Income Statement (P&L)

Updated on 2023-08-29T11:59:24.877371Z

What is an Income Statement?

An income statement shows the profitability of a firm in a given reporting period. It is one of the three main financial statements used in evaluating a firm’s financial health. Even a small business is required to furnish financial statements for bankers to avail credit funding.

Also known as Profit & Loss (P&L) Statement, it reports the net income generated by a firm after summarising all income and expenses for a firm during a given period. It includes the impact of gains, losses, revenue, and expense.

Firms registered under the Company/Corporation Act of any jurisdictions are required to report financial statements periodically, and reporting intervals are usually quarterly, semi-annually, and annually.

Read: Evaluating Financial Statements

The purpose of the income statement is to project the firm’s financial performance in a given period. Financial statements of an enterprise are created through trial balance, which is furnished through daily journal entries.

An income statement will enable to figure out the profitability, losses, fixed costs, variables, administrative expenses etc. It is used along with the balance sheet, cash flow statement to analyse a business. The study of income statement helps the business owners and other financial statement users to know if the company is able to price its products well.

Investors keep tracking financial statements, including income statement, to evaluate the changes in the fair value of the business. A regular reporting of income statements allows investors to understand how the business is delivering against their expectations, forecast or estimates.

A continuous and transparent information flow by companies is crucial for investors because the actual underlying changes in financial statements of the business will impact the perceived fair value assigned by investors w.r.t the business.

But income statement does not include the actual cash realisation and cash disbursement of a firm during the period. While undertaking the financial modelling of a business, it serves as a predecessor to prepare balance sheet and cash flow statement.

Income Statement Vs Balance Sheet

The Income statement and balance sheet are two financial statements that are generally used together but have different information and scope. Income statement may only involve the information of reported period, while the balance sheet represents the value of business on a specified date, which is the last day of reported period.

An income statement is a summary of revenue, expenses, gains and losses during a period, whereas the balance sheet shows the value of assets and liabilities of a firm on a specified date. While income statement reflects profitability, margins and cost, balance sheet primarily depicts the liquidity of a firm to service its obligations.

What constitutes an Income Statement?

Revenue & Gains

Revenue refers to the sum of money recorded by a firm in lieu of selling products or services. It usually refers to operating revenue. A payment received by a retailer from its customer is revenue for the retailer.

In income statement, it is recorded on an accrual basis, meaning that reporting of revenues does not mean cash realisation. Most of the businesses sell goods on credit and payment from the buyers is received after some time, but revenue is recorded when goods are sold (transfer of risk), and cash is realised when payment is received.

Firms can also have multiple and sometimes inconsistent sources of income. It can depend on the information seeker to include the component in revenue or not. Firms can place funds in short term money market to generate interest income and other transactions like commission on selling specific product for some time.

Gains can arise during a business period, and it also depends on the type of business. Sometimes there are unrealised gains, especially in companies that are required to value assets externally such as equity holding, real estate, cattle stock.

Firms also report gains on the sale of assets, but the gain is recorded when the sale consideration is greater than the value of the particular asset in the books or balance sheet.

Expenses & Losses

Revenue is supported by the expenses incurred by a firm. In an operating period, firms can incur a range of expenses. It is important to deduct expenses from the total income to arrive at net income figure.

Under the accrual basis, the expenses can be recorded at a different time than the actual disbursement of cash. Firms incur expenses prior to actual disbursements like wages, sales commission, provisions.

But expenses are also incurred even when payment is made before such as depreciation on machinery is charged to income statement, and amortisation of intangible assets is also charged on income statement.

Expenses are recorded proactively as they incur. Cost of Goods Sold includes the expenses that were directly incurred to generate from the sale of the product. Operating expenses include wages, administrative, distribution etc.

Similar to gains in the above part, losses can be incurred by a firm like a loss on the sale of the asset or unrealised losses in the assets. Interest expenses, which are interest payments on debt, are also recorded in income statement.

Impairment losses are also incurred by companies. When a business has suffered a significant fall in the value of any long-term asset, impairment charges will be incurred to record the fall in the value of the asset.

Likewise, firms are also required to test purchased goodwill for impairment charges annually, and reduction in the value of goodwill will force an impairment charge.

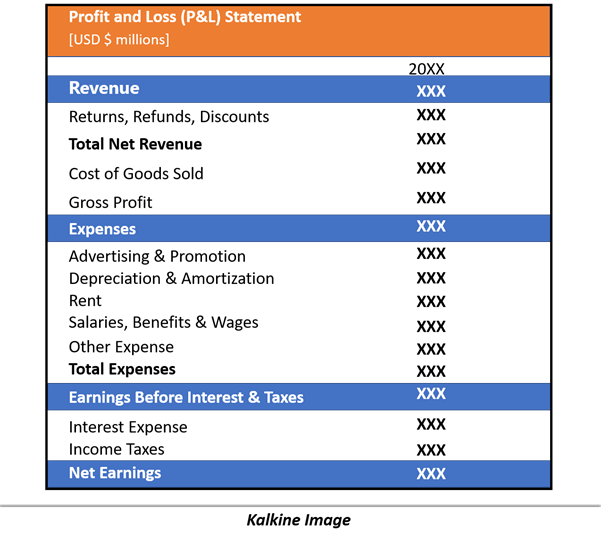

Basic Income Statement

Below is a basic income statement used in Corporate Finance.

Cost of Goods Sold: Cost of goods sold is the total direct cost incurred by a firm from the procurement of raw material to the sale of finished goods. Some firms may not provide the cost of goods sold and can provide other measures like the cost of sales or cost of services.

Gross Profit: Gross profit is the amount of money earned by the business after deducting COGS from revenue, cost of sales or cost of service from the revenues. It does not include variable cost incurred in manufacturing a product.

Operating Expenses: Operating expenses are the expenses incurred during a reporting period and include items like wages, salary, marketing, selling, distribution, depreciation and amortisation. Subtracting operating expenses from gross profit will give operating earnings of the business.

Interest Expenses: Interest expenses are the funds paid to creditors or lenders of the company as interest payments on debt.

Income Taxes: Income taxes are the tax paid to the government on the profits of the business.

Net Income: It is calculated by deducting interest expenses and tax from operating earnings to arrive at net income and earnings per share.