Coca-Cola Amatil Ltd

.PNG)

CCL Details

Better net profit growth: Coca-Cola Amatil Ltd (ASX: CCL) reported a 2.8% rise in revenues for the first half of FY2016 to $2.5 billion while EBIT grew 3.2%. Better EBIT and savings from finance cost helped the company to report a 7.8% rise in net profit to $198.2 million. The company has declared an interim dividend of $21 per share. The company generated free cash flow of $206.2 million while cash realization increased to 98.1% from 49.7%. Regionally New Zealand and Fiji reported 5.4% rise in EBIT. Australian business however declined 1.9% at EBIT level. Going forward the company expects low single digit EBIT growth, which is expected.

But, in the developing market of Indonesia, FIJI and PNG as well as in Alcohol and coffee segment, the management expects double digit EBIT growth. Having a solid dividend yield, we believe the stock is a “Hold” at current market price of $9.97

.png)

CCL Daily Chart (Source: Thomson Reuters)

NIB Holdings Ltd

NHF Details

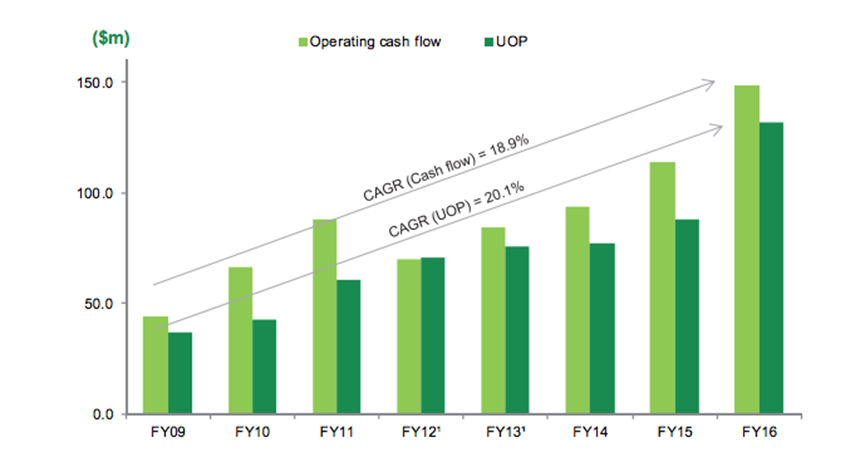

Splendid performance:NIB Holdings Ltd (ASX: NHF) is building on its whitelabelling capabilities by recently entering into a health insurance whitelabelling distribution partnership with New Zealand Automobile Association. NHF earlier reported a strong 14.3% revenue growth to $1.9 billion with underlying profit growth of 49.9% to $132 million backed by impressive growth in all segments and improved underlying operating profit (UOP) in FY16. Businesses other than Arhi increased UOP by 132% to $37.5 million and accounted for 28.4% of group UOP as compared to 18.3% in FY15.

The World Nomads Group made inaugural contribution of $9.7 million while New Zealand business doubled UOP to $17.3 million. With this, the company reported net profit of $91.8 million, up 22%. The group has announced a joint venture with BUPA and HBF which would expand its reach and consumer engagement (~6 million people).

Strong operating cash flow correlating with UOP (Source: Company Reports)

On the other hand, management reported that they would continue to face pressure from rising competition and pressure on margins would also continue due to premium affordability.

The stock already generated over 40.35% during this year to date (as of October 06, 2016) and is trading at a higher P/E. We rate the stock as “Expensive” at the current market price of $4.78

NHF Daily Chart (Source: Thomson Reuters)

Goodman Group Pty Ltd

.PNG)

GMG Details

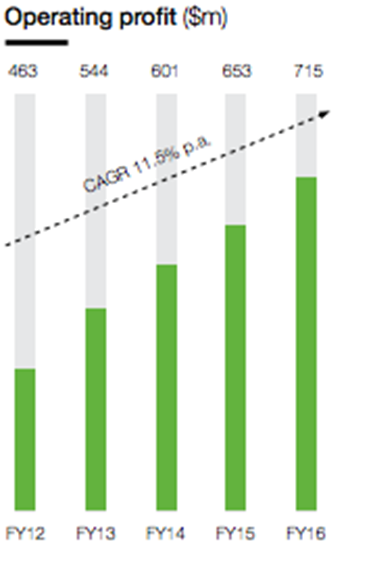

Blackstone plans to acquire logistic assets:Goodman Group Pty Ltd (ASX: GMG) recently announced for the amendment of constitution of Goodman Industrial Trust for the Attribution Managed Investment Trust regime. GMG also reported that Blackstone Group, New York is planning to acquire a second tranche of logistics assets from the group in Australia for more than $650 million (15 assets). Through this move, Blackstone would be the biggest owner of the assets class in the country. During FY16, GMG witnessed a 9% increase in operating profit to $715 million.

Furthermore, the group’s long-term plan which would underpin the group’s future, focuses on low borrowings, a robust balance sheet and strong customer relationships and were the key features for FY16. The group reported statutory profit of $1,275 million contributing to 19% growth in net tangible assets per security.

