Rio Tinto Limited

-

Weak first half performance, but in line with estimates:Rio Tinto Limited (ASX: RIO) delivered weaker underlying earnings, which fell to $2.92 billion in the first half of 2015, against $4.19 billion in first half of 2014. The falling iron ore prices have led to decrease in average realized prices, due to which the group lost over $2.12 billion. As a result, the shares of Rio were impacted and fell over 22.3% over the last six months. On the other hand, Rio Tinto has undertaken efforts to offset this price negative impact by achieving cash savings of around $750 million as well as decreasing the capital expenditure to less than $7 billion for the fiscal year of 2015. Accordingly, for the first half of 2015, the cost reductions, exchange rates coupled with lower energy costs have helped the firm to cover around 40% of the prices decline. Rio Tinto is also seeking to maximize its cash flows by using inventory draw-down throughout the year. For the full year 2015, the group forecast a production of 43 million tonnes of bauxite, 8 million tonnes of alumina and 3.3 million tonnes of aluminum during 2015. RIO estimates to deliver global shipments of over 350 metric tonnes.

.png)

Rio Tinto’s Underlying Earnings (Source: Company Reports)

-

Focus on operational efficiencies: The group has undertaken initiatives to minimize its risks for its loss making projects, and has recently supported the decision of not conducting the final feasibility study for ERA’s (Rio Tinto holds 68.4% stake in this firm) Ranger 3 Deeps uranium project. Rio is offloading some of its non-core projects to improve its focus on strategic assets and completed the sale of its Murowa Diamonds (Rio has 78% interests) and Sengwa Colliery (Rio holds 50% interest) to RioZim Limited. Quite recently, Mick Davis, is also in talks with Rio Tinto, to acquire its coal assets in Australia- Hunter Valley, Bengalla, and Mount Thorley (Rio holds 80% interest in these three coal mines).

-

Why Buy RIO: The falling RIO’s stock prices offers opportunity to investors looking for cheaper value stocks, given its high resource potential and solid dividend yield of 6%. Moreover, with the iron ore prices trading near their multiyear low prices, any possible recovery from these levels would offer some support to the shares of RIO in the coming months. Based on the foregoing, we recommend a “BUY” to Rio Tinto at the current price of $48.81.

BHP Billiton

-

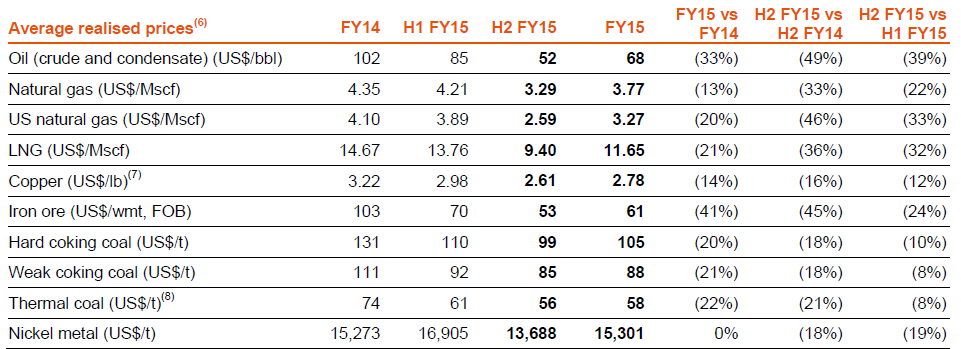

Improved Production to offset declining prices: BHP Billiton Limited (ASX: BHP) has improved its overall production by 9% on year over year (yoy) basis in the fiscal year 2015, while its core portfolio production rose 27% yoy since last two years. Petroleum production surged 4% yoy to 256 mmboe during FY15, boosted from contribution of 56 mmboe by the Onshore US liquids volumes, while the copper production remained at 1.7mt for the year impacted by the mill outage at Olympic dam in spite of better production at Escondida. BHP Billiton’s iron ore production grew 14% yoy to 233 mt in FY15 driven by the 13% yoy increase in Western Australia iron ore production (WAIO). Escondida organic growth project, Stage three expansion of BMA hay point as well as Escondida oxide leach area project witnessed first production during the year. On the other hand, the group’s iron ore and coal prices are linked to the index price for the month of the shipment. Therefore, the Iron ore, Oil (crude and condensate) and copper average realized prices fell 41%, 33% and 14% respectively in FY15, against earlier fiscal year. The group revalued 363 kt of outstanding copper sales at June 30, 2015, at average price of USD2.61 per pound.

Average Realized prices (Source: Company Reports)

-

Stock Performance: BHP Billiton shares opened on a positive note in this year and have rallied till $34.12 on March 2. But the pressure coming from the falling commodity prices, have impacted the stock leading to a decline of over 25.4% in the last six months. Moreover, BHP had to bear the impairment charges of USD 2 billion post tax associated with the demerger of South32. Accordingly, the firm’s underlying attributable profit would incur additional charges in the range of USD 350 million to USD 650 million in the June 2015 half year. Additionally, BHP issued a conservative fiscal year 2016 guidance, by decreasing its copper, petroleum and metallurgical coal production by 12%, 7% and 6% respectively. On the other hand, BHP is focusing on its operational efficiencies for its core assets portfolio post South32 demerger, which might give some support to the group’s profitability for the coming years. Having a dividend yield of 6.1% and cheaper P/E of 10.13x as compared to its peers, we reiterate our “BUY” recommendation on BHP Billiton at the current levels of $24.06

BHP Dividend Numbers (Source - Thomson Reuters)

BHP Dividend Numbers (Source - Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.