Santos Ltd

A leading energy company in Australia and Asia, the company is focused on several things. It believes in driving value and performance in its basic businesses and aims to meet gas demand by unlocking its resources. It leverages existing and new infrastructure and capabilities for LNG. It is building a high value position in South-East Asia.

GLNG Plant (Curtis Island) (Source - Company Reports)

GLNG Plant (Curtis Island) (Source - Company Reports)

2014 full-year summary and business outlook

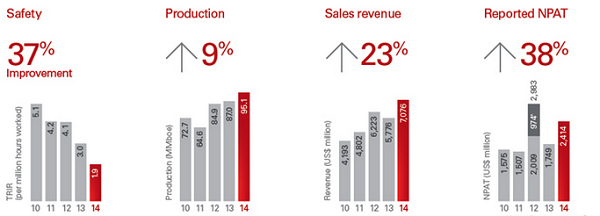

For the full year, production was up by 6% to 54.1 mmboe and sales revenue grew by 12% to a record figure of $ 4 billion. The underlying profit was up a 6% to $ 533 million though it recorded a net loss of $ 935 million after tax which reflected the impact of after tax non-cash impairment charges of $ 1.6 billion. The LTIFR was 0.67 hours for every million hours worked. In the area of project delivery, GLNG is approaching 95% completion within its budget of USD 18.5 billion and the first LNG is expected around the end of the third quarter of 2015. PNG LNG was completed ahead of schedule and 87 cargoes were shipped in the first 12 months. Peluang and Dua projects were also completed and are now online. In terms of cost savings, capital expenditure in 2015 is going to be 44% lower than 2014 and production costs for 2015 are going to be 10% lower per boe than 2014. Cost reductions in the range of 5% to 30% have been negotiated with suppliers and there is a freeze on recruitment and a reduction in the headcount. The company continues to optimise its leveraging of technology and innovation.

The focus on cost savings and operational efficiency translates into delivering higher production with lower capital expenditure. In the first quarter of 2015, production was up 15% over the previous year and capital expenditure was down by 40% for the same period. Apart from the 12% reduction in production costs for the first quarter of 2015, working closely with suppliers has reduced drilling rig day rates by 25%, well evaluation costs by 20% to 40% and savings of $ 450,000 per well on fracking and completion.

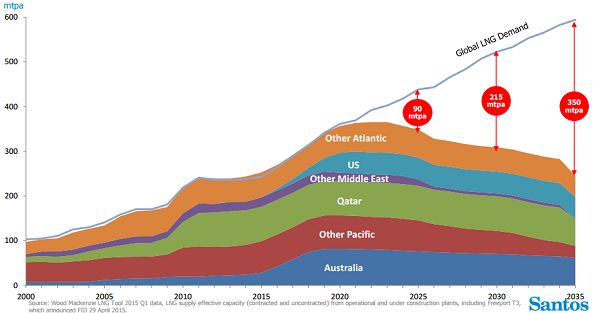

The global outlook for LNG supply and demand shows a continuing gap which is expected to continue to widen into the next decade.

Global Supply and Demand (Source: Company Reports)

The balance sheet and funding continue to be strong with $ 2.6 billion in liquidity and no significant debt maturity until 2017. The liquidity is made up of $ 0.6 billion in cash and cash equivalents and $ 2 billion by way of undrawn debt facilities as at 31 March 2015. Forecasts for free cash flows are expected to be positive in the fourth quarter of 2015 even at an assumed oil price of USD 60/bbl and GLNG will provide positive cash flows even at USD 40/bbl. The full-year dividend was up 17% at $ .35 per share.

We believe that the falling rig count indicates the success of the cost-cutting and the priority the company places on first exploiting richer wells. There is a good chance that oil prices may rise again if OPEC reaches its desired market position. This company also has a number of projects which should generate increased cash flows. We believe that, considering future prospects and growth, the stock is currently undervalued and have no hesitation in recommending that you buy at the current price of $7.62 .

Woodside Petroleum Ltd

In his strategy overview, the CEO says that the strategy remains effective and unchanged and is based on three interrelated concepts. Maximising the core business means maximising operational effectiveness, continuously improving the culture, existing the life of assets which are producing and developing contingent resources to supplement existing ones. Leveraging the company's capabilities means taking advantage of the full value chain of LNG, deepwater drilling, FPSO's and subsea technology as well as market relationships in Asia. Finally growing the portfolio means finding opportunities to provide diversification and optimisation, opportunities in the value chain and establishing aggregate positions by exploration portfolio rebalancing and acquisition of high quality assets in the current low oil price scenario.

.png) Financial Highlights (Source - Company Reports)

Financial Highlights (Source - Company Reports)

The catalysts for near-term value growth are several. The Browse FEED is expected by the middle of 2015 and Wheatstone is expecting its first gas in late 2016. Kitimat is appraising the upstream with targeted reductions in costs and Greater Enfield is aiming at accelerating FEED to take advantage of market conditions. High potential prospects are being drilled for exploration in the next 18 months and the company is actively seeking acquisitions because of the current low oil prices. The company believes that it will provide yield opportunities with strong growth by its de-risking through the Wheatstone acquisition, the added upside with the purchase of Kitimat, organic growth through Browse and Greater Enfield and additional opportunities from exploration, marketing and trading.

Important Highlights (Source - Company Reports)

The financial and operating metrics speak for themselves. Production is a record 95.1 million mmboe and the strong financial results include a reported NPAT of $ 2.4 billion, return on equity of 15.3% and free cash flow of $ 4.2 billion. The full-year dividend is a record USD 2.55 per share and the company has currently $ 6.8 billion worth of liquidity made up of $ 3.2 billion in cash and $ 3.6 billion in undrawn debt. The business continues to be cash flow positive even at low oil prices.

The company aims to be a global leader in exploration by 2018. Among the company's objectives are to achieve a portfolio which delivers the scale and expansion to generate year on year operational success. It wants to deliver consistent value in the top quartile with a success rate better than 25%, discovered resources in excess of 120% of production and finding costs in the top quartile of less than $ 4/boe.

In our opinion, the company has a great portfolio of long-term reserves which can be converted into production over a period of time as well as the financial strength to acquire new assets if they are available at attractive prices. We believe that this company is probably one of the most attractive stocks in the sector because of their ability to buy growth. we put a BUY at the current price of $33.57.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.