Stocks’ Details

PolyNovo Limited

US FDA Acknowledges NovoSorb® BTM as BreakthroughTechnology:PolyNovo Limited (ASX: PNV) is involved in the development of innovative medical devices for a number of applications, utilising the patented bioabsorbable polymer technology NovoSorb®. Recently, the company announced that Mr. Ed Graubart has been appointed as Senior Vice President of PolyNovo North America LLC with direct oversight of all sales and marketing functions in the US business.Mr. Graubart brings with himself, more than 29 years of experience in the orthopaedic medical industry, most recently as Vice President of Professional Development with Titan Spine LLC and previously 10 years with NuVasive Inc. as Senior Vice President of Sales. He has been issued 1 Mn share option with a strike price of $1.55 that will vest over the next 5 years.

In another update, the company informed the market that US FDA sees the potential of NovoSorb® BTM as “Breakthrough Technology” for the burn population. The company is revising its protocol design to incorporate FDA input and submit it to FDA in December 2019. With continued support from Biomedical Advanced Research and Development Authority (BARDA), pivotal trial details are expected to be announced in Q3FY20. Its successful completion of trial would help the company to deploy NovoSorb BTM for use in full thickness burns in the US. The company was added into S&P/ASX 200 Index, effective from September 23, 2019.

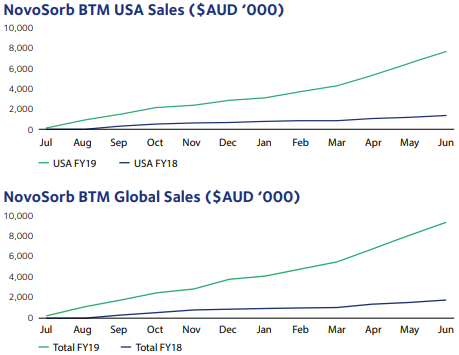

FY19 Key Highlights for the period ended June 30, 2019:Revenue for the period was reported at $13.683 Mn, an increase of 128% from FY18. Sales of goods revenue for the period increased by 435% to $9.348 Mn. Net loss after tax for the period was reported at $3.190 Mn, as compared to a loss of $5.974 Mn in the previous year. This can be attributed to the rising revenue generated by NovoSorb BTM sales in multiple markets. Cash on hand as on June 30, 2019 was reported at $13.9 Mn.

NovoSorb BTM Sales Data (Source: Company Reports)

What to expect:As per the release, CE Burn trail is completed with the final publication of results expected to come in by end of calendar year 2019. The company plans for significant expansion of sales of BTM in the US, Australia and New Zealand. So many exciting new product pipelines are in place in the breast and hernia segment. The group expects to break-even in FY20.

Stock Recommendation:PNV’s share generated a positive YTD return of 278.33%. Its gross margin for FY19 stood at 90.5%, better than the industry median of 70.8%. Its EBITDA margin and net margin for FY19 improved from the financial year 2018. Its current ratio for FY19 stood at 9.64x, better than the industry median of 2.47x. Currently, the stock is trading at its 52-week high level of $2.540. Hence, considering the aforesaid facts and current trading levels, we have a watch stance on the stock at the current market price of $2.540, up 11.894% on October 10, 2019 and suggest investors to wait for better entry levels.

Emeco Holdings Limited

Decent Top-line and Bottom-line Performance for FY19:Emeco Holdings Limited (ASX: EHL) is engaged in the provision of safe and reliable earthmoving equipment solutions to customers in the earthmoving industry as well as the maintenance and remanufacturing of major components of heavy earthmoving equipment. Recently, Paradice Investment Management Pty Ltd decreased its stake in the company from 6.724% to 5.174%, effective from October 3, 2019. In another update, EHL was removed from S&P/ASX 200 Index, effective from September 23, 2019.

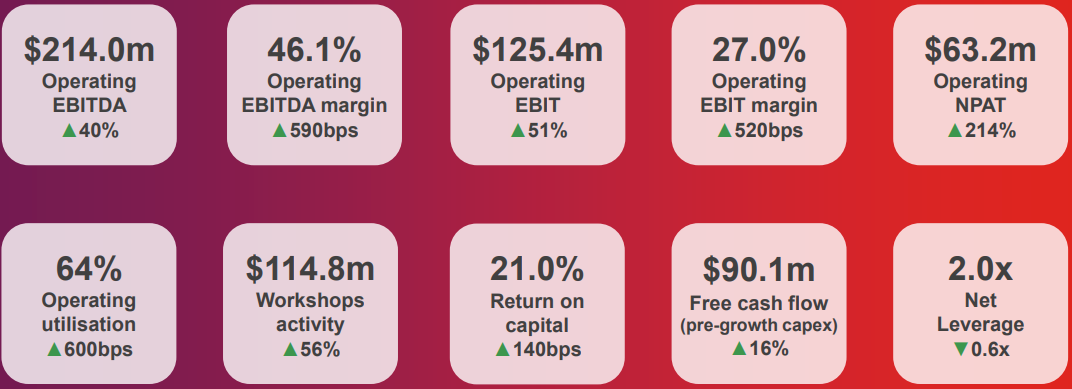

FY19 Key Highlights for the period ended June 30, 2019:Revenues from ordinary activities for continuing operations for the period increased by 21.9% to $464.5 Mn. Profit/(loss) from ordinary activities after tax attributable to members of Emeco Group for the period increased by 198.2% to $34 Mn. Profit/(loss) after tax (excluding significant items) increased by 213.9% to $63.1 Mn. The strong growth in earnings can be attributed to the continued increase in average operating utilization to 64% from 58% in FY18; improvement in rental rates; continued cost control; and a full-year contribution from Force and Matilda Equipment. Net tangible asset backing per ordinary security for FY19 was reported at $0.58, as compared to $0.48 in the previous corresponding period.

