Healthscope

-

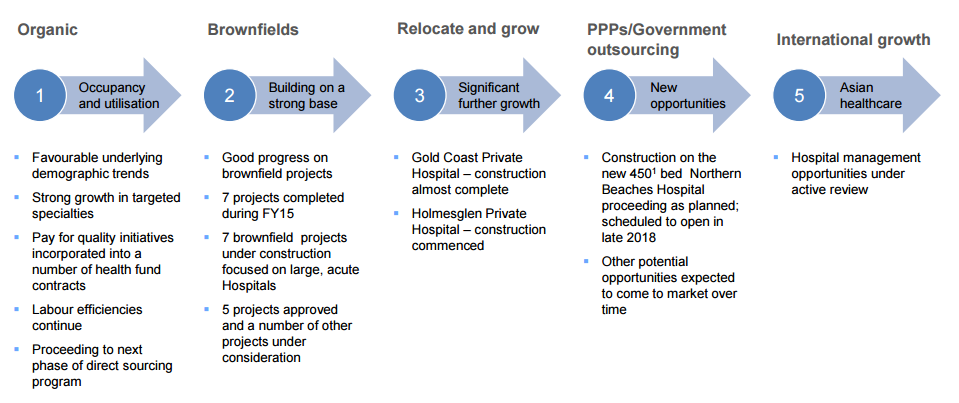

Strong pipeline of hospital expansion projects: Healthscope Ltd (ASX: HSO) delivered a lower than estimated results, with revenues at $2,438.2 million for the fiscal year of 2015, a 4.8% increase as compared to FY14, but decreased by 0.4% as compared to the statutory prospects. On the other hand, the hospitals segment (which contributes over 81% of the overall group’s EBITDA for FY15) revenues grew 5.7% yoy to $1,852.5 million, driven by the organic admissions growth while brownfields impact was less. Only 23 new beds were opened since past two years, while the group did not open any new beds in the second half of 2015. Meanwhile, Healthscope is making aggressive plans to expand its hospital segment, and estimates to deliver over 980 new beds and 50 new theatres by the end of 2018. HSO intends to begin some major capital projects like Gold Coast, Knox, and National Capital by the second half of Fiscal year 2016, resulting to a further growth from FY17.

NPAT FY15 performance (Source: Company Reports)

-

Improved Operating EBITDA across the segments: The group’s focus on operating efficiency has already been reflected in its EBIT growth during FY15, and HSO intends to further drive growth through better labor and procurement efficiencies. Healthscope’s operating EBITDA increased by 8.7% yoy to $388.3 million during FY15, which is 0.3% higher as compared to the Prospectus forecast. Accordingly, the Operating EBIT surged by 9.4% yoy to $286.9 million in FY15, 0.8% better as compared to prospectus forecast, while the group’s Operating NPAT rose by 4.0% to $153.1 million during the year. As per the segment highlights, the hospital segment’s operating EBITDA rose by 10.4% yoy to $327.6 million in FY15 and accordingly the operating EBITDA margin improved by 80 basis points to 17.7%, due to improved operating efficiency.

-

Outlook: The shares of Healthscope fell by 12.8% over the last six months, impacted by the tough market conditions. But the group’s recent change in in payment model for doctors would drive its earnings in future. Healthscope is a major hospital player to deliver quality and accreditation, and got 8% “Met with Merit” accreditation ratings from ACHS during the fiscal year, which is four times better as compared to the industry average of 2%. We remain bullish on the stock and recommend a “BUY” on the stock at the current price of $2.65.

Medibank Private

-

Delivered outstanding results: Medibank Private Ltd (ASX:MPL) reported a Statutory Group net profit after tax (NPAT) of $285.3 million for the fiscal year of 2015, as compared to $130.8 million in fiscal year of 2014. Moreover, the Pro forma Group NPAT rose 13.0% above the prospectus forecast to $291.8 million. MPL also declared dividends of 5.3 cents per share, which is better than the Prospectus forecast of 4.9 cents per share. The implied total year dividends is 7.4 cents per share (inclusive of pre-IPO dividend to Commonwealth) which is payout ratio of 70%. On the other hand, the group’s overall policy holders growth decreased by 60 basis points to 0.9% for FY15, as compared to 1.5%, due to higher membership lapses, cover reductions and change in revenues mix.

.png)

NPAT FY15 performance (Source: Company Reports)

-

Competitive margins against peers: The group’s Health Insurance premium revenue rose 5.1% yoy to $5,934.8 million during the year, but the segment’s operating profit delivered solid performance, by improving 33.8% yoy to $329.3 million in FY15, well above the prospectus estimates. Accordingly the Gross margin rose to 14.2% in FY15 against 13.5% in FY14, and higher than the Prospectus forecast of 13.6%. Management expense ratio for the segment also improved to 8.6% during FY15, against the FY14 ratio of 9.2%, and much better than the prospectus forecast of 8.7%. The net operating margin improved by 120 basis points to 5.5%, from 4.4% in fiscal year of 2014 and delivered above the prospectus forecast of 4.9%, driven by savings in management expenses and better health benefit claims management. Medibank intends to further improve its margins and enhance its operating base

.png)

Competitive margins as compared to peers (Source: Company Reports)

-

Outlook: The shares of Medibank Private Ltd(ASX:MPL) are trading at 5.1% higher since its IPO till date (as of September 3rd close). However, the stock has been under pressure over past few months, and even posted a negative 6.6% of year to date returns. However, with the group positing more than estimated results, the stock rallied over 6.6% in last four weeks alone. Moreover, Medibank issued a positive outlook, and estimates a Premium revenue growth of more than 5.5% in FY16. MPL estimates to further enhance its management expense ratio to 8.3% for FY16 and achieve less than 8.0% of MER during FY17. The group targets a better health Insurance operating profit of > $370 million for the fiscal year of 2016. We believe strong fundamentals of Medibank would drive the stock higher in the coming months, and give a “BUY” recommendation at the current stock price of $2.25.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.