Company Overview: IRESS Limited is engaged in providing information, trading, compliance, order management, portfolio and wealth management, and related tools. The Company's segments are Financial Markets-APAC, Wealth Management-ANZ, UK, UK Lending, South Africa and Canada. Financial Markets-APAC segment provides information, trading, compliance, order management, portfolio systems and related tools to financial markets participants in Australia, New Zealand and Asia. Wealth Management-ANZ segment provides financial planning systems and related tools to Wealth Management professionals located in Australia and New Zealand. The UK Lending segment operates in the United Kingdom to provide mortgage origination software and associated consulting services to banks. The UK, South Africa and Canada segments operate by providing information, trading, compliance, order management, portfolio systems and related tools to financial markets participants in the United Kingdom, South Africa and Canada respectively.

.png)

IRE Details

Growth in Core Markets: IRESS Limited (ASX: IRE) is a leading technology company, providing software related products and services to the financial services industry. The company has its operations across Australia, New Zealand, Asia, Canada, United Kingdom and South Africa. During the year ended 31 December 2018, the company generated revenue amounting to $464.6 million, representing an increase of 8% on prior corresponding period. On a constant currency basis, revenue increased by 6%. The composition of revenue on the basis of the region came in as 54% from APAC, 32% from the United Kingdom, 10% from South Africa and 4% from Canada. Reported NPAT for the year stood at $64.1 million, increasing 7% on the previous year. EBITDA for the year amounted to $117.9 million, up 10% on prior corresponding period EBITDA of $107.3 million. On a reported basis, the company’s segment profit stood at $137.7 million, up 10% on prior corresponding period profit of $125.4 million. Key initiatives during the year included the introduction of IRESS Automated Personal Advice product which helped the clients to grow their business by providing digital advice to their customers. During the year, the company also opened IRESS Labs wherein it co-designs software with users. The period was also marked by the launch of IRESS Client Portal to assist in delivering a professional and personalised digital experience to clients. Several milestone projects were executed in 2018, including significant deliveries in the UK and Australia to large private wealth management and advice clients.

Over a period of 5 years starting from 2014 to 2018, the company has reported top-line CAGR growth of 9.0% with revenue in 2014 and 2018, amounting to $328.96 million and $464.62 million, respectively. Revenue over the 5-year period went up continuously with the highest growth of 10.3% in 2017. Bottom-line CAGR growth was reported at 6.1% with 2014 and 2018 profits amounting to $50.67 million and $64.10 million, respectively. The company has a history of delivering sustained shareholder returns, depicting a strong track record of revenue and earnings growth. Since 2008, revenue generated from the operations has been trending upwards with 8% growth in FY18. Revenue in FY18 increased due to strong overall performance, accompanied by improved operating leverage that helped earnings during the period.

Going forward, the company has a well established foundation in place for future growth. In the first half of 2019, the company reported a 10% growth in the segment profit as comapred to prior corresponding period. Overall in 2019, segment profit is expected to report growth in the range of 6% - 11%.

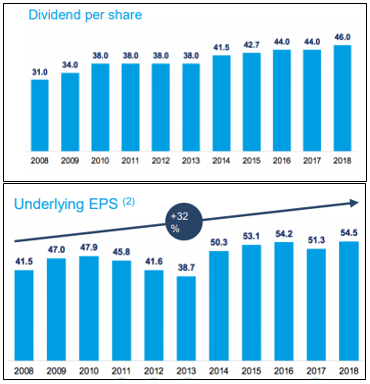

DPS & Underlying EPS (Source: Company Reports)

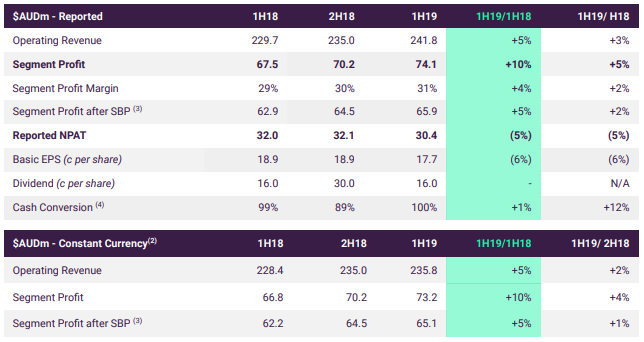

1H19 Financial Highlights: During the six months ended 30 June 2019, the company reported group revenue amounting to $241.8 million, up 5% in comparison to prior corresponding period. Revenue growth during the period was supported by growth in core markets and positive contribution from QuantHouse acquisition. Group segments profit stood at $74.1 million, up 10% on prior corresponding period. Reported NPAT for the period amounted to $30.4 million, down 5% on pcp. NPAT went up by 2%, excluding the impact of new leasing standard and QuantHouse acquisition. Dividend for the period remained flat in comparison to prior corresponding period at 16.0 cents. The shareholders received the dividend on 27 September 2019.

1H19 Financial Results (Source: Company Reports)

Acquisition of QuantHouse: The company recently acquired QuantHouse, a leading international provider of market data and trading infrastructure, for a total consideration of €38.9 million. The acquisition helped to expand the company’s footprints globally, providing clients with real-time access to additional services.

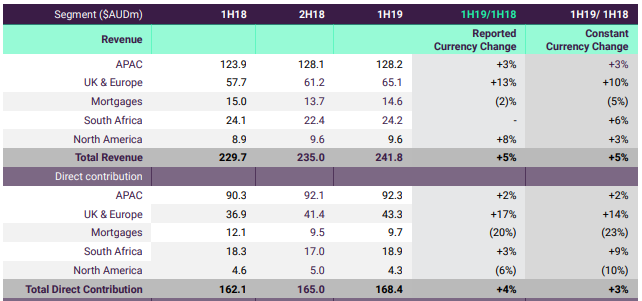

Segment Results:

APAC: Operating revenue for the segment stood at A$128.2 million, up 3% on prior corresponding period revenue of $123.9 million. During the period, growth was driven by the demand for financial advice software. Financial Advice revenue witnessed a rise of 9% as compared to pcp.