FY19 Key Metrics (Source: Company Reports)

What to expect:As per the release, the company expects to see an additional growth in revenue and earnings for FY20, with major weightage to the second half of financial year 2020. The company is expected to pursue greater commodity diversification in the financial year 2020. It is also focused in diversifying Eastern Region exposure to gold and copper. Moving forward, the company will be identifying opportunities to further build on its business model and widen its value proposition to achieve growth and sustainability through the cycle.

Stock Recommendation:EHL’s share generated a negative YTD return of 8.96%. The stock is trading close to its 5-week low level of $1.630. Its gross margin, EBITDA margin and net margin for FY19 stood at 33.9%, 42.8% and 7.2%, better than FY18 results of 28.8%, 38.2% and 1.4%, respectively, which implies that company’s fundamentals have improved against the previous year. Its ROE for FY19 stood at 19.2%, better than the industry median of 15.6%, which implies that the company generated a better return for its shareholders than its peer group. Moreover, EV/EBITDA multiple on NTM basis stands at 3.8x, lower than the industry median of 7.9x. Hence, considering the aforesaid facts and current trading levels, we recommend a “Speculative Buy” rating on the stock at the current market price of $1.870, up 2.186% on October 10, 2019.

Netwealth Group Limited

NWL’s FUA for Sep’19 Qtr Increased by 31.3% on PCP:Netwealth Group Limited (ASX: NWL) is involved in providing financial intermediaries and investors with financial services including managed funds, investor directed portfolio services, a superannuation master fund, separately managed accounts and self-managed superannuation administration services.

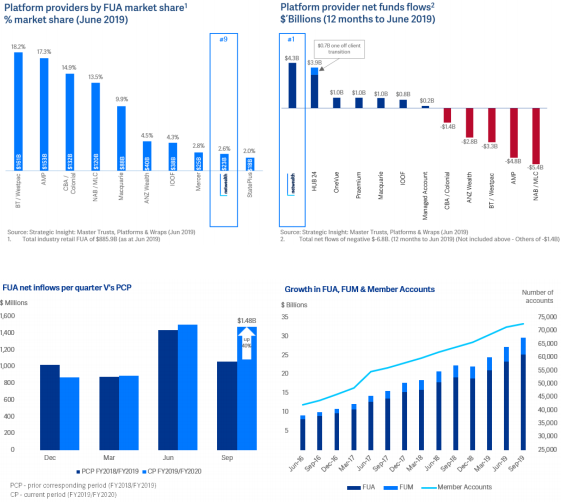

Recently,the company announced its September 2019 quarterly business update, wherein it highlighted that its funds under administration (FUA) as on September 30, 2019, was reported at $25.3 Bn, an increase of 8.5% on previous quarter, and 31.3% increase on previous corresponding period. FUA net inflows in the period were reported at $1.5 Bn, which was an increase of 39.6% against the previous corresponding period. Funds under management as on September 30, 2019, were reported at $4.4 Bn, an increase of 12.6% for the quarter.

The company was included in the S&P ASX200 index, effective from September 23, 2019.In another update, the company announced the appointment of Ms Sally Freeman as an independent non-executive director of the company. She has more than 25 years of experience as a risk consulting and corporate governance executive. She has headed KPMG’s national risk consulting practice, inclusive of internal audit, IT risk, privacy, forensic, actuaries, credit risk, liquidity risk, market risk, legislative compliance, data and analytics, governance, climate change and ethical sourcing. In July 2019, the company was awarded the SMSF platform provider for the year at Momentum Media SMSF awards.

NWL September’19 Quarter Key Metrics (Source: Company Reports)

What to expect:As per the release, the industry trends continue to support strong and sustainable growth with many major banks and institutions exiting or rationalising advice businesses. The company has a strong pipeline and is further looking for new opportunities. The company also expects to increase its investment in technology and people to maintain its market leading technology and service proposition.

Stock Recommendation:NWL’s share generated a positive YTD return of 17.37%. Its EBITDA margin and net margin for FY19 stood at 51.4% and 36.5%, lower than the industry median of 58.9% and 21.3%, respectively. Its ROE for FY19 stood at 53.6%, better than the industry median of 6.2%, which implies that the company generated a better return for its shareholders than its peer group. Its current ratio for FY19 stood at 4.36x, better than the industry median of 1.46x, which implies the company’s decent liquidity position. Currently, the stock is trading close to its 52-week high level of $10.110. Hence, considering the aforesaid facts and current trading levels, we have a wait and watch stance on the stock at the current market price of $9.200, up 3.139% on October 10, 2019.

.jpg)

Comparative Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.