. The asset to equity ratio of the company stood at 2.11x in FY18 as compared to the industry median of 1.97x. It posted a debt to equity ratio of 0.65x in FY18 against the industry median of 0.22x. On the price performance front, the stock delivered returns of -7.11% and -26.12% in the time span of one month and three months, respectively.

The performance during 1H19 was impacted by adverse conditions during the Moroccan blueberry season, low mushroom demand, raspberry quality and impact of citrus water cost and fruit fly. Consequently, the profitability was adversely impacted with EBITDA-SL and NPAT-SL witnessing a decline during the period. On account of lower profitability, challenging environment, and other factors, the stock saw a sharp fall post the release of 1H19 results as on 23rd August 2019. Given the backdrop of above-stated facts, we advise the investors to book the profit at the current level and, therefore, recommend a “Sell” rating on the stock at the current market price of A$3.170 per share (down 16.359% on 23rd August 2019).

LiveHire Limited

Issue of Shares Under EIP: LiveHire Limited (ASX: LVH) is into the provisioning of cloud-based human resources software and platform services with the market capitalisation of ~A$84.12 Mn as on 23rd August 2019. Recently, the company updated that Patrick Grant Galvin has made a change to his substantial holdings in the company with the current voting power of 5.16% as compared to the previous voting power of 6.31%, which became effective from 8th August 2019.

As per the release dated 9th August 2019, the company stated that it has issued 174,948 unquoted performance rights under the EIP (Employee Incentives Plan) to a senior employee of LVH. It added that the Performance Rights will be vested in two equal tranches on the achievement of performance hurdles by 30 June 2020 and will expire on 8 August 2023. In another update on 9 August 2019, the company completed the cashless buy-back of 6,966,390 ordinary shares which were subject to loan-back arrangements under the EIP.

For the quarter ended 30th June 2019, the company reported annualised recurring revenue (ARR) amounting to $2.53 Mn, reflecting a rise of 3% on QoQ basis. The following picture depicts key business metrics for the quarter ended 30th June 2019:

.png)

Key Business Metrics (Source: Company Reports)

Future Aspects: The company plans to deliver long-term sustained high CAGR in annualised recurring revenue by making an entry into international markets via outsourced channel sales partners, providing them with an easy to self-deploy, scalable Talent Community platform. The company is exploring MSP opportunities in new markets.

Stock Recommendation: The current ratio of the company stood at 13.34x in 1HFY19 as compared to the industry median of 1.58x. This implies that the company is in good position to address its short-term obligations in comparison to the broader industry. On the stock’s performance front, it produced returns of -22.97% and -29.63% in the time frame of one month and three months, respectively. As per ASX, the stock is trading closer to its 52-week lower levels. Hence, considering the above-stated facts and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.295 per share (up 1.724% on 23rd August 2019).

Bapcor Limited

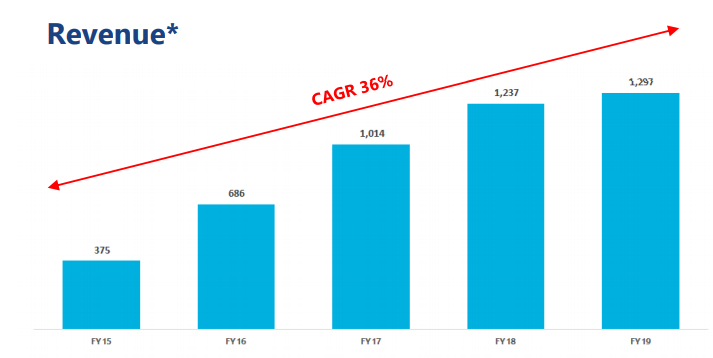

5-year CAGR growth in Revenue at 36%: Bapcor Limited (ASX: BAP) is involved into the sale and distribution of motor vehicle aftermarket parts and accessories. The market capitalisation of the company stood at ~A$1.9 Bn as on 23 August 2019. The company recently announced that The Vanguard Group, Inc. and its controlled entities has become an initial substantial holder in the company with the voting power of 5.048% on 16th August 2019.

The company released its full year results for FY19 which were in-line with the guidance. The Management stated that FY19 results reflected resilience to market conditions. The retail segment witnessed a challenging second half due to market conditions and high proportion of immature loss-making stores. The revenue and EBITDA of the company stood at $1,297 Mn and $164.6 Mn, reflecting a rise of 4.8% and 9.8% on YoY basis, respectively.

Revenue Growth over 5-years (Source: Company Reports)

Future Priorities: As per the FY19 results presentation, the company stated that first six weeks of trading has witnessed some sign of improvement in all the segments.The company expects mid to high single digit percentage increase in pro-forma NPAT and a rise of around 2% in EBITDA due to additional depreciation from investment in technology and systems for FY20.

Stock Recommendation: The company has declared a final dividend of 9.5 cps, fully franked, for FY19, which brings the total dividend for FY19 to 17.0 cps, reflecting a rise of 9.7% on FY2018 and representing 51% of pro-forma NPAT from continuing operations. The record date and payment date for the dividend are 30th August 2019 and 26th September 2019, respectively. The current ratio of the company stood at 2.29x in FY19, reflecting YoY growth of 16.9%, which represents that the company has improved its liquidity position to address its short-term obligations. Hence, considering the aforesaid facts coupled with decent outlook and sound liquidity levels as depicted by current ratio, we give a “Buy” recommendation on the stock at the current market price of A$6.700 per share (down 0.149% on 23rd August 2019).

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.