UK & Europe: This segment reported operating revenue of £35.5 million, up 10% in comparison to pcp revenue of £32.4 million. Revenue growth in the segment was driven by ongoing delivery to key clients and positive contribution from QuantHouse. Moreover, a significant project activity with new and existing clients will assist in revenue growth in the second half of FY19.

Mortgages: Revenue for the segment went down by 5% in comparison to pcp, due to project timing and investment for growth in Australia. The company signed new clients during the period that are expected to drive recurring revenue growth in the second half.

South Africa: The segment reported operating revenue of ZAR242 million, representing an increase of 6% on prior corresponding period. Direct contribution for the period stood at ZAR189 million, up 10% on prior corresponding period. The company is progressing well on the deployment of private wealth software to a large financial services client which is expected to be completed in 2H19.

North America: Operating revenue for the segment stood at $C9 million, up 3% on prior corresponding period revenue of $C8.8 million. Performance of the segment was characterised by stable recurring revenue and a positive revenue contribution from QuantHouse.

Segment Highlights (Source: Company Reports)

During the first half, the demand and delivery for software and services remained strong with the rising role of technology in financial services businesses globally. The performance in the first half established a base for further growth in the second half of 2019. Segment profit, including the impact of adopting new accounting standards and excluding the impact of acquisition of QuantHouse, is expected to report a rise in the range of 6%-11% in 2019.

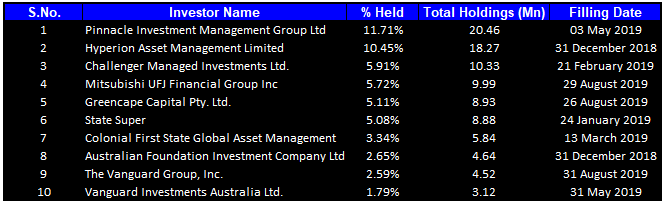

Shareholding Update: As per an announcement released on 03 September 2019, the company notified that Mitsubishi UFJ Financial Group Inc became a substantial shareholder of the company with a voting power of 5.72%. Another announcement dated 28 August 2019 notified that Greencape Capital Pty Ltd became a substantial shareholder with 5.11% of the voting power.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 54.35% of the total shareholding. Pinnacle Investment Management Group Ltd holds the maximum interest in the company at 11.71%, followed by Hyperion Asset Management Limited holding 10.45% of the shares.

Top Ten Shareholders (Source: Thomson Reuters)

Key Metrics: During the six months ended 30 June 2019, the company had an EBITDA margin of 27.1%, higher than the industry median of 26.1%. EBITDA margin for 1H19 also exceeded the margin of 25.5% in prior corresponding period. Gross margin for the period stood at 92.0%, slightly lower than the gross margin of 92.3% in prior corresponding period.

Key Metrics (Source: Thomson Reuters)

What to expect: In FY19, the company is expecting to report a segment profit in the range of $146 million - $153 million, representing growth in the range of 6% - 11% on a constant currency basis. Including the acquisition of QuantHouse, segment profit is anticipated to be in the range of $144 million - $151 million. Although, the acquisition of QuantHouse will be a loss-making step for 2019, it is expected to provide greater scale and strategic advantage from 2020. Non-operating costs in 2019, excluding acquisition related items are expected to be substantially lower than 2018. The company expects non-operating costs for the year in the range of $4 million - $6 million.

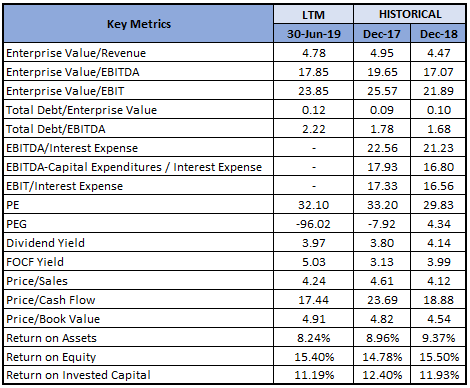

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

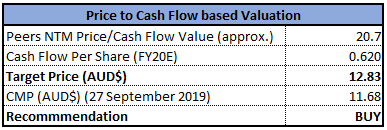

Method 1: Price to Cash Flow Based Approach:

Price/Cash Flow Valuation (Source: Thomson Reuters)

Stock Recommendation: The stock of the company generated negative returns of 6.84% and 17.58% over a period of 1 month and 3 months, respectively. During the first half of FY19, the company reported a strong cash conversion of 100% and recurring revenue of ~90%. On the segment front, UK & Europe was characterised by strong Private Wealth sales and client activity. South Africa reported a return to growth through adoption of new software and successful client deployments. The positive contribution from the acquisition of QuantHouse was also visible in the segment results. Going forward, the company expects the acquisition to be EPS accretive from 2020 and drive revenue growth post full integration into IRESS’ business. In North America, a project to deliver a broad retail trading system to a tier-one bank is underway with delivery expected in the second half of 2019. Overall, performance in the first half laid a strong foundation to incremental growth in the second half, majorly in the form of projects in progress with expected to complete in 2H19, acquisition of QuantHouse and sign up with new clients. Considering the above factors, we have valued the stock using a relative valuation method, i.e., Price/Cash Flow multiple and arrived at the target price of high single-digit upside (in % term). Hence, we recommend a “Buy” rating on the stock at a current market price of $11.680, up 0.864% on 27 September 2019.

IRE Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.