Operating profit (Source: Company Reports)

The group declared dividend of 24 cents per share, up 8% from FY15. On the other hand, GMG stock fell over 4.7% in the last four weeks (as of October 06, 2016) on concerns over Australian economy.

Based on a Washington-based International Strategic Studies Association, the group has been cautioned over Australian property market if the government is not taking proper measures. We believe that the stock is “Expensive” at the current market price of $6.99

GMG Daily Chart (Source: Thomson Reuters)

Monash IVF Group Ltd

.PNG)

MVF Details

Strong results:Monash IVF Group Ltd (ASX: MVF) reported a 25.3% rise in revenues to $156.6 million, driven 10.7% by organic growth and 14.6% by acquisitions.

Total IVF treatments were up by 12.9% to $17.9 million which led the Net profit after tax to witness a 346% strong growth to $28.8 million. Ultrasound revenues increased over 200% driven by the acquisition of Sydney Ultrasound for Women in June 2015.

.png)

Key financials (

Source: Company Reports)

The company reported RoE of 19.3% up 340 basis points and repaid debt, while reducing them by 10.6% to $86.5 million. The company has 23.8% market share with strong presence in Victoria and South Australia.

The group has declared final dividend of 4.5 cents making total dividend of 8.5% for the year. We give a “Hold” at the current market price of $2.49

.png)

MVF Daily Chart (Source: Thomson Reuters)

Vita Group Limited

.PNG)

VTG Details

Impressive net profit growth:Vita Group Limited (ASX: VTG) reported a 19% rise in revenues to $645.1 million while the net profit growth of 43% to $38 million was the highlight for FY16. The underlying EBITDA was up 55% to $62 million.

VTG operates through 137 operating outlets, which comprised of 100 Telstra Corporation Ltd retail stores, 21 Telstra business centers, 14 One Zero and 2 Fone Zone outlets.

.png)

Revenue and EBITDA growth (Source: Company Reports)

Telstra stores and business centers helped the company to report like-for-like store sales growth to 18% in the retail segment and 8% in its small and medium business segment.

The group declared about 14 cents per share dividend for the year, which is up 75% over FY15. VTG plans to hold its AGM on October 28, 2016. We give a “Hold” on the stock at the current market price of $4.97

.png)

VTG Daily Chart (Source: Thomson Reuters)

Pact Group Holdings Ltd

.PNG)

PGH Details

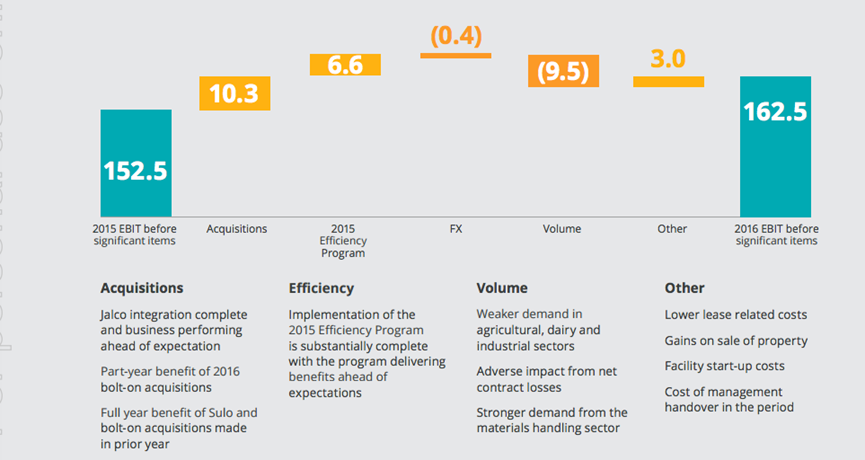

Acquisition to boost earning:Pact Group Holdings Ltd (ASX: PGH) has entered into an agreement to acquire specialty contract manufacturer Australian Pharmaceutical Manufacturers, which is one of the largest providers of manufacturing and packaging services for nutraceuticals in Australia, for $90 million. The acquisition would be funded by $75 million of bank debt and $15 million share issue. The management expects the acquisition to be earning accretive in year one and to meet the company’s 20% return on investment target in three years. Furthermore, for FY16, sales revenue increased 10.6% to $1381.3 million while EBIT grew 7%. Net profit after significant items grew 26% to $85.1 million. Total dividend per share stands at 21 cents compared with 19.5 cents in previous year.

Total shareholders return is at 33.5% compared to 36.6% earlier. The group has implemented efficiency program in 2015, which is expected to deliver $15 million of annual savings in 2017.

Acquisition and efficiency drive EBIT growth (Source: Company Reports)

According to the program, the group closed 3 plants, rationalized 5 plants, and moreover $6.6 million efficiency savings were realized in FY2016.

The total program cost is expected to be at $30 million pretax. As a result, the stock surged over 29.66% in the last six months (as of October 06, 2016) and reached a higher P/E while trading close to its 52-week high price. We rate the stock “Expensive” at the current market price of $6.47

PGH Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our

Terms & Conditions has been provided please go through them and also have a read of the

Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.